Email of the day on the yield curve spread:

Article in yesterday’s NYT. Is this the predictor of a recession that will follow trade wars?

Thank you for this article which may be of interest to subscribers. Here is a section:

There is an argument to be made against reading too much into the yield curve’s moves — and it hangs on the idea that, rather than the free market, central banks have had a big influence on both the long-term and short-term rates.

Since the last recession, central banks bought trillions of dollars of government bonds as they tried to push long-term interest rates lower in order to lend a helping hand to the economy.

Even though they’re reversing course now, central banks still own massive amounts of those bonds, and that may be keeping long-term interest rates lower than they would otherwise be.

Also, the Federal Reserve has been raising short-term interest rates since December 2015 and has indicated it will keep doing so this year.

So, if long-term rates were pushed lower by central bank bond buying, and now short-term rates are being pushed higher as the Fed tightens its monetary policy, the yield curve has nowhere to go but flatter.

“In the current environment, I think it’s a less reliable indicator than it has been in the past,” said Matthew Luzzetti, a senior economist at Deutsche Bank.

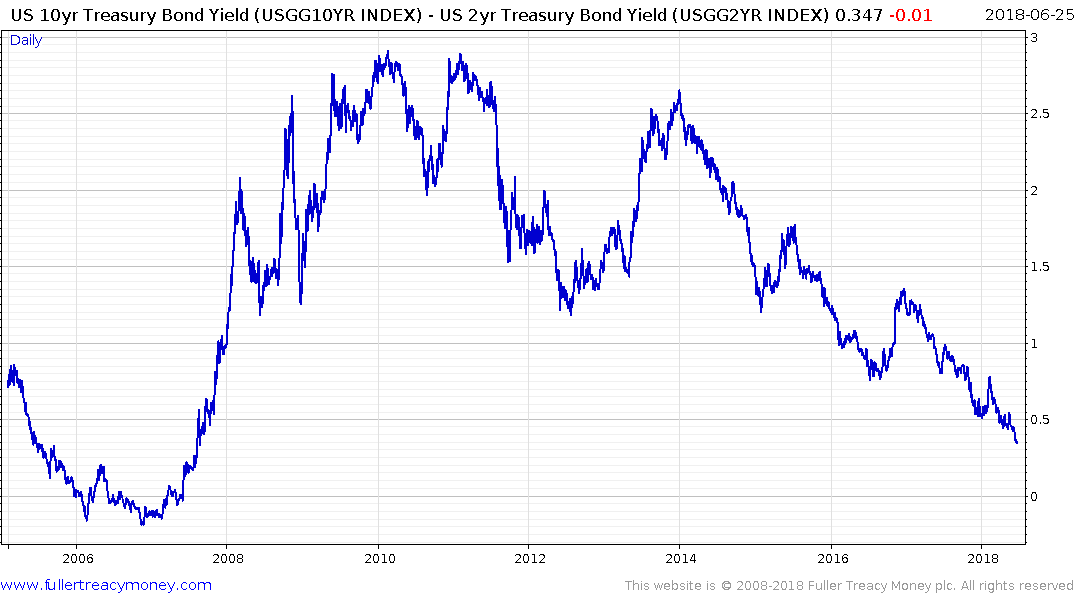

There are a lot more people looking at the yield curve spread today than when it last became inverted 12 years ago. Back then there were also arguments for why it would not be useful indicator despite its record of predicting recessions. In 2006 the argument ran along the lines that with inflation rising there was little chance of the short end catching up with the long end of the curve and besides China’s economic growth was going to change the world forever.

The yield curve spread is not the only indicator of a future recession but it is sufficiently reliable that we have no choice but to pay attention when it eventually does become inverted. However, it is also worth remembering that the yield curve inverted in early January of 2006, bounced and became inverted again later that year and all the way through the first half of 2007. In that time the S&P500 rallied from 1250 to a peak above 1550. That 24% rally did a lot allay fears about an impending recession and a year and a half is a long time in markets.

The other points to watch for an impending recession are rising high yield spreads, rising unemployment surging oil prices and the underperformance of banks. Right now, US high yield spreads remain inert but Eurozone high yield spreads are trending higher, unemployment is still at record lows and oil prices are rising but are not accelerating. That points towards the current hiatus on Wall Street looking more like a pause than a top, unless of course the major indices sustain moves below they repsective trend means and banks roll over.

My one big concern is that major banks in China and Europe are trending lower in an aggressive manner. US Banks are still holding at the region of the trend mean and lower side of the latest range but will need to rally soon to signal a return to demand dominance.