How Early Exercise Order Flow Impacts Equity Option Put/Call Ratios

Thanks to a subscriber for this article from the Cboe which may be of interest. Here is a section:

Historically, dividend related ITM [Ed. In-the-money] call exercises have resulted in some of the highest call volume days of the year, including March 15, 2012, when a record 9M calls traded in SPY, but changes to the clearing process since then have dampened that activity.

Mathematically, the decision to exercise a call or put early is related to the extrinsic value of the contract. For calls, if the dividend(s) amount exceeds the extrinsic value, a long holder is usually better off exercising. For puts, the decision is a bit more subtle, with extrinsic value compared to the carry cost on the strike. As U.S. interest rates have increased sharply to decade-highs this year, the cost of carry for deep positions has increased, while the selloff in many popular stocks has resulted in large blocks of deep put open interest. Unlike dividend-related call exercises, which tend to happen quarterly, put exercise dynamics may repeat daily if positions are open. In practice, put exercises are more common on Wednesdays based on the timing of settlement. Puts exercised on a Wednesday result in a stock sale on Thursday, which settles Monday.

Fortunately, early-exercise candidate call and put strikes for all listed products are calculated intraday and available in a subscription product on the Cboe DataShop.

A sample from the file for December 7 shows that all the active Amazon deep put strikes were considered optimal to exercise as of 2 p.m.

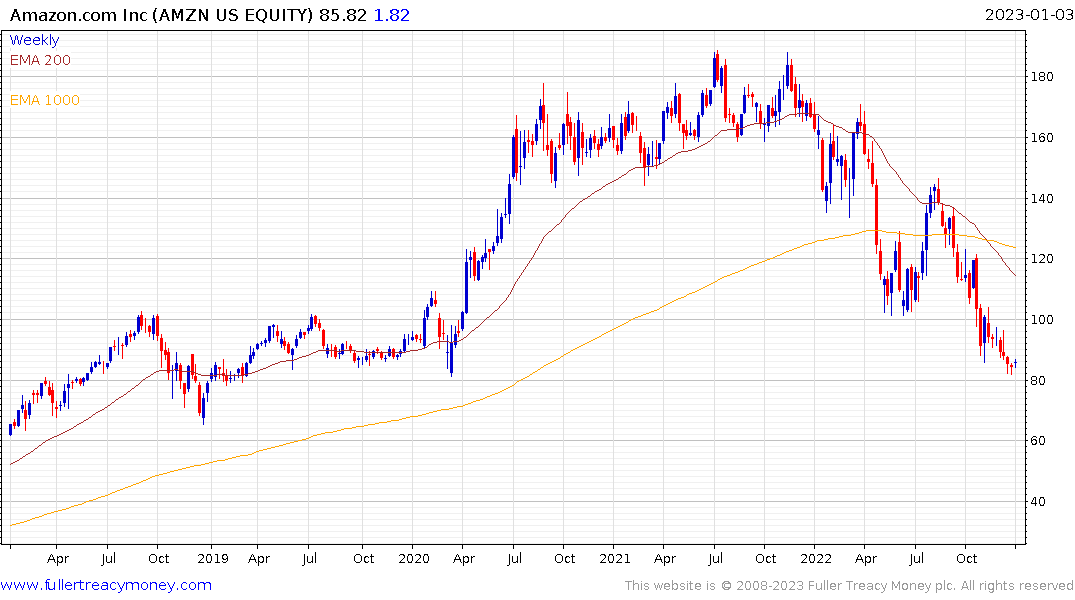

Large volumes of options traded in single stock names is a function of how much liquidity is still circulating the market. Massive volume in Tesla was a major factor in the stock’s ability to defy gravity in 2021. The opposite condition has been evident in Amazon, where outsized appetite for shorts has resulted in the share being among the worst performers in Q4.

The surge in demand for Amazon puts happened at a time when the VIX was not fulfilling its normal function as a hedge against S&P500 weakness. It is worth considering that the largest companies offered leveraged exposure to the major indices on both the upside and the downside.

The fact they occupy a decreasing weighting in the major indices suggests that condition will not last indefinitely. The S&P500 looks susceptible to additional weakness as it pulls back from the region of the 200-day MA.