Fed Reverse Repo Facility Usage Soars, Rates Low at Year End

This article by Liz Capo McCormick for Bloomberg may be of interest to subscribers. Here is a section:

The Fed allotted $9.4 billion in reverse repos in the inaugural test on Sept. 26 and the facility has averaged $11 billion a day prior to this week. The collateral for the transactions has been limited to Treasury debt.

Fed policy makers, while still buying bonds to support the economy, have also been developing methods to eventually help withdraw record monetary accommodation. Along with raising the overnight bank lending rate, Fed officials have said they may use tools including reverse repos to withdraw or neutralize cash in the banking system.

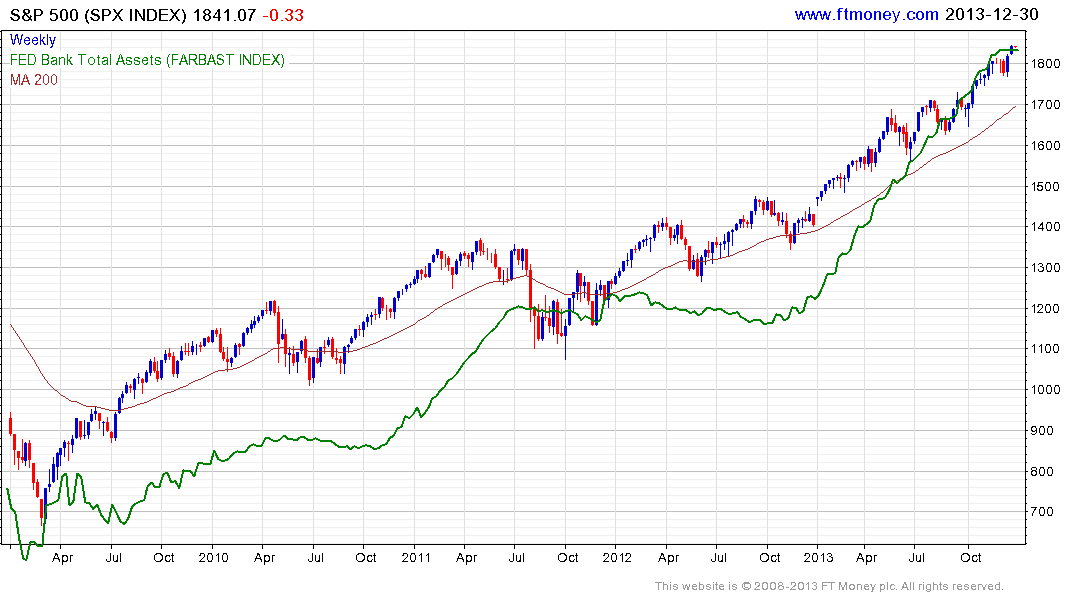

The Fed’s balance sheet currently stands at a tad over $4 trillion and perhaps more importantly continues to trend higher. Considering just how much money has been created over the last five years and its role in fuelling asset price inflation, it is reasonable to assume that any significant change to the status quo will put funding mechanisms and leveraged participants under pressure.

The correlation of the S&P500’s performance and the increase in the size of the Fed’s balance sheet is currently at 0.146 and has been improving all year. At FT Money we have referred to the stock market’s rally as liquidity fuelled since 2009 and this remains very much the case today.

As awareness of the role of liquidity has increased, investment managers have experienced career risk by expressing concern at the role of liquidity in the stock market’s advance. In the current circumstances, the only way to have kept pace with the benchmark this year would have been to get long and stay long. This has a conditioning effect on sentiment and means that some of the investors who followed this policy will eventually have a harder time selling.

Provided the Fed’s balance sheet continues to expand, the benefit of the doubt can probably continue to be given to the stock market’s medium-term uptrend. However, when the Fed eventually begins to curtail and reverse the expansion of its balance sheet, it would not be surprising to see the S&P500’s uptrend lose consistency.

Back to top