Emerging Markets Are Hot, Except for China

This article by Mia Lamar and Rachel Rosenthal for the Wall Street Journal appeared in Saturday’s edition but the authors might have wished they waited another day before publishing. Here is a section:

The wariness partly reflects how unnerved global investors remain by markets that have proved exceptionally unpredictable, even by emerging-market standards. After surging 60% in the beginning of last year, Chinese stocks tipped into a selloff that sent Shanghai’s benchmark index down as much as 41% from June to August. The index rebounded briefly last fall, then plunged 23% in January. The yuan, meanwhile, logged a 5% loss against the dollar in 2015, following an unexpected devaluation one year ago that helped to spur enormous outflows of money as panicked Chinese sent cash abroad.

Many investors say they are disturbed by steps China has taken to tame market convulsions, from heavy-handed currency intervention and the buying of shares by state-backed funds, to allowing widespread trading suspensions of shares and blaming “malicious” forces for stock-price falls.

Others say they remain concerned about China’s economic slowdown, and suspect conditions may be worse than official figures suggest.

Chinese officials have stressed measures by Beijing to address the concerns of global investors, and played down concerns about growth. “The Chinese economy is a ‘stability anchor’ for the global economy,” Premier Li Keqiang said last month. “Prophecy of China’s economy heading for a hard landing is rarely heard now.

Many of the limitations imposed on the Chinese market have been aimed at inhibiting speculation following a particularly tumultuous period in 2015. That is a condition which is in sharp contrast to the environment on a number of other international indices.

Chinese regulators messed up the launch of options trading, and timing its debut with the opening of the Shanghai – Hong Kong connection only exacerbated the short term mania. In trying to avoid a crash they threw every measure available to stem the decline and there is plenty of evidence over the last six months that the 3000 level on the CSI300 is being defended.

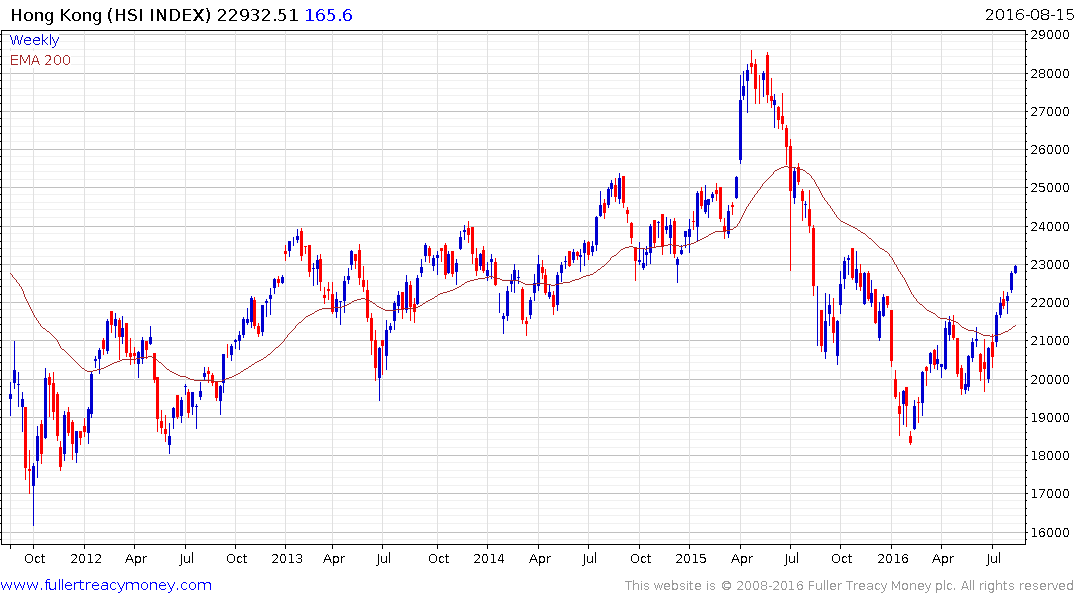

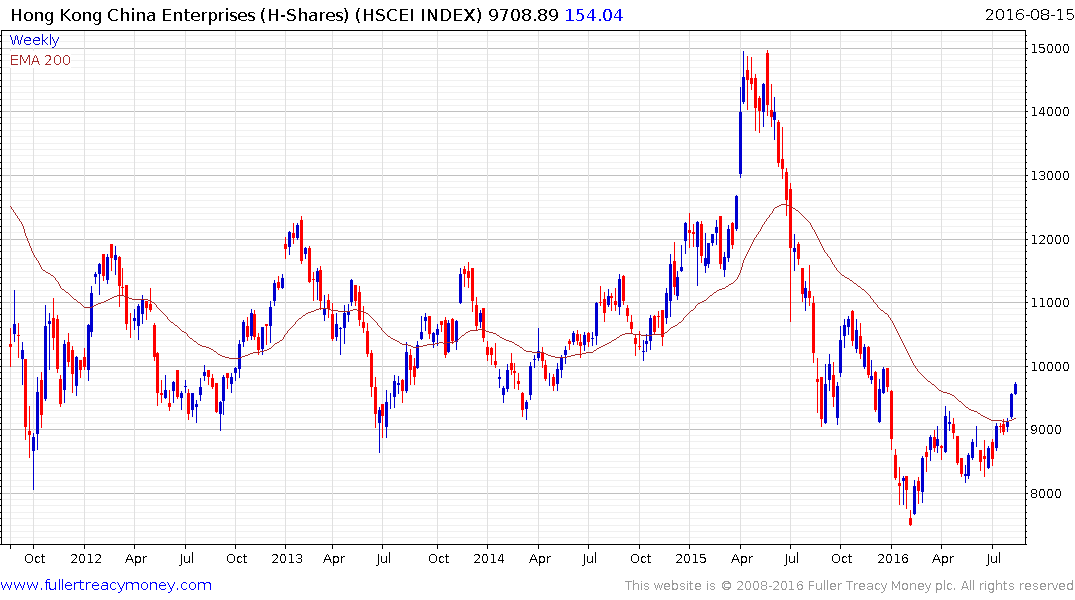

Taking all of the concerns expressed in the above article, with the slew of factors designed to inhibit volatility, the Chinese market has been a relative laggard for much of the year to date. However Hong Kong has some of the lowest valuations for a large cap market in the world. The Hang Seng Index trades on an historical P/E of 11.92 and yields 3.56% even though it has rallied impressively over the last two months. The China Enterprises Index (H-Shares) trades on an historical P/E of 7.66 and yields 3.81%.

Both indices have broken medium-term progressions of lower rally highs as they play catch up with both regional and global indices. They have been given an additional push today with speculation that the long awaited Shenzhen – Hong Kong stock market connection may be close to being finalised.