Email of the day on the Dollar and commodities

A very well-respected cotton trader in Texas told me many years ago, that amongst all the factors influencing the price of cotton, the value of the dollar is by far number one. I guess this also is true for the price of gold to some extent. I was presently surprised to see how well gold has held inspite of the dollar’s strength. Am I missing something? I would be grateful if you would share your views on gold in the current environment. As always thanks for your very valuable service.

Thank you for your kind words and this topical question which may be of interest to the Collective. The Dollar usually trends higher when there is a wide interest rate differential with other currencies supporting it. That makes borrowing money for speculation more expensive, such liquidity out of the global economy, and reduces demand for raw commodities. That tends to weigh on commodity prices.

Gold is difficult to analyse because the price tends to be volatile. It will do nothing for years at a time, only to explode on the upside when most people have become disillusioned with its inactivity.

Gold is a major globally traded commodity and is not immune from contagion when both bonds and equities fall together. Nevertheless, it is less well-owned than either of those assets, so it less susceptible to tighter liquidity than either of those markets.

.png)

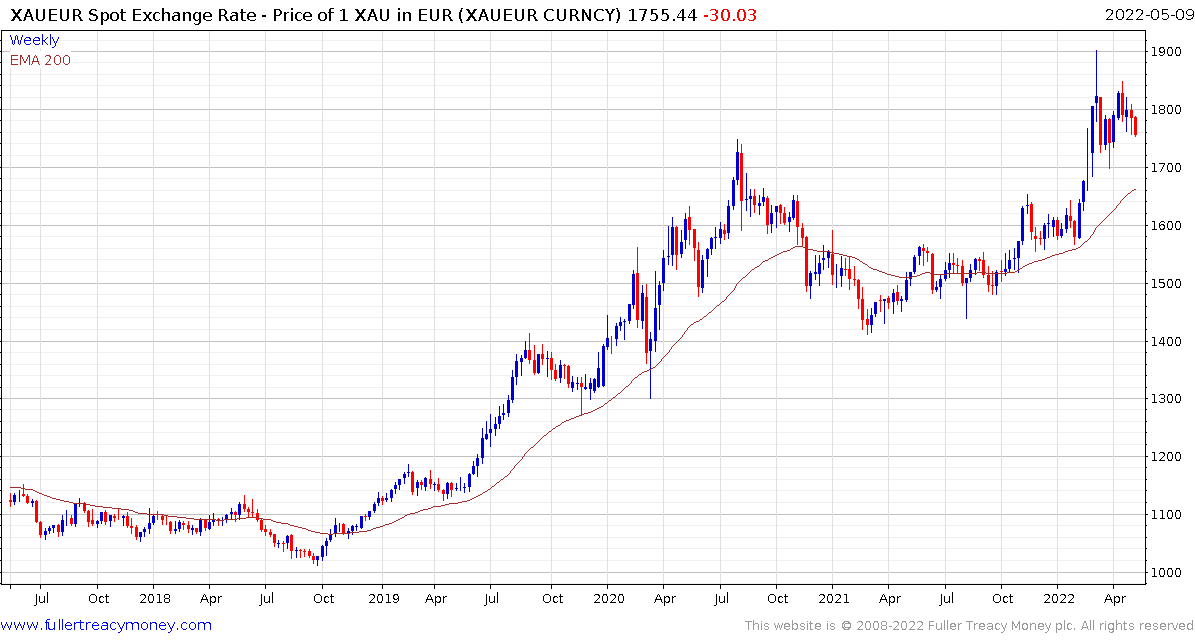

Gold has performed better when denominated in other currencies. The significant deterioration of the Pound, Euro, Australian Dollar, New Zealand Dollar, Yen, and Renminbi have made gold more attractive for investors in those countries.

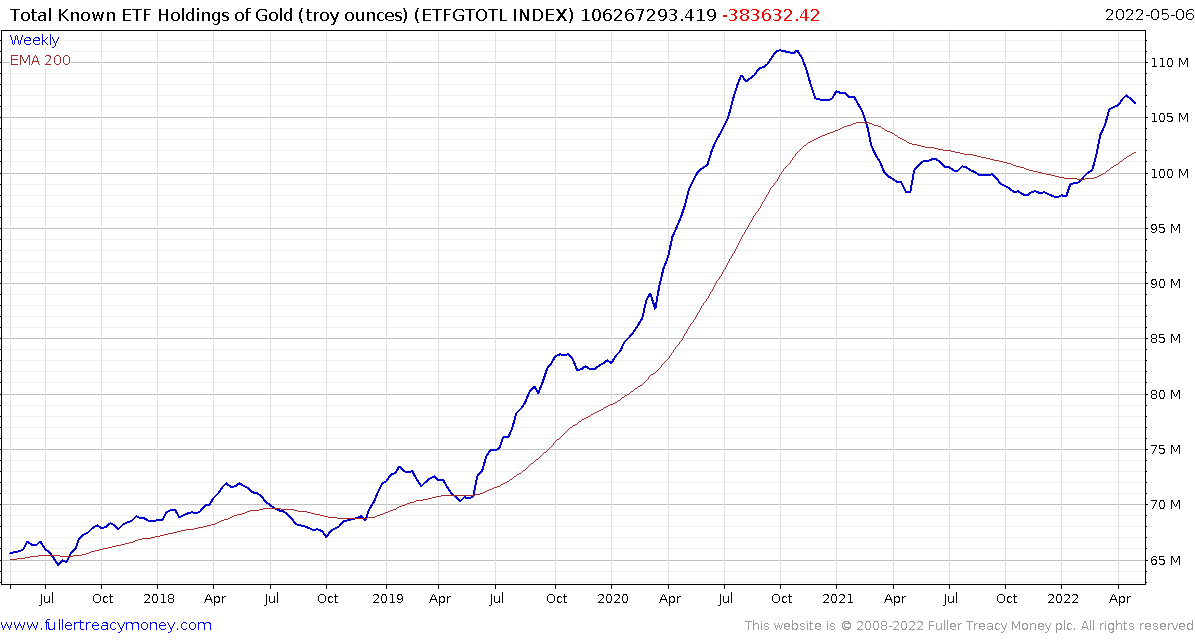

Total ETF holdings of gold have also been quite steady despite volatility in other assets.

The strength of the Dollar detracts from the store of value characteristics gold offers. The counter argument is the Dollar is only the least dirty shirt among a host of fiat currencies actively being depreciated in real time. By that standard gold is in a realm of its own when it comes to limited supply and monetary history.

The primary risk to gold is forced liquidation from a panicky sell-off in the stock market. Contagion selling resulted in a significant drop in 2008 and fear of a repeat has deterred investors from taking positions recently. Everyone is aware that gold sold off aggressively during that episode before storming back to set new highs.

I am encouraged by the fact gold is holding the region of the 200-day MA and the upper side of the underlying range, but it will need to find support soon if the benefit of the doubt is to be given to the upside.

Silver is also testing an area of potential support at the lower side of its range and the 1000-day MA.

Silver is also testing an area of potential support at the lower side of its range and the 1000-day MA.

Gold shares are now also back at the lower side of their range.