How Long Can the Fed Keep the Boom Going?

Thanks to a subscriber for this article by Thorsten Polleit for the Mises Institute. Here is a section:

To keep the boom going, the central bank must keep interest rates below their natural levels. It cannot raise them back to “normal.” First and foremost, higher interest rates would make the boom collapse. The credit market would collapse, stock and housing prices would tumble, and the financial system and the economy as a whole would go into a tailspin.

One may ask: Why is the Fed then raising rates then? Perhaps the Fed’s decision-makers think that the US economy has overcome the latest crisis and higher interest rates are economically justified. Others might wish to tighten policy for getting the short-term inflation adjusted interest rate out of negative territory.

Be it as it may, the disconcerting truth is this: Fed rate hikes will close the gap between the natural interest rate and the actual interest rate level. This, in turn, amounts to putting a brake on the boom, bringing it closer to bust. It is impossible to know with exactitude at what interest rate level the US economy would fall over the cliff.

One thing is fairly certain, though: The US economy, and with it the world economy, is caught between a rock and a hard place. Maybe the Fed’s current rate hiking spree will bring about the bust. Or the Fed refrains from raising rates further and keeps the boom going a little bit longer.

The big question is how can the Fed raise interest rates and shrink its balance sheet at the same time, without having an adverse effect on the economic expansion it has worked so hard to achieve.

The bond market does not appear to believe the Fed can do both at once. That helps to explain why investors have been so unwilling to drive yields higher on the short end of the curve. I have sympathy with that view since the ECB contributed to Eurozone deflationary pressures when it shaved €1 trillion Euros from its balance sheet between 2012 and 2014. The Fed risks doing the same if it is too aggressive.

Right now the odds are stacked in favour of the Fed raising rates in June but if they are in fact intent on shrinking the balance sheet it is hard to imagine that can be achieved while also raising rates even further. That suggests the gradual pace of normalisation could be even slower than many people imagine.

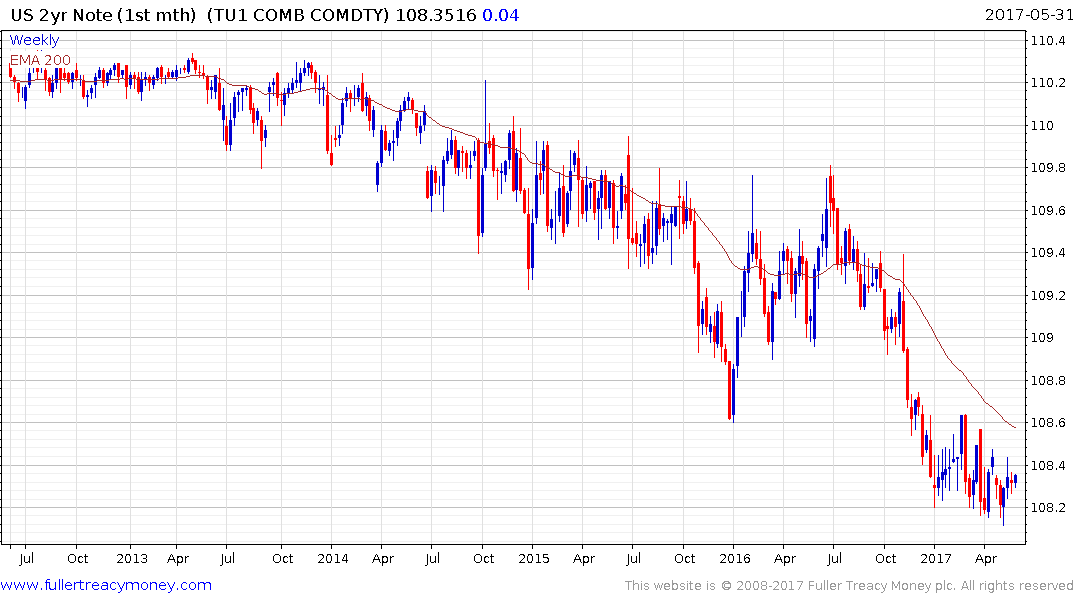

US 2-year futures continue to encounter resistance in the region of the trend mean and pulled back from that area again today.

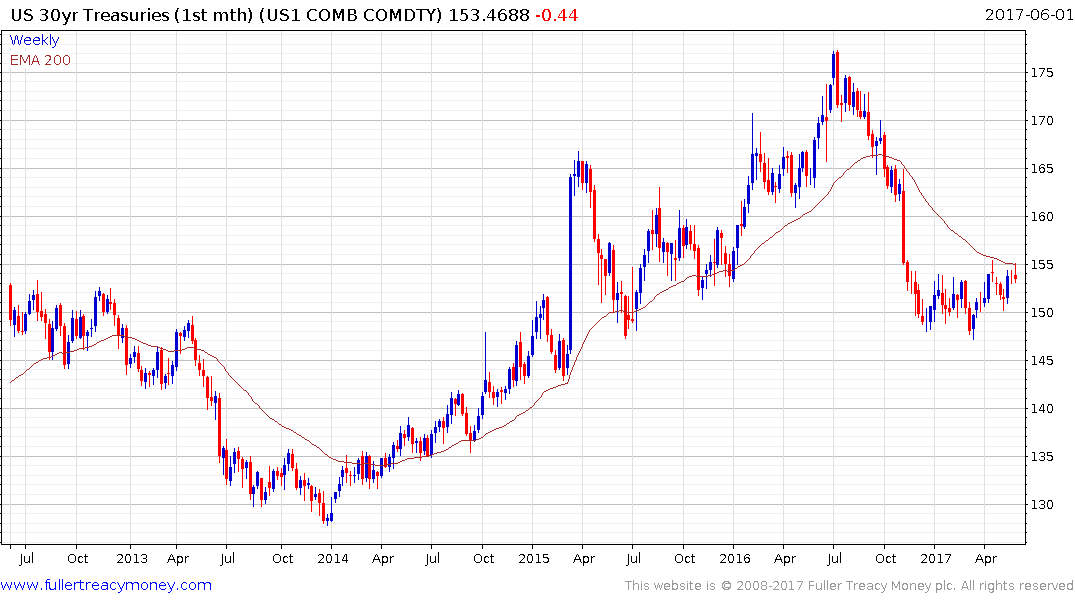

US 30-year futures pulled back from the upper side of a six-month range today to confirm at least near-term resistance in the region of the trend mean. A sustained move above it will be required to question medium-term supply dominance.

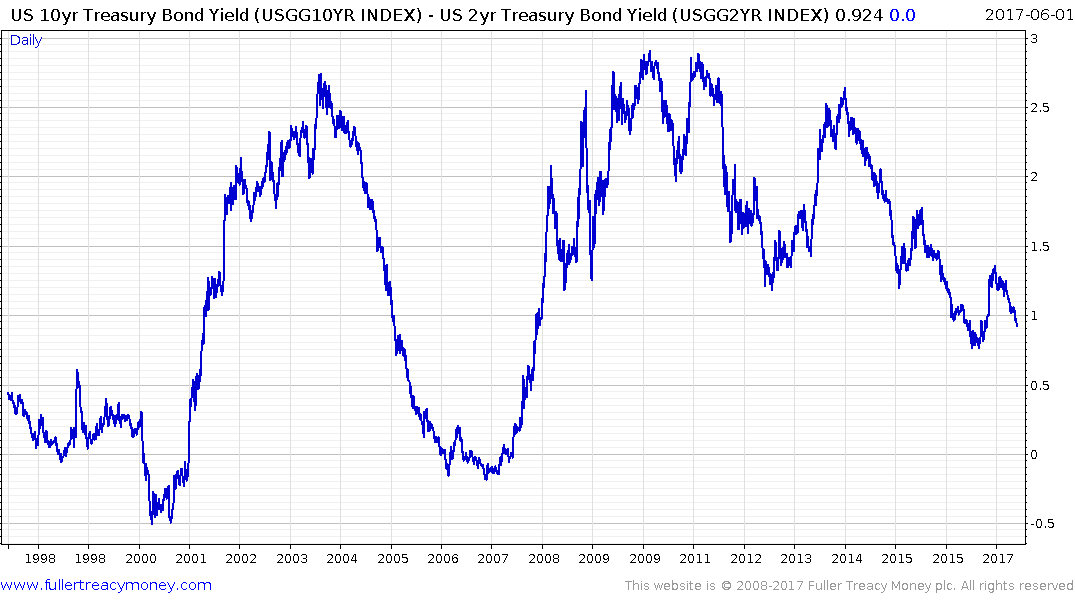

The fact the yield curve continues to flatten suggests the bond market is not particularly confident the Fed will succeed in normalising interest rates without a hiccup.