In Gold We Trust May 2022

Thanks to a subscriber for this book-sized report from the team at Incrementum. Here is a section comparing the USA to Rome.

The Roman experience looks eerily similar to the present US economic situation. Just like ancient Rome, the USA enjoys the privilege and shoulders the burden of enforcing its “Washington Consensus” on the world, but like late-stage Rome, the US cannot fund its army and welfare state through taxation alone.

As Rome had to resort to currency debasement to pay for its welfare/warfare state, the US finds itself increasingly unable to fund current expenditures through taxation. For each downcycle the US relies ever more on a complex process of bond issuance, covert, and more recently, overt inflationary policies to ensure the once mighty Empire can pay its bills.

Although the US saw expenditures soar during the world wars, large subsequent surpluses allowed the Federal fiscal house to remain in order. When the last vestiges of the old Gold Standard were abandoned in the 1970s, the spending dynamic changed as the Empire no longer needed to adhere to a sound fiscal policy. Funding was secured via the central bank. The modern-day Empire felt entitled to take full advantage of its ‘exorbitant privilege’ to keep its soldiers and plebs content, docile and obedient.

During the Global Financial Crisis (GFC), taxes covered less than 60% of outlays, down from an average of ~90% in preceding decades. In the course of the Covid-19 shutdowns the US government funded less than 50% of its outlays from taxation.

Rome found itself equally tied down by a Gordian knot. The ancient Empire had to fund its army above all else. Imperator Severus famously advised his sons Caracalla and Geta to “Be harmonious, enrich the soldiers, scorn all others” 61 to remain in power.

Similarly, the US has to placate its industrial military complex, but even more important to modern day ‘Imperators’ is to mollify the ~60% of its population who are either on state welfare or directly employed by the government.

Here is a link to the full report.

The investment community has been conditioned to believe technological innovation will continue to provide sufficiently large benefits and productivity gains to compensate for rising debt levels. A powerful secular bull market delivers big gains and changes how people perceive risk and react to downdrafts. That helps to explain the rush to buy the dips at every initial sign of a relief rally taking hold.

Artificial Intelligence, robotics, synthetic biology, autonomous vehicles and nuclear fusion are being discussed as near-term realizable solutions. I don’t think investors are prepared for the possibility the timeline for these kinds of advances might stretch to a decade or more. The fact Elon Musk’s latest pronouncement that full self-driving is less than a year away fell flat is a sign enthusiasm for inevitable imminent technological disruption is waning.

Every big bull market is also based on contraction. Sometimes it is earnings don’t matter, other times its global domination is inevitable, today it is debt doesn’t matter.

The threat to growth means debt is currently a good investment destination. Yields spiked higher and are now rapidly unwinding that condition. The temptation is to think of the debt issues as insurmountable is very powerful, except the issue is now global.

The global financial crisis resulted in Europe failing to raise rates. Today they are still extraordinarily cautious about doing so. The pandemic may have the same effect on the USA. Funding operations without recourse to much higher taxation is impossible with higher yields. We already have evidence the economy is unable to tolerate even modest hikes.

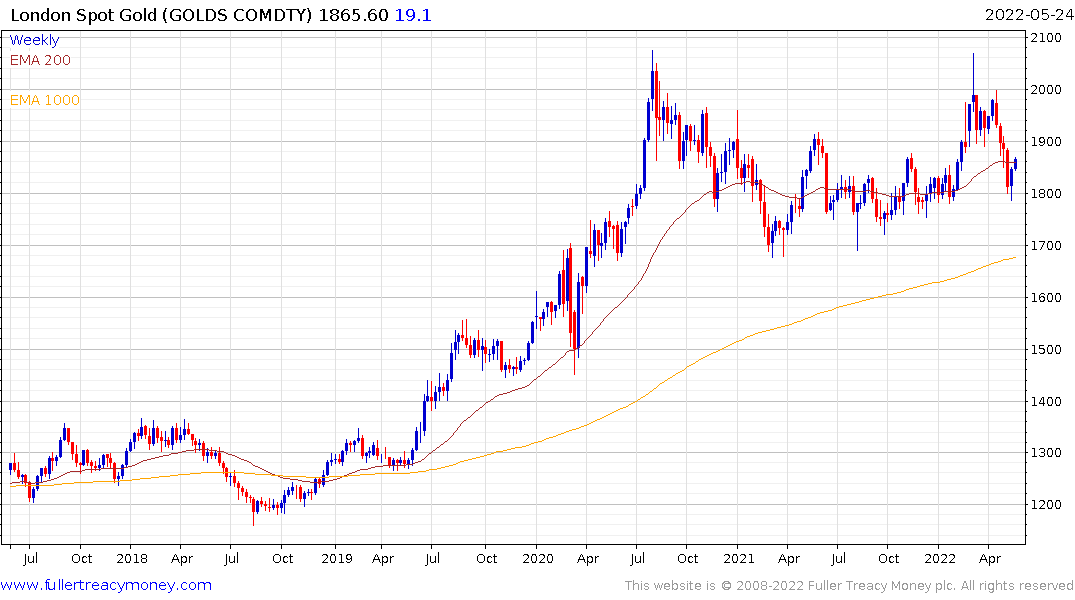

The trend of debt accumulation and devaluation of fiat currency purchasing power is not about to disappear. Governments find themselves in debt traps and that’s why gold is rebounding. It remains a barometer against which we can measure the decline in the purchasing power of government issued currencies.

Meanwhile the Nasdaq-100’s correlation with the bond market has evaporated as growth concerns now overpower inflationary issues. The Index continues to trend lower.

Meanwhile the Nasdaq-100’s correlation with the bond market has evaporated as growth concerns now overpower inflationary issues. The Index continues to trend lower.

The reality is bull markets thrive on liquidity. The longer they last the more liquidity they need. The pandemic infused global markets with trillions in additional new capital. Additional infusions of at least that much will be required to recharge bullish sentiment. That’s also why China’s efforts to support the economy has been so slow to show results. The size of the promised assistance is just not big enough to move the needle.

The reality is bull markets thrive on liquidity. The longer they last the more liquidity they need. The pandemic infused global markets with trillions in additional new capital. Additional infusions of at least that much will be required to recharge bullish sentiment. That’s also why China’s efforts to support the economy has been so slow to show results. The size of the promised assistance is just not big enough to move the needle.