Email of the day on when it is best to hold cash:

I’d love to join you in China. I’ve not been there since 1996 but went frequently between 1983 and 1990. Never made money there but that did not quell my belief in China and its people. Since my last email some three months or so again when I suggested that it might make sense to hold more cash, you have (appeared to me) to become increasingly concerned about stretched values and tightening credit markets. I still hold very little cash having made the mistake of reinvesting much of what I had earlier raised. Like a rabbit in the headlights, I’m currently paralysed but feel fairly certain the sensible thing to do would be to hold cash and wait patiently. I doubt if I shall actually be able to do that. My interpretation of your views today is that you think we could see a sharp downward move in markets due to credit tightening, China and global political manoeuvring but that long term a secular bull market remains in place. What you don’t say is whether you believe it’s best to sit tight in equities or lighten, if not eliminate, equity positions and hold cash. Perhaps there’s no reason why you should. However, at times like this, I wish I had a subscription model business like yours and did not actually have to rely on my investments!

Thank you for this email and I have no reservations saying my family enjoy visiting China but we have no desire to live there. Guangzhou is my favourite city not least because of the quality of the food, friendly people and warm weather.

Your email raises a very important point about when to raise cash. First of all, however, I would like to dispel any illusion about whether our interests are aligned. A subscription business is only effective as long as it has subscribers. The only way it can survive therefore is to generate something of value, that is not easily found elsewhere, and to provide it to as wide a field as possible. We do no marketing, relying primarily on word of mouth. Therefore, I have a very clear interest in you doing well from your investments.

Being highly liquid at this stage suggests you believe the highs posted in January are at least medium-term in nature and that the risk of a deeper pullback, which would offer a much more attractive entry opportunity outweighs the potential that the initial assumption is incorrect. I think you are a little early in making that assumption, particularly without evidence of top formation completion but there is no denying that we are late in the medium-term cycle.

I believe what we are currently seeing is a medium-term correction that could last for anything from six to eighteen months. The fact that both the Nasdaq-100 and Russell 2000 have broken out to new highs and have, so far at least, held those moves suggests the correction might be on the shorter side of that timing window.

I believe I’ve been very clear since Xi Jinping became president-for-life that China deserves an additional risk premium. That market is deeply oversold right now but it deserves to trade on a similar multiple to Russia based on the condition of governance. That is where I see the greatest risk and that is even before we think about the knock-on effect of trade wars.

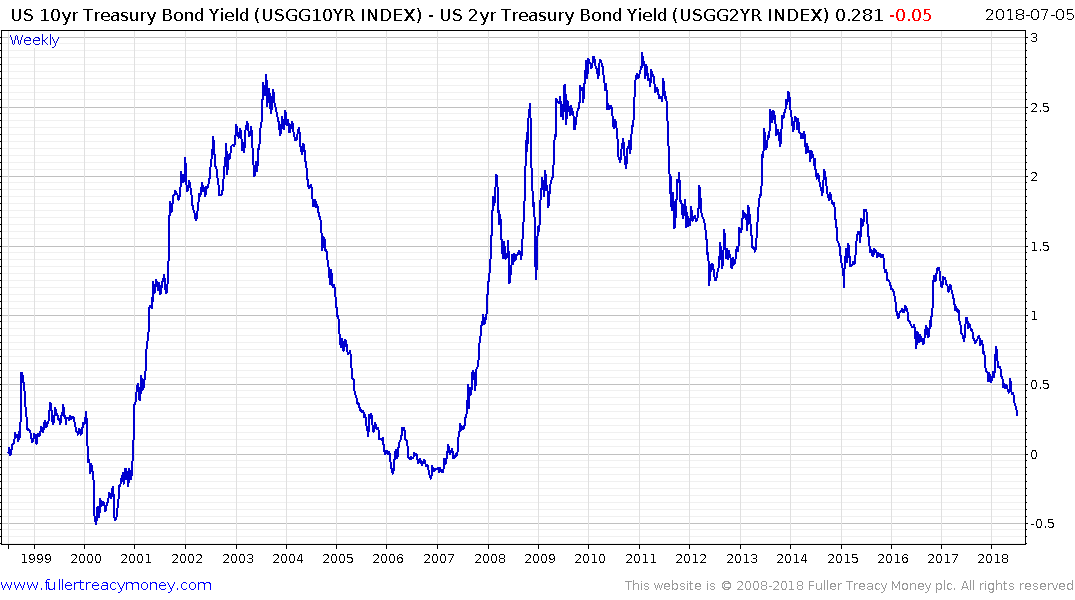

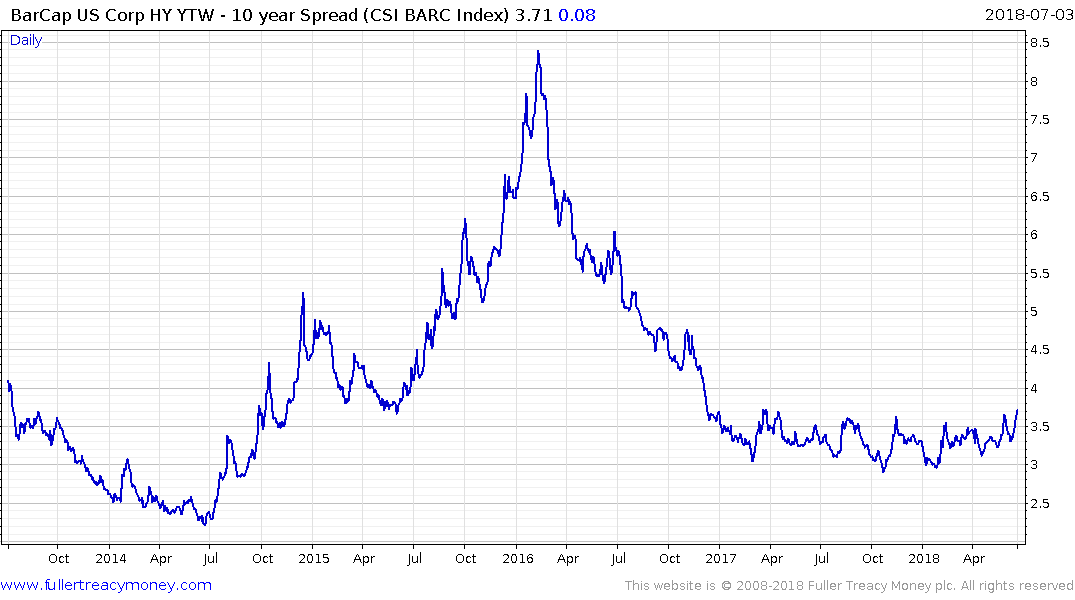

There is no doubt that credit conditions are tightening. Central bank balance sheets are, on aggregate, declining. The US Treasury yield curve spread is contracting rapidly. High yield spreads have been trending higher in Europe since December and broke out in the USA this week. Global banks sector indices are weak or trending lower.

Importantly, the S&P500 Banks is, so far, holding the bottom of the range, the KBW Regional Banks Index is steadying in the region of the trend mean and the Australian banks appear to be in the process of breaking medium-term downtrends.

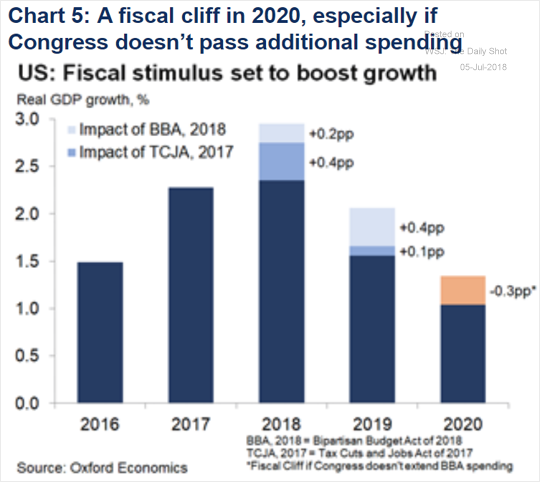

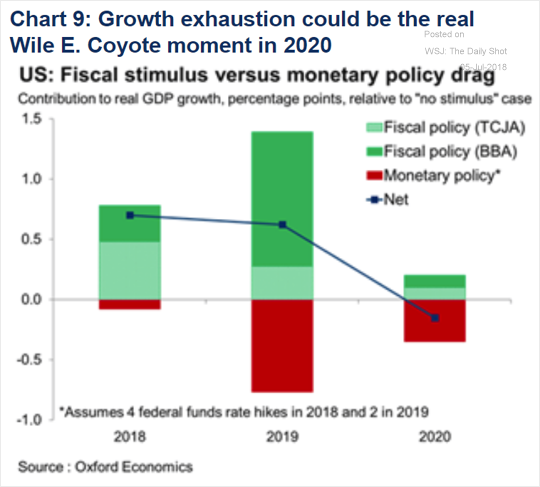

One might argue that the USA is outperforming right now not so much because of American exceptionalism but because the fiscal stimulus is still helping to propel the domestic economy and that is attracting inward investment from all over the world. In turn that is leeching flows away from just about everywhere else. However, the bump from stimulus will have run its course by the end of next year.

Let’s talk about the biggest risk from going to cash right now. It’s that we get an acceleration on the upside. The yield curve spread went negative in early 2006 but the market did not peak until October 2007 when it was almost 30% higher.

In recent videos I’ve described the Nasdaq-100 holding the 7000 level as the best of all possible scenarios. If its reaction is limited to such a small pullback then a further concentration of speculation in the FAAMNG stocks could result in the Index taking another leg higher. If that market accelerates then it will only further enhance bullish sentiment towards the “digital economy” while the tightening of financial conditions will become even greater and then you would have a recipe for the kind of pullback you are worried about sitting through.

Alternatively, the Nasdaq-100 does not hold the 7000 level and pulls back to test the trend mean. If it does post a failed upside break then we can conclude there is a surfeit of supply above that level and we know that people are anxious so stops have already been tightened. That holds out the prospect of a somewhat lengthier, more volatile trading environment. Quite how much financial conditions tighten would likely influence just whether that then represents a top.

Back to top