In gold we trust

Thanks to a subscriber for the 11th annual edition of Ronald-Peter Stöferle and Mark J. Valek’s trademark report on the gold market for Incrementum. Here is a section:

Moreover, the ratio of real assets to financial assets is currently the lowest since 1925.5 In a study worth reading, Michael Hartnett, chief strategist at Bank of America Merrill Lynch, recommends to “get real”, i.e. to reallocate investments from financial assets into real assets.

"Today the humiliation is very clearly commodities, while the hubris resides in fixed-income markets" as Hartnett explains. Gold, diamonds, and farmland show the highest positive correlation with rising inflation, whereas equities and bonds are negatively correlated with increasing prices, a finding that we have pointed out repeatedly. The political trend towards more protectionism and stepped-up fiscal stimuli will also structurally drive price inflation.6

In the past years, rate cuts and other monetary stimuli have affected mainly asset price inflation. Last year, we wrote: “Sooner or later, the reflation measures will take hold, and asset price inflation will spill over into consumer prices. Given that consumer price inflation cannot be fine-tuned by the central banks at their discretion, a prolonged cycle of price inflation may now be looming ahead.” 2016 might have been the year when price inflation turned the corner. However, the hopes of an economic upswing due to Trumponomics and the strong US dollar have caused inflation pressure to decrease for the time being. Upcoming recession fears resulting in a U-turn by the Fed, and the consequential depreciation of the US dollar would probably finalise the entry into a new age of inflation. This will be the moment in which gold will begin to shine again.

Low interest rates combined with the pressure to invest and FOMO, have nurtured a treacherous sense of carelessness within many market participants. Scenarios such as significantly higher inflation or a recession are currently treated like black swans, although history shows that these events do occur at regular intervals.

Many signals suggest that we are about to face a big shift within the financial and monetary system. Nobody can foresee what it will look like. But an early look at such scenarios creates a good opportunity to come out stronger at the other side of this transition. As Roland Baader brilliantly summed it up: “In the middle of the boisterous summer party, the sensitive ones start feeling the chills.”7 To some degree, we find ourselves in this quote.

Here is a link to the full report.

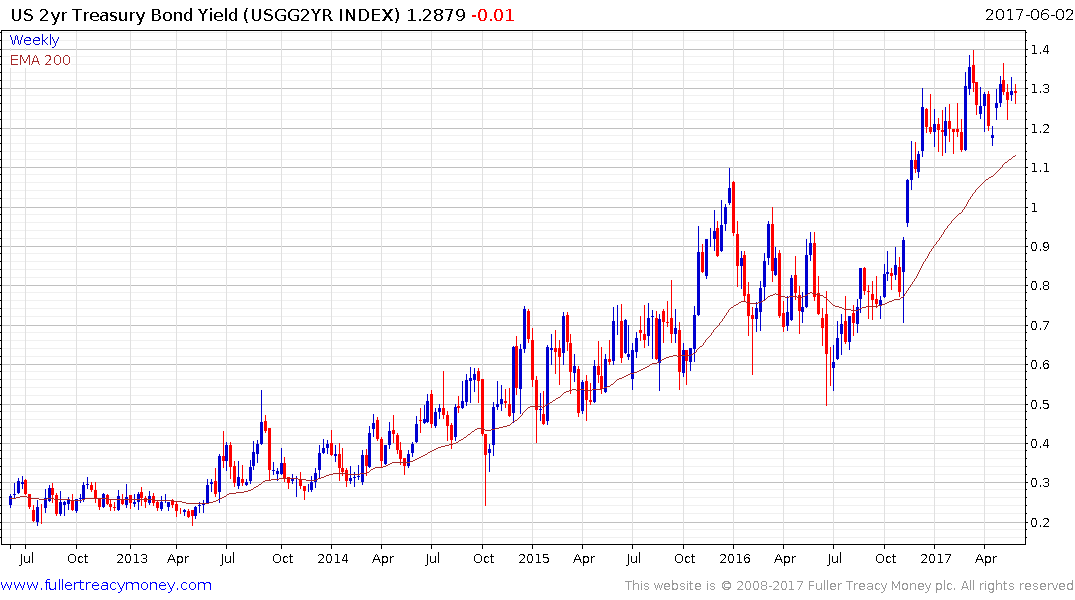

2-year yields at a shade under 1.3% signal bond investors are unwilling to anticipate Fed action beyond the next quarter. They’ve probably been punished too much for making that mistake over the last few years when the Fed has overpromised and under delivered on rate hikes.

Considering the Fed is now talking about beginning the process of normalising its balance sheet, the bond market has probably correctly assumed that will put a dampener on the central bank’s ability to continue to raise rates.

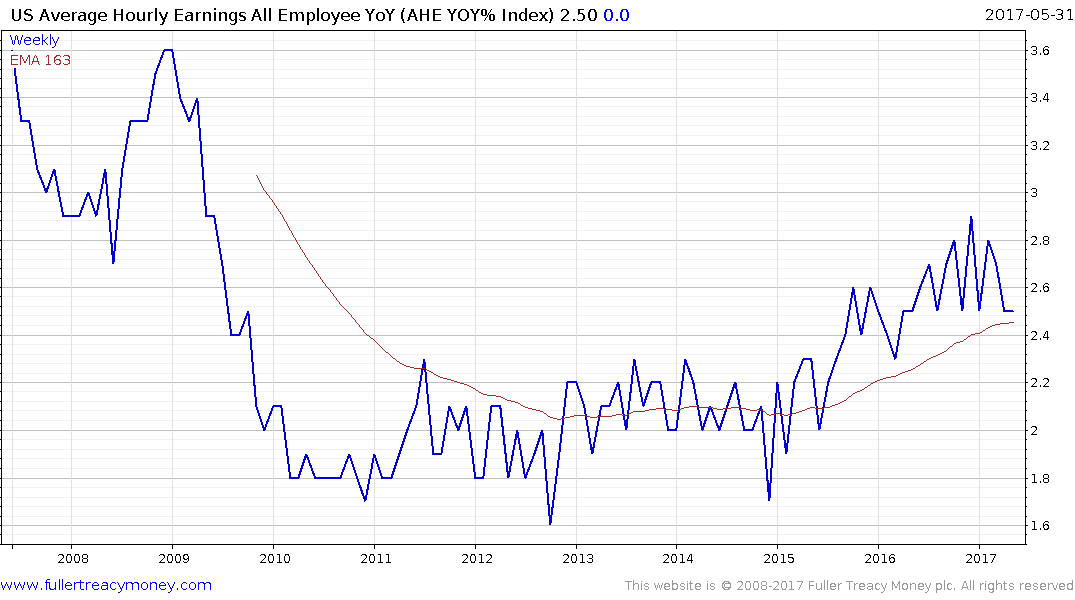

The clearest evidence of building inflationary pressures is in wage growth but even that has been static over the last year. Therefore the argument for imminent jumps to inflation expectations would appear to be too early for the market.

Right now gold prices are rising gently but a sustained move above $1350 will be required to signal a return to medium-term demand dominance.