Gundlach Says Bond Wipeout Just Beginning as Bulls Rush for Exit

This article by Edward Bolingbroke, Liz Capo McCormick and John Gittelsohn for Bloomberg may be of interest to subscribers. Here is a section:

With a Federal Reserve seemingly committed to raising interest rates a third time this year and speculation the European Central Bank could announce a tapering of bond purchases by the end of the year, the fundamentals aren’t encouraging. As yields are now approaching key technical marks that could trigger a fresh flush out of long-end bulls, the risk is building that Treasury yields go even higher.

Ten-year Treasury yields are on course to move “toward 3 percent” this year, Gundlach said in an emailed response to questions. There has “been no justification for the divergent policies in the U.S. versus Europe given economic fundamentals,” he said - a point he has made previously.

A 10-year yield at 3 percent would put Treasuries in “definitive” bear market territory, Gundlach added. The yield traded as high as 2.39 percent Thursday, just ahead of a key retracement level at 2.42 percent, coinciding with the May high.

“People this year had been buying long-dated Treasuries and other sovereigns as the hedge to their equity portfolios and that’s why this unwind is so ugly,” said Peter Tchir, head of macro strategy at Brean Capital LLC. “They are losing money on both the equity and debt side now, and are bailing out of their long-dated Treasuries.”

The risk parity trade, which has been among the most favoured by macro traders over the last couple of years, where volatility in equities is counterbalanced by equal but opposite positions in bond volatility, is coming under pressure.

So far, the movements in equities have been relatively minor while the sell-off in the long bond has only been underway since last week. However, these types of trades are at risk both from bonds and equities moving in the same direction and upticks in volatility that are not easily hedged.

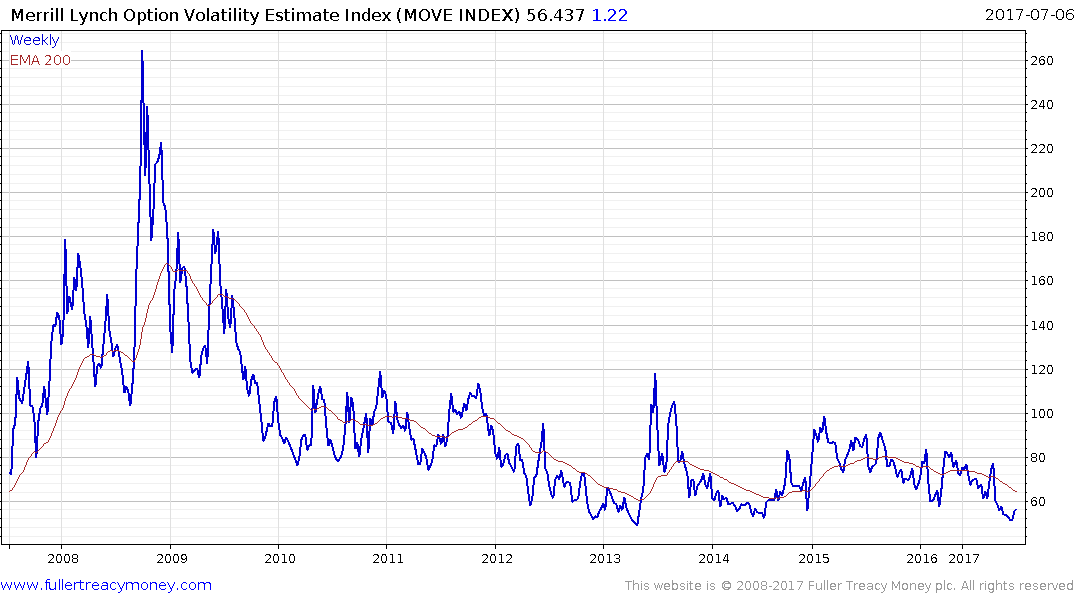

The Merrill Lynch Option Volatility Estimate (MOVE Index) is a yield curve weighted average of normalised implied volatility on 1-month Treasury options across maturities. Like its equity cousins it is testing historic lows but there is increasing evidence of at least near-term support forming.

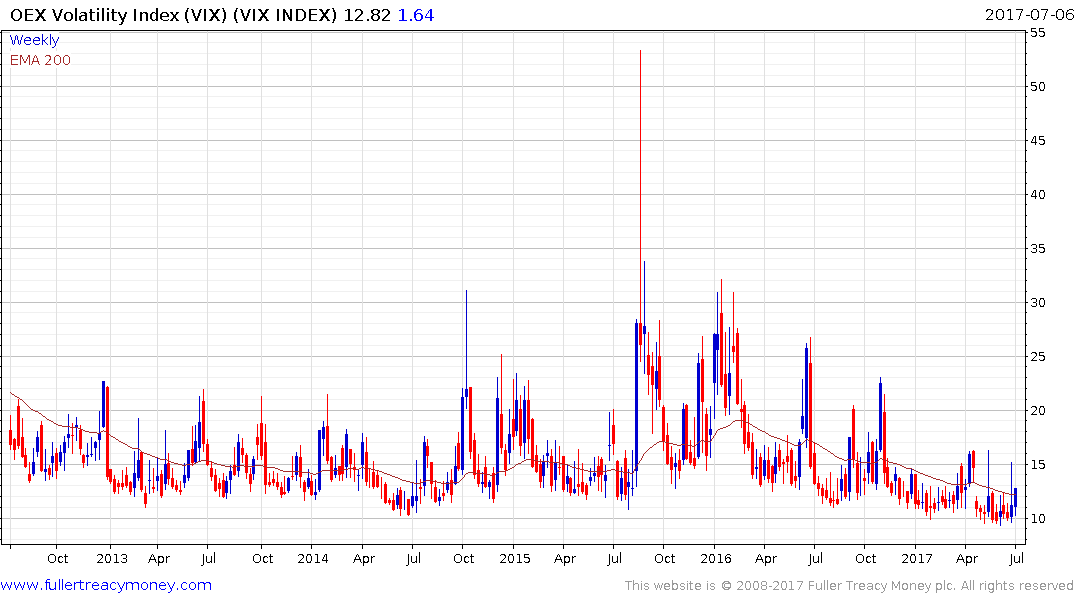

The VIX Index firmed from above the 10 area again today. A sustained move above 15 will be required to signal more than a temporary squall.

Meanwhile the S&P500 has trended higher in a consistent manner since early 2016, with a series of ranges one above another. It will need to hold the 2400 region if that sequence is to be sustained.