Email of the day on the next crash

Dear Eoin, could you comment on Niall Ferguson's market prediction in the Sunday Times:

Thank you for this article which may be of interest to subscribers. It is always a useful exercise to contemplate the end of the financial world but in the full knowledge it doesn’t happen all that often. Niall Ferguson does a good job of articulating the potential causes of future problems in this article which is sure to garner attention for his new book.

Here is a section:

The combined assets of the big four central banks, ”the Fed, European Central Bank, Bank of Japan and Bank of England” will peak in December 2018, but the rate of expansion has already started to slow. Moreover, global credit growth in aggregate is slowing. History shows that monetary tightening acts with long and variable lags. But it does act, often on stock markets.

Second, as the economist Charles Goodhart and others have argued, we are at a demographic inflection point. Globally, the ratio of workers to consumers has peaked. Between now and 2100, China’s working-age population is projected to shrink from 1bn to below 600m. Already many labour markets look tight, with unemployment rates and other measures of slack leading economists to expect a surge in wages and inflation.

Countries such as Germany that think immigration will help matters will be disappointed as many newcomers lack the skills to be easily absorbed into a modern workforce. What is more, the rising dependency ratio as populations age doesn’t translate into higher saving but into higher consumption, especially on healthcare. Welfare safety nets have encouraged many retirees not to provide completely for the costs of a prolonged old age. This leads to the conclusion that the end of the 35-year bond bull market is nigh. Bonds will sell off; long-term rates will rise. The question is whether inflation will increase as much or more. If not, then real (inflation-adjusted) interest rates will rise, with serious implications for highly indebted entities. The Bank for International Settlements recently published early-warning indicators for stress in domestic banking systems. Two big economies with flashing red lights are China and Canada.

Point three: regardless of monetary policy, a networked world, ”whose biggest companies are dedicated to reducing the cost of everything from shopping to searching to social networking” is a structurally deflationary world. According to the World Bank, a bewildering range of occupations” from food processors to finance professionals” have a 50% or higher probability of being “computerised”, with technology entirely or largely replacing human workers. Already Waymo’s driverless cars are on the streets of Phoenix, Arizona. Last week, Elon Musk unveiled the spectacularly cool Tesla truck, which no doubt shares the self-driving features of Tesla cars. I have seen the future and it drives itself. Today’s drivers need to retrain as nurses.

Oh, and if you debtors were pinning your hopes for an inflation surprise on a new Middle Eastern crisis, as in 1973, 1979 and 1990, I have to disappoint you. According to the International Energy Agency, America is halfway through the biggest expansion in oil output by any country in history” an additional 8m barrels of oil a day between 2010 and 2025” thanks to the ingenuity of shale oil drillers. Even without electric cars, we would avoid a serious oil shock even if Iran and Saudi Arabia went to war tomorrow.

If we ask ourselves the simple question “has quantitative easing had a distorting influence on markets?” The immediate answer has to be yes.

Which market has been most distorted? It has to be in the sovereign bond and credit markets. One of the defining characteristics of a crowd in the euphoric stage is a tolerance of contradiction. If negative yields are not a contraction in terms nothing is. Therefore, we can logically assume the next big problem is likely to be in the bond markets.

There are two big well understood events happening within the next 12 months. The Federal Reserve gets a new chair and four of the seven seats are due to be filled. President Trump has an unprecedented opportunity to reshape the committee that sets rates and that represents an uncertainty. The second is the Federal Reserve has embarked on a tightening phase. It is now both reducing the size of its balance sheet and raising rates simultaneously. That is at least in part aimed at countermanding the inflationary pressures of running procyclical fiscal policy.

The balance sheets of the major central banks stand at approximately $19.5 trillion. The big question right now is whether shrinking by the Fed and tapering by the ECB will be made up for by printing in Japan and China. If not then Ferguson’s contention that the total will peak in late 2018 could be true.

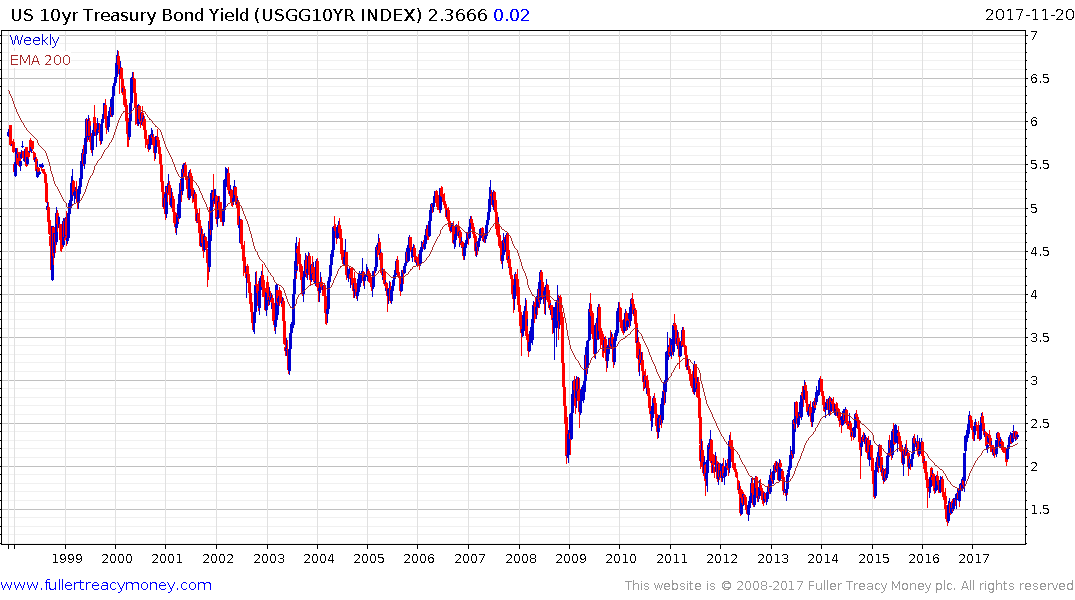

An important point to remember is that ranges are explosions waiting to happen. 10-year Treasury yields are at the same level today as they were in December 2008 and have been in a well-defined range since at least 2011. When yields eventually break out of this base formation, the move is likely to be both abrupt and surprising in its magnitude.

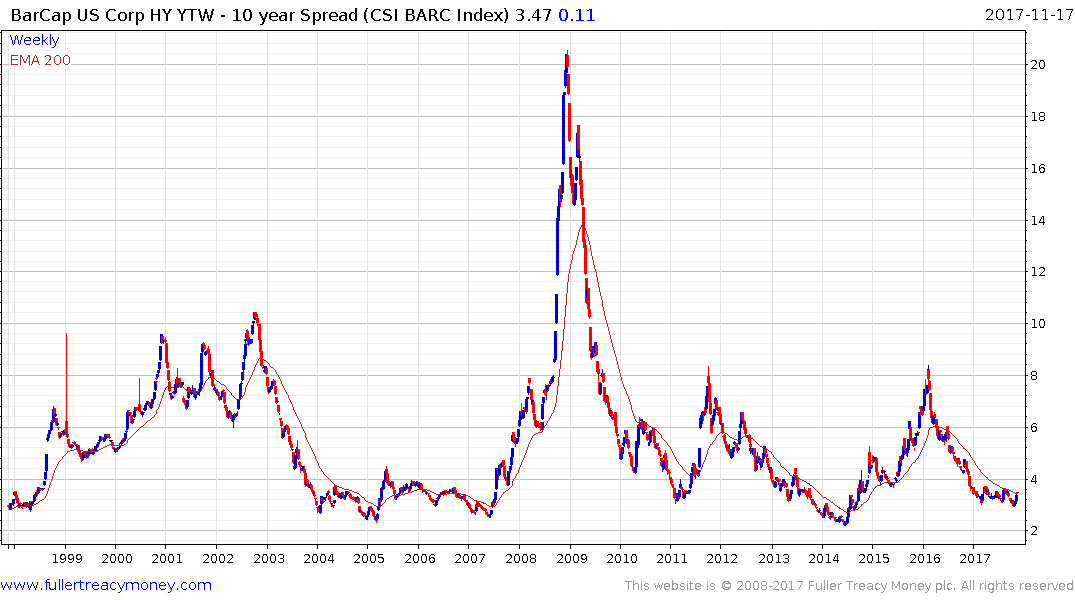

At that point there is likely to be a reckoning in the credit markets. Many companies have increased their debt to equity ratios. Who wouldn’t when credit was essentially free? One of Warren Buffet’s adages is “You don’t know who has been swimming naked until the tide goes out” As interest rates rise so do refinancing costs. High yield spreads represent a leading indicator for future trouble in the credit market. High profile companies like Tesla and Uber, that are both highly disruptive and loss making, represent the thin end of the wedge in the high yield market.

The US consumer is no longer the epicentre of risk because it is now companies and governments that carry the most leverage. However Chinese, and by extension Australian and Canadian consumers, are highly levered. That is most especially true since they largely sidestepped the last credit crisis and so have become even more leveraged in the last decade. China is engaged in a massive experiment as it transitions to a consumer driven economic model. There is no sign yet that anything is askew but it bears monitoring nonetheless.

The nature of contagion selling is that people end up selling not what they want but what they can. That generally means bargains appear in attractive assets that lead the way out of the decline. The accelerating pace of the technological innovation is unlikely to be disrupted by trouble in the bond markets but it could represent a catalyst for a medium-term correction.

Back to top