Entering The Connected Life Era

Thanks to a subscriber for this report from Deutsche Banks which may be of interest to subscribers. Here is a section:

With all the innovation happening across the software layers mentioned above, and all the new ways to engage with users across these many new device types in the Connected Life era, the next logical question to ask is “what is this all worth to an ecosystem?” Below we attempt to answer that question from the standpoint of software, services and advertising. Importantly, we do not attempt to quantify the hardware opportunity. What we attempt to quantify is once Apple or Google or Xiaomi has a user in its ecosystem, what kind of ARPU is likely to be generated from all the software, services and advertising opportunities.

As we mentioned above, given how engagement models are changing rapidly in the Connected Life era, we firmly believe the right approach when assessing the monetization potential per user is measured in terms of sessions (not time spent). We further analyze the respective monetization potential for different engagement models (push vs. pull vs. paid) on various devices. Breaking down user sessions based on commercial intent and the ad engagement approach on various devices is important because different engagements and behaviors monetize at different rates. For example – a search on Google for a commercial term carries a very high eCPM, whereas a newsfeed ad on Facebook or Twitter may not carry the same level of user intent. If we extend to ad formats we are likely to see in the Connected Life era like push notifications and card-based offers, displayed on smaller screens, the commercial intent of these engagements is going to fragment further. Lastly, a number of new services are being introduced on mobile devices for the first time, and those subscriptions and in-app-purchases carry very high revenue per session and eCPM equivalent rates. For example, if a user pays $10 per month for a Spotify subscription, and accesses the service three times per day (~100 times per month) each session would amount to around $0.10, or the equivalent of a $100 ad eCPM.

Here is a link to the full report.

The evolution of the internet experience over the last decade has been nothing short of remarkable and is still having profound effects on how we are marketed to and how people respond to these additional stimuli.

Young people spend much more time on Facebook, Twitter, Instagram, YouTube, Amazon Prime etc than they do consuming conventional media. Since they represent the prime 18-34 age bracket prized by advertisers, companies are eager to capture their attention.

This is a rapidly developing sector so we can anticipate continued aggressive competition. However, as anyone who has moved from an Android to Apple device or vice versa can testify, you need a good reason to migrate from one ecosystem to another.

A great deal of good news has already been priced into related shares.

Google (Est P/E 19.52) lost momentum from early this year following a particularly impressive advance in late 2013. It has dropped over the last month to test the $500 area and while steady today, a sustained move back above the 200-day, currently near $530, would be required to begin to signal a return to demand dominance.

Apple (Est P/E 13.92, DY 1.74%) continues to unwind the overbought condition relative to the 200-day MA. It steadied somewhat today but a break in this month’s progression of lower rally highs will be required to question potential for some additional easing.

Facebook (Est P/E 44.99) has seen its multiple contract steadily from its IPO valuation as earnings have improved. The share has been ranging below $80 since August and will need to continue to find support in the region of the 200-day MA on reversions if medium-term potential for continued higher to lateral ranging is to be given the benefit of the doubt.

Twitter (Est P/E 372.5) has failed to deliver on the hype of its IPO and has been drifting back towards its May low near $30 over the last three months. A break in the progression of lower rally highs will be required to begin to signal a return to demand dominance.

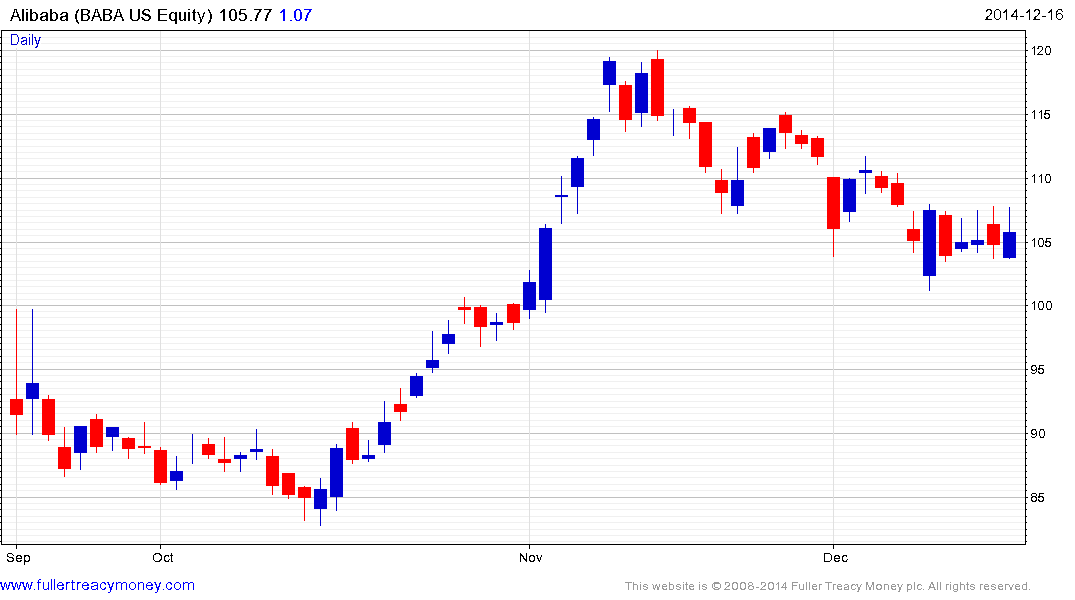

Alibaba (Est P/E 49.95) found support last week in the region of the psychological $100 level and a sustained move below it would be required to question potential for additional higher to lateral ranging.

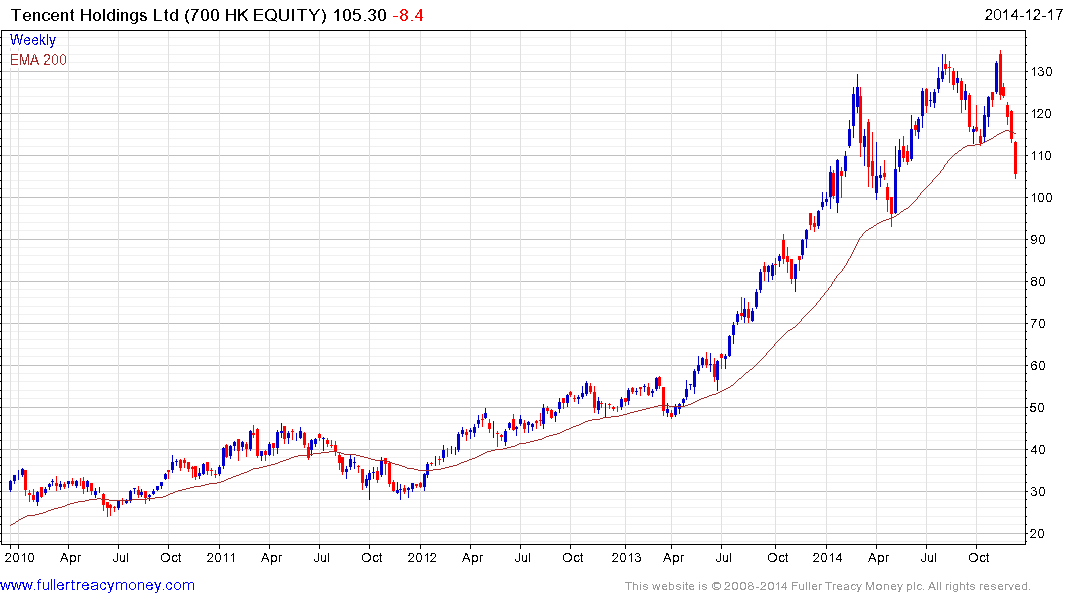

Tencent (Est P/E 32.87, DY 0.23%) lost momentum following an accelerated advance that rolled over in February. It failed to hold the breakout to new all-time highs in November and has now dropped to break the progression of higher reaction lows and the 200-day MA. While somewhat oversold in the short-term, a sustained move back above HK$120 would be the minimum required to begin to repair the damage done to the consistency of the trend.

Back to top