I have seen the future and his name is Kevin

Thanks to a subscriber for this note by Albert Edwards at SocGen which may be of interest to subscribers. Here is a section:

Summers’ relaxed view on the debt build-up, particularly visible in the corporate sector, is in sharp contrast with our own view that this looks set to wreck the US economy. Summers was particularly dismissive of comparing debt to income as the former is a stock and the latter a flow concept. He thought it entirely appropriate in a world of lower interest rates that debt had reached record levels relative to income? belying, for example, the concerns expressed by the IMF this week. Should we worry about the chart below or not?

The charts above and below have just been updated by my colleague Andrew Lapthorne (and using the S&P 1500 ex financials universe). Summers? point was we shouldn’t be too stressed about rising debt as 1) QE is driving up asset prices and higher debt does not look excessive relative to assets, and 2) rock-bottom interest rates mean the debt is easily serviceable. Now on the first point, Andrew shows that quoted company corporate debt has rocketed relative to assets to now exceed the madness last seen at the height of the 2000 TMT bubble. Indeed the problem with Summers? analysis in my view is that it is the higher debt that is being used to push up asset values (via share buybacks), just as it did during the housing bubble in 2005-7. And by pushing asset values well beyond fundamentals you build debt structures on false asset values, which only become apparent when the asset bubble bursts. And am I in any way reassured that the Fed sees no bubbles? No, I am not. These dudes will never identify an asset bubble? at least before the event!

Andrew notes that the way corporate bond pricing models work (e.g. Moody’s KMV and Merton’s “distance to default” models) it is not just a company’s ability to pay its coupon that affects its valuation. Investors are in effect always asking, can this company repay its principal TODAY, even though the repayment is not actually due for 30 years. If asset values collapse in the event of a recession, corporate bond spreads will explode irrespective of the fact that they can easily pay the interest. But hang on a second, let’s just look at interest cover for the quoted sector, for Andrew finds that despite record low interest rates, cover has declined to levels last seen in the depths of the last recession (see chart below)! In the next recession a sharp decline in both profits and the equity market will reveal this Vortex of Debility. US corporate spreads will then explode as the economy is overwhelmed by corporate defaults and bankruptcies. And with the Fed having been the midwife of yet another financial crisis, what price do you give me for it to lose its independence?

Here is a link to the full report.

A point I’ve made on a number of occasions is that the corporate finance courses taken by MBA students dictate that corporations attempt to access the cheapest cost of funding in order to reduce the weighted average cost of capital. It is advantageous, from a balance sheet perspective, to load up on debt when interest rates are low and to extend the maturity out as far as is practicable, then to use the proceeds to buy back shares, regardless of price, because that reduces funding costs overall.

Our fiscal instincts might recoil at such low regard for value for money when a company is throwing around shareholder equity but since it results in generally higher stock prices rebellions are seldom seen. The massive debt build-up in the 1990s funded the creation of the internet but on this occasion the debt has been used to refinance old debt, buyback shares and most of the capital expenditure has been on labour saving devices like software and factory automation rather than physical infrastructure. The rapid pace of technological innovation may at least in part nullify this qualification since so much activity now takes place online rather than at physical locations.

Despite the higher debt to income levels overall, perhaps a more important question is when it is likely to contract or revert to the mean? Interest cover might be low but is unlikely to become a problem until fixed rate debt is refinanced. DoubleLine has been issuing charts for quite some time highlighting the quantity of both government and corporate debt that needs to be refinanced from 2018 through 2021. However markets are discounting mechanisms so as corporate treasuries begin to price in the prospect of a Fed rate hike this year and perhaps another next year corporate spreads are likely to come into sharper focus.

It is still open to question just why LIBOR rates have rallied well beyond the Fed Funds rate but the impending changes to money market funds (due tomorrow) is at least partly to blame. With a great deal of debt tied to LIBOR, if rates stay higher for longer that is likely to affect the ability of companies to continues to source cheap debt.

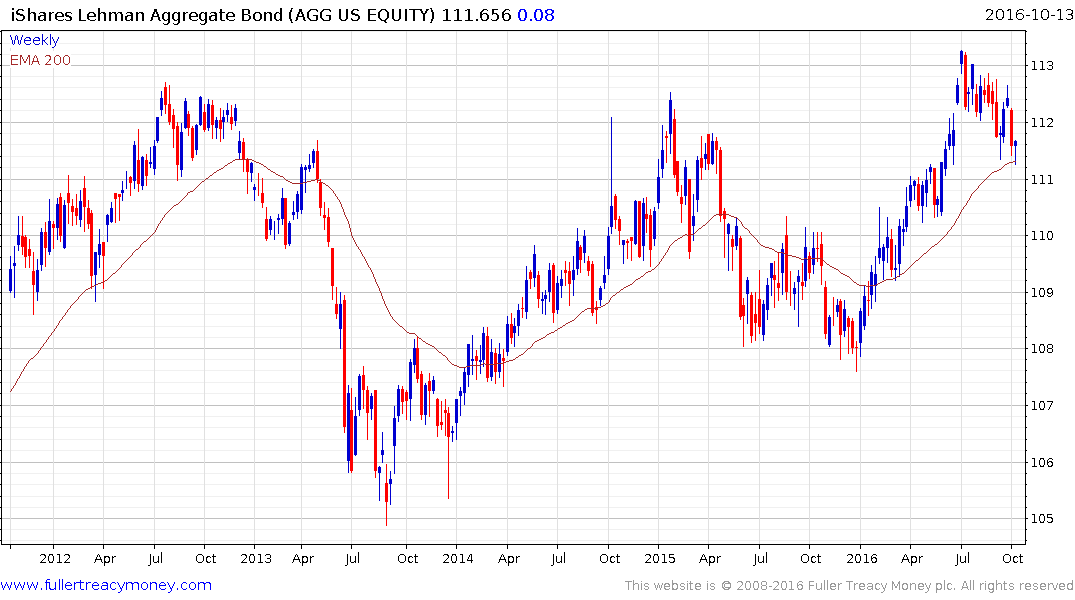

The iShares Core U.S. Aggregate Bond ETF (YLD 2.45%, Expense Ratio 0.05%) invests in all types of investment grade bonds from Treasuries to corporations and asset backed securities. It is now testing the region of the trend mean and the upper side of the underlying 4-year range. It will need to rally soon if medium-term potential for higher to lateral ranging is to be given the benefit of the doubt.

For US investors the tax advantages of municipals are something few people of means can ignore and their underperformance of late will be an issue for many wealth managers. The iShares S&P National Municipal Bond Fund (YLD 2.25%, Expense Ratio 0.25%) encountered resistance in the region of its historic peak from July and has now dropped to break the progression of higher reaction lows and is trading below the trend mean. It will need to stage an impressive rally to question potential for a further test of underlying trading.