Here Are Three Reasons to Short Australia's Dollar

This article by Ruth Carson and Michael G. Wilson for Bloomberg may be of interest to subscribers. Here is a section:

The Reserve Bank of Australia is forecast on Tuesday to keep its cash rate target at a record low 1.5 percent, where it’s been for about two years, as it endeavors to breathe life into the nation’s sluggish economy. The Federal Reserve in contrast has raised its benchmark seven times since December 2015 and said last week it remains committed to further tightening.

Australia’s 10-year bond yields dropped to more than 30 basis points below their U.S. peers at the end of July and the divergence is expected to keep widening. Markets are anticipating the RBA will stay on hold well into 2019, while the Fed is expected to raise rates another two times this year.

Positioning data backs up the gloomy assessment. Hedge funds and other large speculators shifted to a net short position on the Aussie of 23,995 contracts on July 24 -- the biggest bet against the currency in more than two years -- after being net long position as recently as May.

The Australian Dollar has historically been a high yielding currency so with interest rate differentials narrowing and pressure coming to bear on the commodity markets there is a logical argument for why it should be trading lower. The big question is how much of that argument is already in the price?

The spot rate had held a progression of higher reaction lows within its range between early 2016 and early 2018 which bore the hallmarks of support building following the collapse from the 2011 peak. However, the Australian Dollar failed to hold the breakout to new recovery highs in January and subsequently dropped to break the sequence of higher reaction lows. It has steadied of late but a sustained move above the trend mean will be required to signal a return to demand dominance beyond potential for short-term steadying.

Oil prices remains reasonably steady and generally speaking natural gas exports are tied to the price. Meanwhile iron-ore is exhibiting some interesting price behaviour. The China imports price is looking barely steady near the lower side of its yearlong range.

Meanwhile, the Chinese iron-ore futures prices are rebounding from the lower side of its range and has found support in the 400 area on multiple occasions since early 2016. They can’t both be right and that suggests speculation in the term spreads.

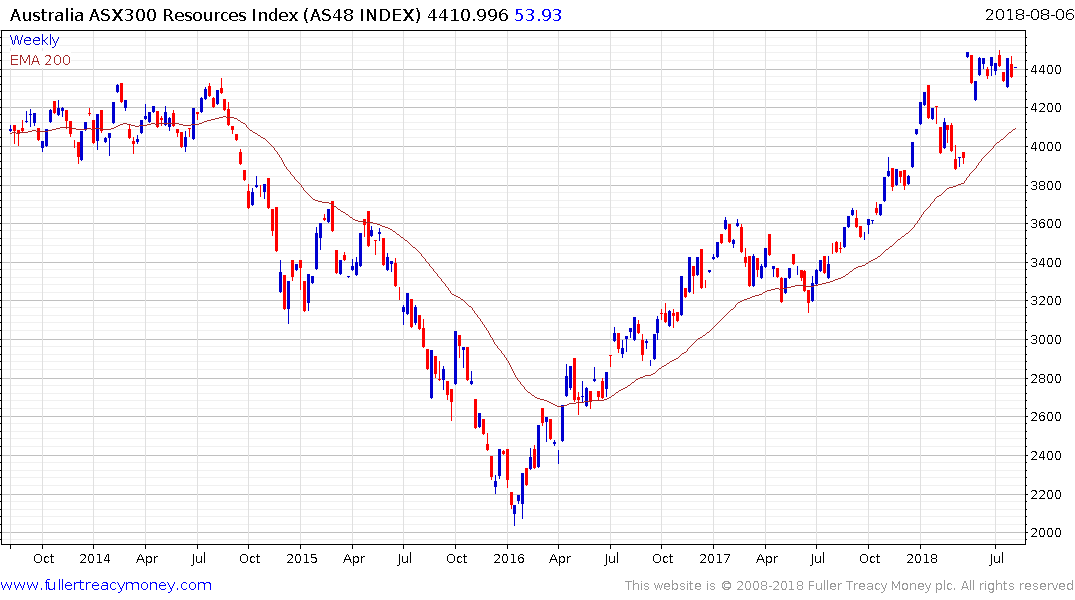

The S&P/ASX Resources Index remains in a reasonably consistent medium-term uptrend and a sustained move below the trend mean would be required to question medium-term scope for continued upside.

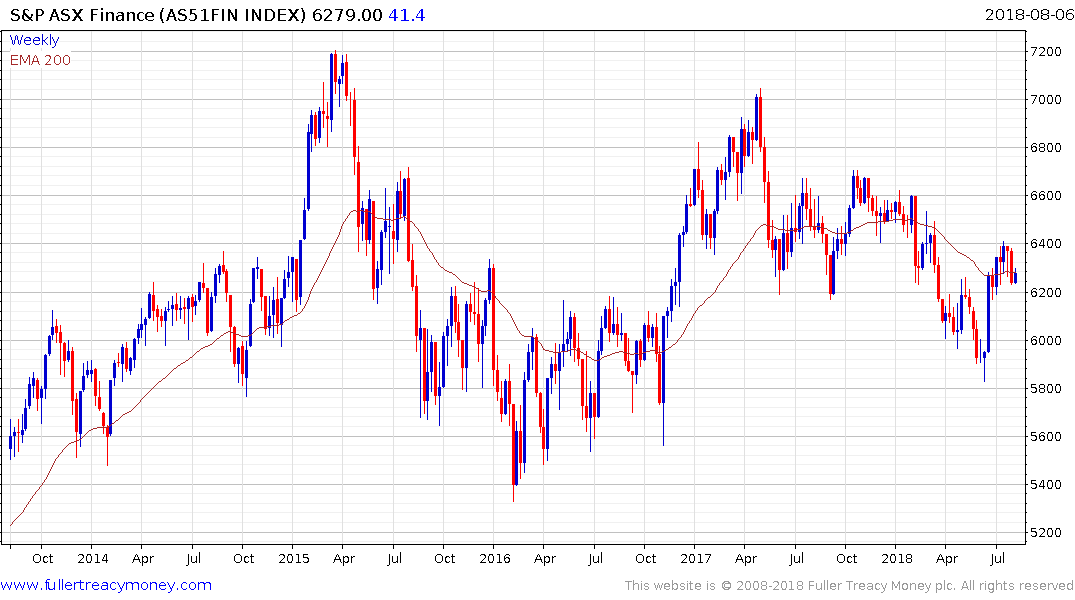

The S&P/ASX 200 Financials Index rebounded impressively to break the yearlong progression of lower rally highs and is now testing potential support in the region of the trend mean. The extent to which the Index can hold the majority of the rebound from the June low will signal how likely a return to medium-term demand dominance is.