Email of the day on the upcoming MSCI decision to admit A-Shares to the Emerging Markets Index:

How do you think the H-shares will be affected if MSCI (and later FTSE) add the A-shares to their emerging market indices?

The 2 futures which give easy access to the Chinese market at the moment are the Hang Seng China enterprise index and the FTSE China A-50 index. Which of these do you think is the better bet?

China has been making efforts to open up its capital market to foreign investment. The Hong Kong Shanghai Connect is the most visible measure and the touted expansion of the system to Shenzhen suggests they are still open to additional expansion of the conduit. However it is open to question whether what has already been achieved is enough to warrant a positive decision by MSCI. This article from the Wall Street Journal carries additional information. Here is a section:

The looming decision underscores the disconnect between the expanding role China plays in the world economy and the limited weighting China has in global investment portfolios.

In the MSCI All Countries World Index, a global benchmark, China has a weighting of 2.7%, although the country’s economy accounts for 15% of global gross domestic product.

The MSCI emerging-market index has a 25.7% allocation to China, but primarily comprises Chinese companies listed in Hong Kong.

For decades, regulatory restrictions and opaque rules set by Chinese authorities have kept foreigners away. In addition, concerns about the health of China’s economy, corporate governance and the earnings multiples that many Chinese shares trade at have led many managers to hold even fewer Chinese stocks than these benchmarks suggest.

As of 2014, foreign investors held about 3% of the Chinese market, compared with a 12% foreign stake in India, according to Qi Wang, partner at Shanghai MegaTrust Investment, an A-share fund manager based in China.

My feeling is that MSCI will be very measured in their approach since they have a responsibility to their clients not to shake the market too much by their decisions. This suggests that even if they do not decide to admit A-Shares on the 9th they will say under what conditions they will begin to admit them.

A-Shares rather than H-Shares stand to benefit from any evolution in MSCI policy. This is at least partially explained by the A-Shares outperformance over the last six months. Considering the fact that the Emerging Markets Index is heavily skewed towards Hong Kong listings there is the possibility that demand will be cannabilised by the admittance of A-Shares. The big question then is to what extent the World Index weighting changes. A gradual move from 2.7% to 15% would be hugely positive for both the A and H-Share markets.

The FTSE/Xinhua China A50 Index has paused for much of the last six weeks in a similar sized range to that posted between December and March. A sustained move below 13,000 would be required to question the consistency of the advance and to suggest a deeper process of mean reversion is underway.

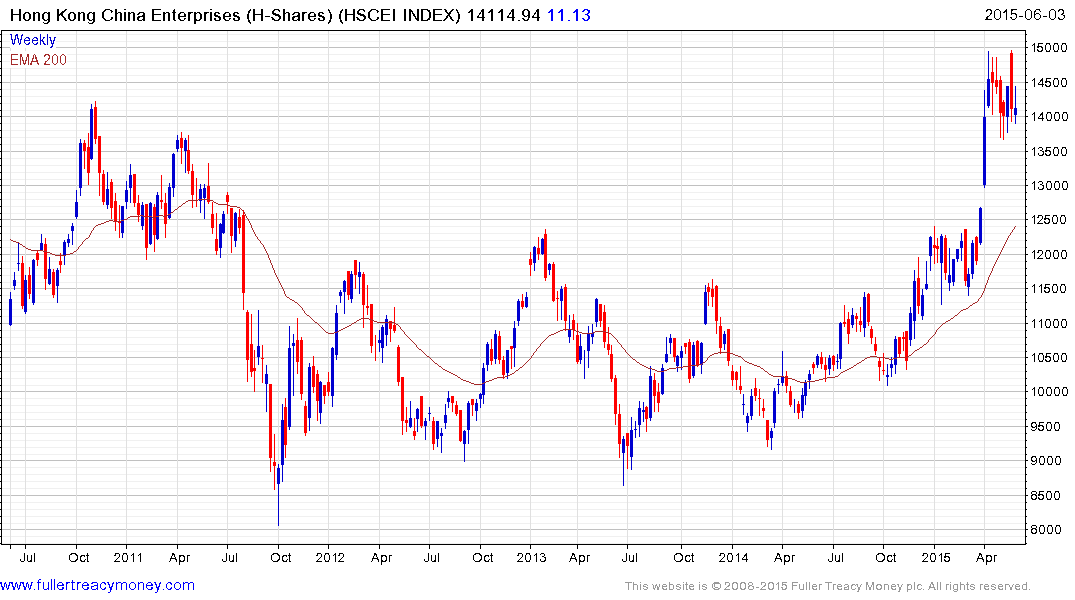

The Hong Kong China Enterprises Index (H-Shares) has been ranging mostly above 14,000 and the 2011 peak since mid-April, in a relatively gradual process of mean reversion. The 13,650 level will need to hold if current scope for continued higher to lateral ranging is to be given the benefit of the doubt.