Hands Tied and Swords Bent, Emerging Markets Battle the Dollar

This article by Srinivasan Sivabalan for Bloomberg may be of interest to subscribers. Here is a section:

But that’s not the ominous undertone. It’s about how the traditional fortifications of emerging markets -- strong oil and commodity prices -- are failing to protect developing-nation currencies from the onslaught of a stronger dollar.

Look at the chart below. In January, developing-nation currencies and commodities fell together and rose back in tandem. But this time, while the Bloomberg Commodity Index is extending gains, currencies have collapsed. This divergence suggests that a strong U.S. dollar is more decisive for risk appetite than commodity prices.

That’s bad news for countries such as South Africa and Russia. The ruble, for instance, is now moving in the opposite direction to oil even though it’s the country’s biggest export earner. Their usual positive correlation was destroyed by a four-day decline in the currency in the wake of enhanced U.S. sanctions.

Here is a PDF of the full article.

The Dollar’s rally is resuming with some of the most pressured emerging markets being forced to raise rates aggressively to stem declines. Argentina’s 40% repo rate is beginning to have the desired effect but it is one of a very small number of currencies that was able to squeeze out a rally against a resurgent Dollar today.

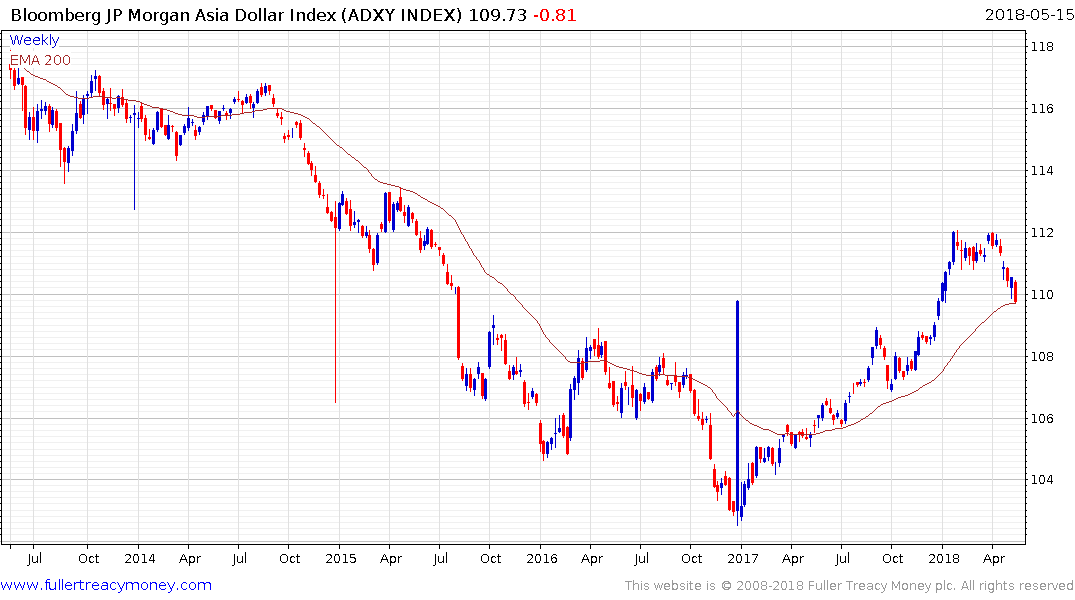

The Asia Dollar Index pulled back sharply to retest the region of the trend mean and will need to rally smartly to question potential for a break of the medium-term uptrend.

The US Dollar Index is now holding a move above the trend mean for the first time in a year. A clear and sustained downward dynamic will be required to question potential for additional upside.

The Latin America Dollar Index hit a new closing low today and a clear upward dynamic will be required to question potential for additional downside.

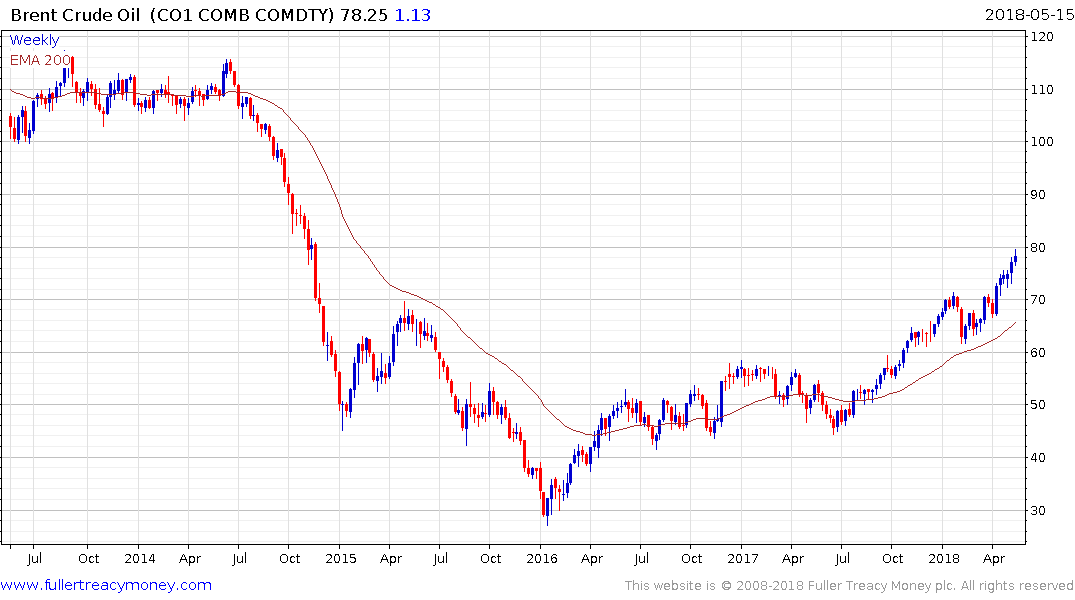

Crude oil prices might be short-term overbought but have so far remained resilient to more than intraday selling pressure. People are now starting to talk more openly about the inflationary pressures of high gasoline prices and the effect that is having on the cost of trucking goods around.

That is also part of the reason US Treasuries broke so emphatically above 3% today.

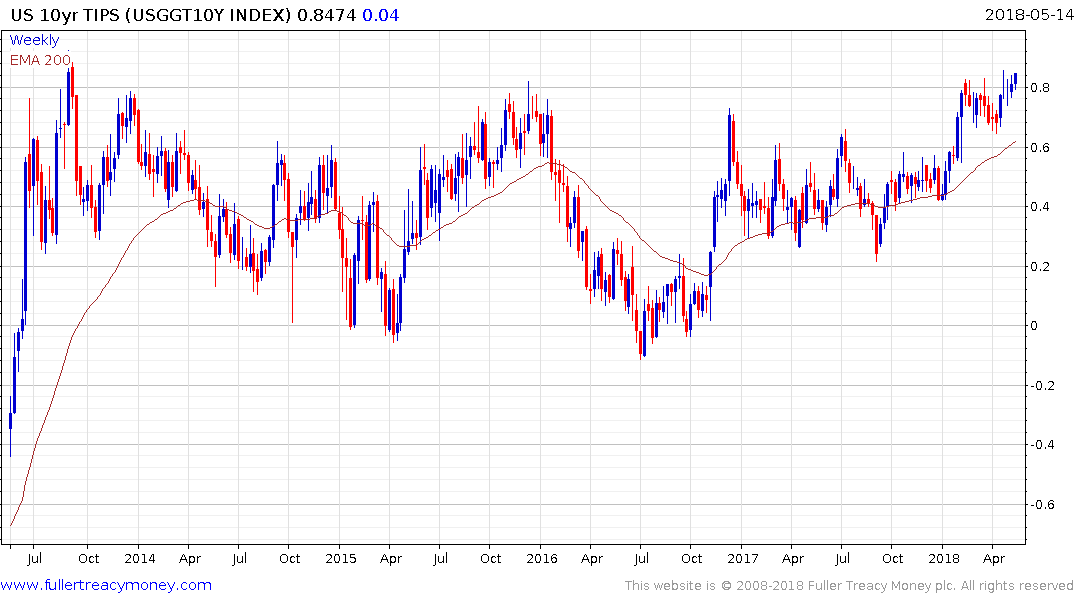

Additional supply has contributed to weakness in Treasuries but there is no new supply of TIPS scheduled. The fact 10-year TIPS yields appear on the cusp of breaking out points towards inflationary fears being priced in.

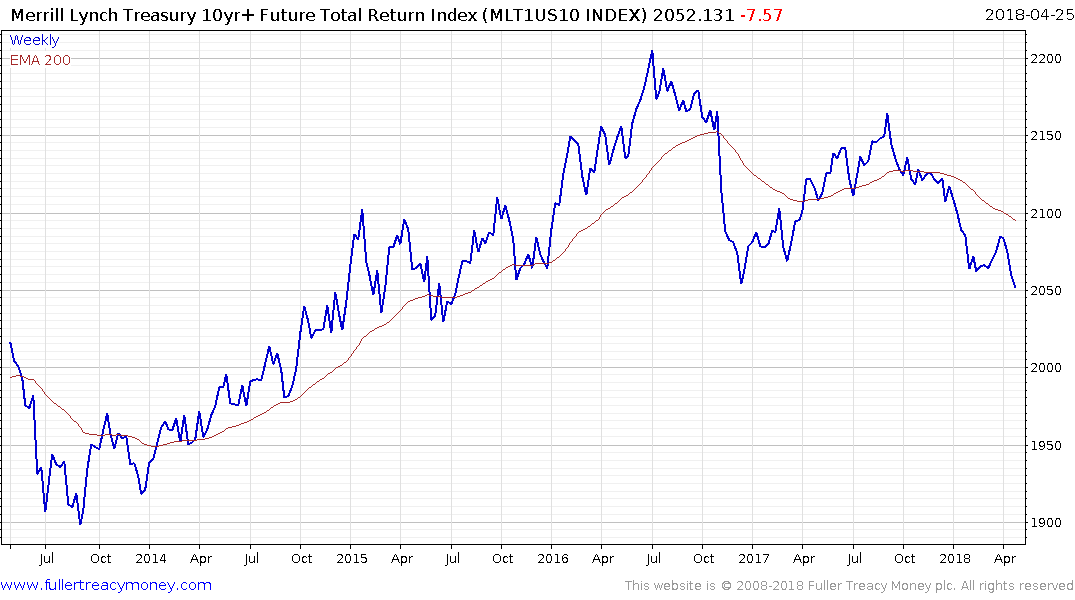

The Merrill Lynch 10yr+ Futures Total Return Index appears on the cusp of completing a Type-3 top formation which would confirm a major long-term change of trend.

Gold broke below $1300 today and needs a clear upward dynamic to signal a return to demand dominance.