Goldman Sachs Asked Two of the World's Best-Known Economists If U.S. Stocks Are in a Bubble

This article by Julie Verhage for Bloomberg may be of interest to subscribers. Here is a section:

When asked how worried he is about the prospects for the market over the next six months, Shiller says that his concern has risen with the market and that there could very well be a correction in the next year, although the timing of such market events is inevitably difficult. He advised people to both save more and diversify their investments because their portfolios probably won't do as well as they had hoped — even over the longer term.

Next, Goldman talks to Wharton professor Jeremy Siegel, who has continued to be on the bullish side with his buy and hold strategy.

Siegel says he believes stocks are only slightly above their historical valuations today and the level is "completely justified" due to low interest rates. To those that claim the stock market is in a bubble, Siegel says he is in complete disagreement. "In no way do current levels that are nowhere near those highs (of March 2000) qualify as a bubble," he says.

Siegel adds that there isn't much that would dissuade him from holding equities over the medium term and recommended investors allocate 50 percent of their portfolios to the U.S., 25 percent to non-U.S. developed markets, and 25 percent to emerging markets.

Of course, Shiller and Siegel are also well-known friends so there is at least one place where they are in agreement and that is the bond market. Both economists said it was fair to say bonds are overvalued and some concern is justified, although neither of them would commit to calling it a bubble. Shiller said that historically the bond market doesn't tend to crash like the stock market. Siegel steered away from calling it a bubble due to his expectation that both short- and long-term rates will remain low.

The answer to the question on whether stocks are expensive will in many respects hinge on whether one takes an absolute or relative comparison. In absolute terms we can see that valuations are higher than they were in 2008 but this does not tell us how expensive they will become. The CAPE is elevated for example but does not tell us if it will move higher.

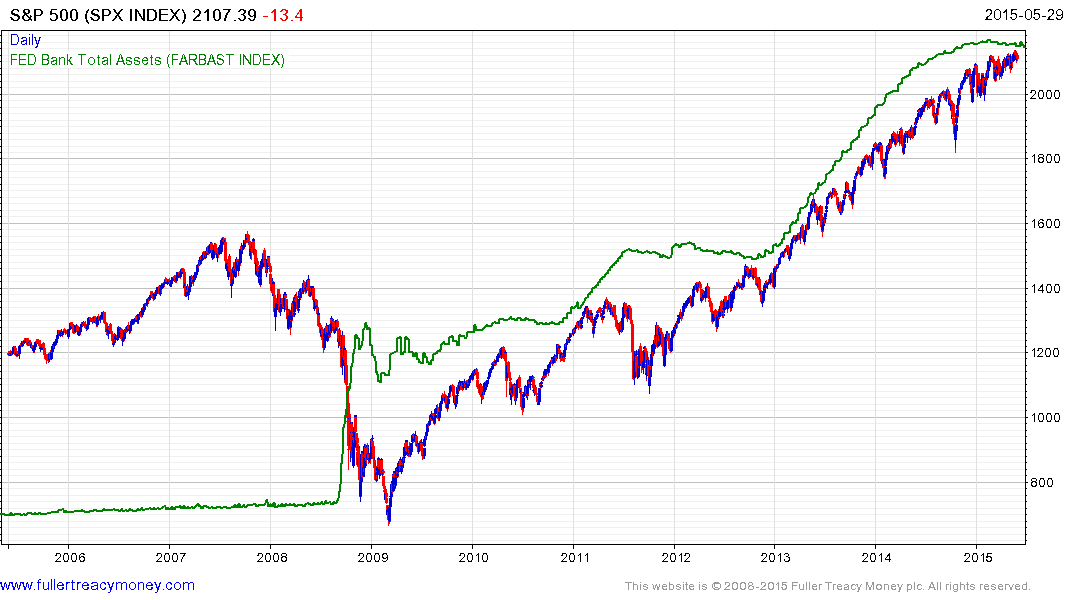

Perhaps most important is that interest rates are low and liquidity abundant. If stocks are valued with this in mind then the high correlation between the S&P 500 and the size of the Fed’s Balance Sheet makes more sense.

I do not believe the wider US stock market is in a bubble. We are a long way from the mania that is associated with such a condition. However there is no denying that the rally since 2009 has been liquidity fuelled. The lacklustre performance evident on the S&P500 is in no small part due to the fact that the Fed’s quantitative easing program ended in October.

Capital is both global and mobile so another way to look at the market is on the relative prospects for outperformance. Why should I wait and see what happens in the USA when liquidity fuelled rallies are taking place in China, Japan and Europe? In these terms Wall Street is in need of a catalyst to reinvigorate investor appetite. Accelerating M&A activity in the technology sector has so far not been enough. Eric Rosengren today saying that the US economy is not strong enough to raise rates might be more important. Persistence of the low interest rate environment will allow companies to continue to borrow at attractive levels in order to refinance and buy back shares.

A sustained move below the 200-day MA, currently near 2040, would be required to question the consistency of the S&P500’s advance.

Back to top