Extracting Growth Alpha in Emerging Markets

This report from Jennison Associates may be of interest to subscribers. Here is a section:

Generally speaking, an investor’s primary motivation for making a portfolio allocation to emerging market equities is the desire to tap into superior structural growth. However, equity market returns rarely correlate tightly to economic growth. There are many attractive secular growth companies in emerging markets—and they exist regardless of the economic growth conditions of their domestic economies. Investors wanting to tap into the powerful long-term benefits of superior structural growth trends can benefit from seeking out highly active strategies. In our experience, a strategy succeeds by continuously seeking out innovative companies with superior growth trajectories. A clear and consistent investment philosophy and repeatable investment process can help to ensure that a portfolio reflects bottom-up decisions that incorporate the superior growth available in EM equities.

The growth opportunity set is bigger than is generally thought. EM companies face challenges and problems different from those of their developed market counterparts, but their distinct circumstances often spur them to innovate and disrupt existing practices. EM companies are moving up the value chain, from export-oriented business models built on low-cost labor and cheap manufacturing to higher-value-added businesses based on technological and scientific innovation. Low recognition of these dynamics by investors and indexes creates an opportunity for growth-minded investors. Add to the mix companies that execute well to exploit a superior economic growth backdrop, and the opportunity set expands.

Here is a link to the Subscriber's Area.

China’s success in developing domestic champions has been truly impressive and they are now among the largest companies in the world by market cap and revenue. Success in expanding internationally has been limited in the technology sector to the Chinese diaspora because the global market tends to be much more competitive than the sheltered environment domestically.

As the international community becomes progressively more wary of the Communist Party, it is arguable how much further these companies can grow beyond the confines of the Chinese community. WeChat censoring the Prime Minister of Australia, India expanding the number of banned Chinese apps, the impending demerger of TikTok and the questions over China’s control of Huawei all suggest generating alpha from China’s tech giants is going to be more challenging in the next decade.

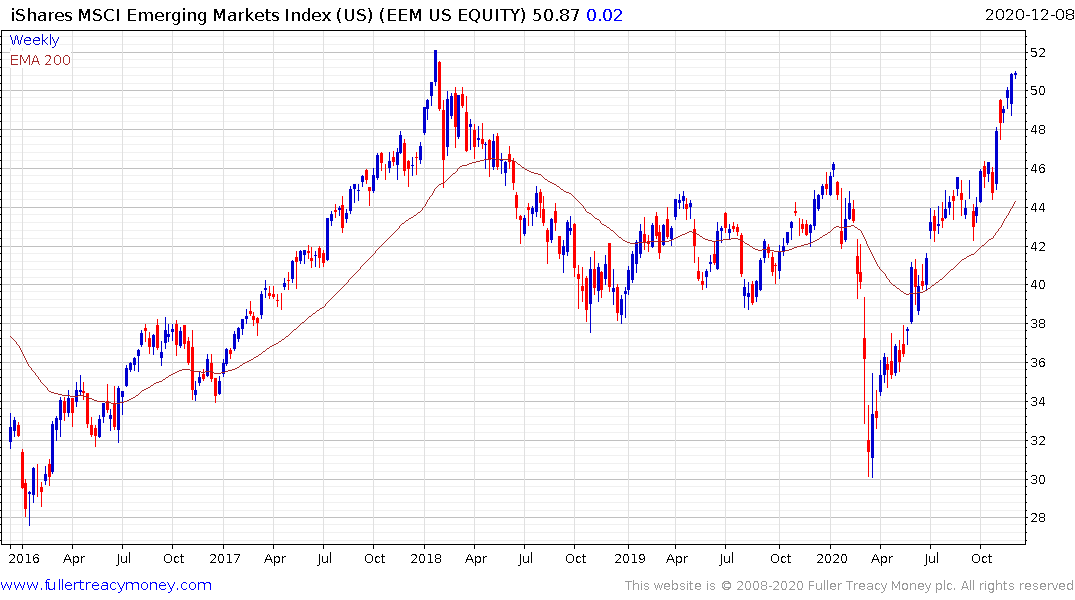

Tencent represents a significant weighting in the MSCI Emerging Markets Index. In many respects it is the equivalent of Apple for the Nasdaq-100. The share remains in a reasonably consistent uptrend but will need to continue to hold the region of the trend mean during reactions if the benefit of the doubt is to be given to the upside.

Meanwhile, the continued evolution of the middle class in Asia remains a high probability outcome. However, the next decade is much more likely to be an India, Indonesia, Vietnam, Thailand and Philippines led story than a China one.

Barings International Umbrella ASEAN Frontiers Fund is an institutional fund with high minimums but its performance confirms the trend of outperformance in high growth Asia ex-China.