Email of the day on the impact of financial regulation

You write: "The prospect of negative interest rates is particularly bad news.....because not only do they have to hold more capital but they have to pay the ECB for the privilege". This is not particularly clear. Please explain why banks have to hold more capital when rates go negative. Also, how the link with the ECB works. Thank you very much.

Thank you for the opportunity to clarify what is an important point. The regulatory overhaul that has been implemented across markets means banks need to hold more Tier 1 capital. Prior to the financial crisis they could have substituted some Tier 2 capital, (lower quality assets) to fulfil their core capital requirements. If they don’t have enough Tier 1 capital they need to get it somewhere and the easy route is to borrow bonds at the discount window in exchange for Tier 2 and lower quality assets. The result of negative interest rates is that they now have to pay for the privilege rather than picking up the carry on the spread on higher yielding assets.

The Japanese response to its banking problems has been to force the banks to hold onto the bad loans. The Europeans nationalised a lot of debt but the banks have not been recapitalised sufficiently to allow them to lend again. The US response has been more comprehensive but it would be rash to conclude they have fully recovered from the financial crisis, although they are certainly further along in the process. Janet Yellen’s schizophrenic discussion of raising rates and in the same breadth considering negative interest rates is hardly confidence inspiring.

The S&P 500 Banks Index (P/E 9.87, DY 2.41%) includes JPMorgan, Wells Fargo, Citigroup and Bank of America. It dropped precipitously in January to break the almost four-year progression of higher reaction lows, in a massive reaction against the prevailing trend. An unwind of the short-term oversold condition is now underway but big questions will be asked assuming it gets back to test the region of the trend mean and the lower side of the overhead top formation.

The DJ Euro STOXX Bank Index’ five largest, Banco Santander (11.84%), BNP Paribas (11.44%), Intesa SanPaolo (9.3%), ING (8.99%) and BBVA (8.14%) represent almost 50% of the sector’s market cap. The Index accelerated to last week’s low so there is scope for an unwind of the short-term oversold condition but a sustained move above 130 will be required to begin to signal a return to demand dominance beyond short-term steadying.

The FTSE 350 Banks Index is dominated by HSBC, Lloyds and Barclays, representing 87% of the Index. It accelerated to test the 2011 low over the last month and has at least steadied in the region of 3000. As with the above indices there is scope for a reversionary rally but a potentially lengthy period of support building will be required to begin to rebuild confidence.

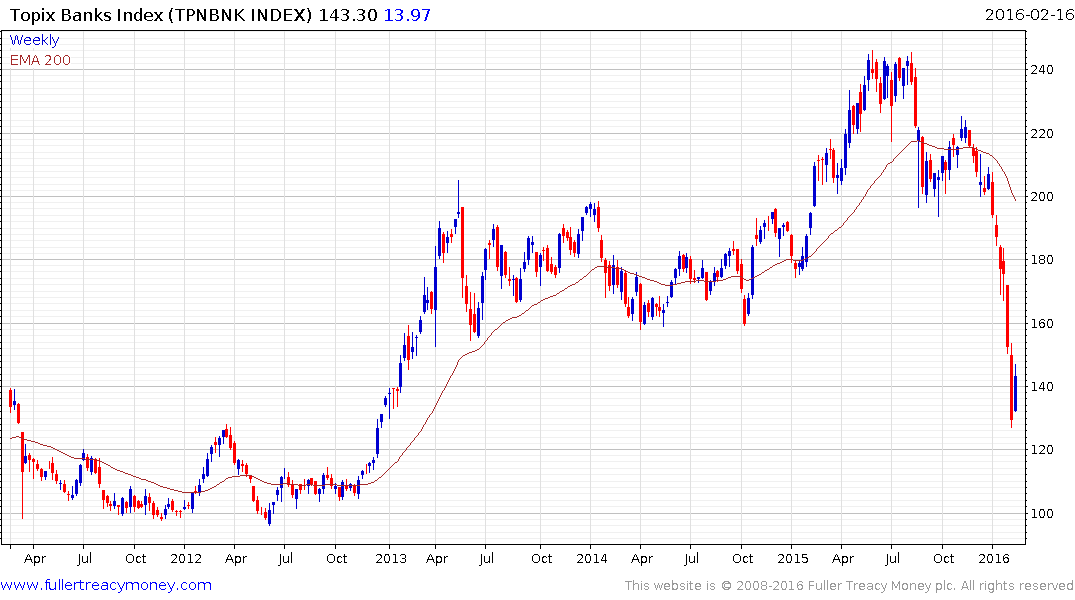

Japan’s Topix Banks Index is dominated by Mitsubishi UFJ, Sumitomo Mitsui and Mizuho; representing almost 62% of the sector. It unwound its entire bull market advance as it crashed lower between November and last week, before steadying above the 2011/12 base. Even following this week’s bounce to date it is still 38% overextended relative to the trend mean, so there is scope for a reversionary rally but the price action is likely to remain volatile.

The attitude of regulators towards the banking sector is a major consideration because it is interfering with the role they play in providing liquidity to both the market and the wider economy. The combination of wholesale and investment banking in the 1990s enabled trading desks to expand and the more recent rules on capital, interest rates, compliance and risk means that banks have had to dispose of trading desks and no longer have the same capacity to lend. There are good reasons to reduce the influence of banks in stoking investment bubbles but it is a mistake to conclude that the financial sector was solely to blame for the credit crisis. Lax regulation and short-term government policies were also at fault. The backlash that has taken place is now inhibiting the important role played by the financial sector in promoting economic growth. This is contributing to credit spreads widening.

.png)

The Credit Suisse High Yield Index has completed top formation characteristics and following such a large run-up from the 2009 low it would be foolhardy to ignore the impact that it is likely to have on the financial sector. This suggests the corrective phase evident on the above charts might have found a short-term low but potentially lengthy support building will be required to begin to rebuild confidence and a great deal will depend on what governments do to lend assistance.

Back to top