Email of the day on the cumulative effect on interest rate hikes

I seem to remember many years ago David saying that the time to be wary of share markets is after the third interest rate rise. Is this accurate and, if so, is it a relevant indicator for us now?

Thank you for this topical question which may be of interest to the Collective. The initial response to a new hiking cycle is generally seen as positive by investors because they prize efforts to control inflation and preserve growth. However, interest rate hikes have a lagged effect on the economy and are cumulative in nature. That means the initial enthusiasm at continued growth gives way to worry about the toll of withdrawing liquidity as the number of hikes builds.

Historically, 3 interest rate hikes have been enough to swing sentiment from complacency at the new hiking cycle to worry it may go too far. Stock markets begin to price in disappointing future growth well before a recession begins.

The challenge right now is central banks are tightening and corporate earnings could be peaking. The stock market has been supported by the ability of companies to expand margins despite lower sales. That is not sustainable indefinitely because price hikes eventually run into resistance from buyers and slower growth results in fewer sales.

The FANGMANT shares are leading on the downside. They still represent 21.75% of the entire market.

The FANGMANT shares are leading on the downside. They still represent 21.75% of the entire market.

The market is much more interest rate sensitive today than in past cycles. That suggests the pass through of tightening liquidity is happening faster too.

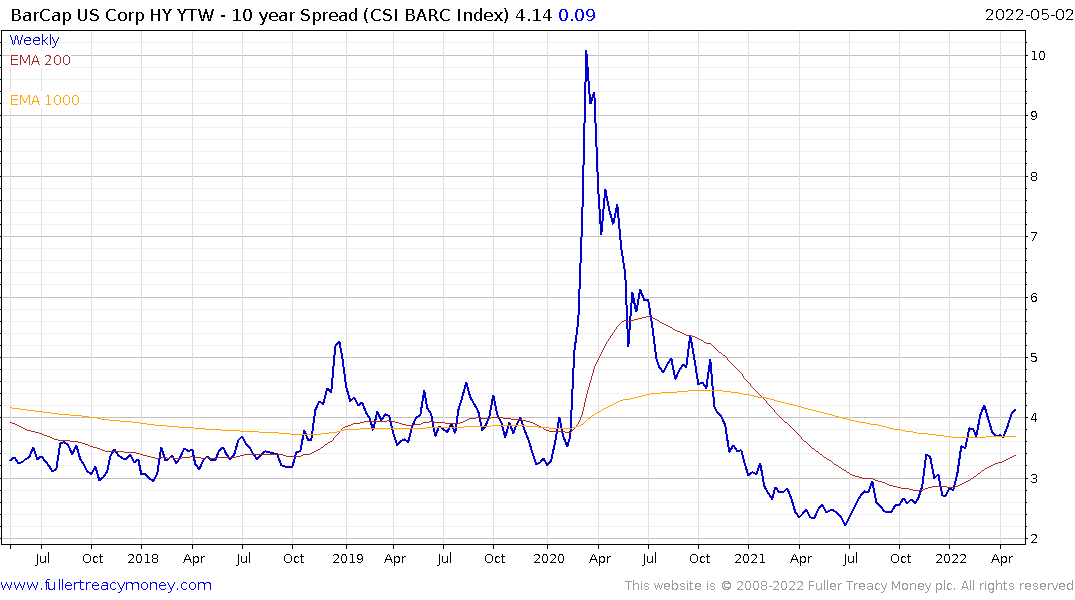

High yield spreads continue to firm and closed above 400 basis points yesterday. Trending spreads above 500 basis points tend to coincide with significant stress in the stock market and generally prompt central banks to take remedial action.

High yield spreads continue to firm and closed above 400 basis points yesterday. Trending spreads above 500 basis points tend to coincide with significant stress in the stock market and generally prompt central banks to take remedial action.

Earlier this year I believed the Federal Reserve would not be able to raise rates beyond a single token hike (my one and done hypothesis). I thought the stock market would be in a hurry to price in hikes so the Fed would not be able to act. I was too early in thinking we would see a meaningful decline. Stocks remained steady for longer than I thought likely, and we have now seen 2 hikes and the Fed Funds Rate at 1%.

Being early and being wrong are similar in the markets but the conclusion remains the same. We will not see a significant change of policy until negative stock market performance causes both political and monetary alarm. That generally coincides with a reversion to the 1000-day MA for the major indices. That could easily be achieved before the next Fed meeting.

Being early and being wrong are similar in the markets but the conclusion remains the same. We will not see a significant change of policy until negative stock market performance causes both political and monetary alarm. That generally coincides with a reversion to the 1000-day MA for the major indices. That could easily be achieved before the next Fed meeting.

Bitcoin unwound yesterday’s rally today, to confirm resistance in the $40,000 area. As a barometer for risk appetite and global liquidity, bitcoin’s underperformance is a further sign of deleveraging.

Bitcoin unwound yesterday’s rally today, to confirm resistance in the $40,000 area. As a barometer for risk appetite and global liquidity, bitcoin’s underperformance is a further sign of deleveraging.