Email of the day on the Bank of England's support action

I just read the article below, and am surprised that pension funds take (or are allowed to take) leveraged positions. If the positions are for hedging, then should they not have the full cash to take delivery? Your views would be invaluable.

An interesting chart is attached. The extent of loss on a 40-year UKT issued last year!

It's been a long time since I first started listening to your amazing Daily Commentary. Now it is mandatory for me to hear your comments so that I can put whatever else I hear elsewhere into perspective.

Thank you for your valuable service, and I hope that your readers will have your guiding words for many decades to come.

Thank you for this informative email and the chart of the 40-year Gilt. The fact I received this same chart from several sources today is an indication of how momentous it is for a developed country long-dated bond to trade at 20p on the pound. Last year was a great time to issue a 40-year bond so kudos to the Treasury department. The measures announced by the Bank of England to backstop the market were necessary but come at a significant cost.

UK pension funds have been hit with variation margin calls of as much as £100 million ($107 million) each, after sharp falls in gilts and sterling pushed mark-to-market valuations on derivatives and leveraged repo positions heavily against them.

UK pension funds have been hit with variation margin calls of as much as £100 million ($107 million) each, after sharp falls in gilts and sterling pushed mark-to-market valuations on derivatives and leveraged repo positions heavily against them.

Simeon Willis, chief investment officer of consultancy XPS Pensions Group, says he knows of three different fund managers running pooled pension portfolios that have requested emergency capital from clients to keep positions open. “Unless clients happen to have a large amount of capital with those managers, that will lead to some temporary closing out,” says Willis, adding:

“The markets are moving more quickly than the timescales to transfer liquid assets from one place to another. So, the teams that don’t have instantaneous access to liquid assets in a large liquidity pool are starting to get hit with this.”

Pension funds face large margin calls on the interest rate derivatives and asset swaps they use for asset-liability hedging. Some are also being asked to post additional collateral against leveraged gilt repo positions, as well as foreign exchange derivatives used to hedge US dollar.

One of the family offices I advise had a founding position in a San Francisco-based provider of battery solutions to office buildings. After several funding rounds, they sold out at a substantial profit. However, it was the buyers that raised eyebrows for me. There were all pension funds and they were from all over the world.

Every pension has had the same problem. How do they generate their required return when yields were at historic lows for a decade? The only thing is to do was to go further out the risk curve on private assets. Pensions are both leveraged and heavily exposed to private assets. The action by the Bank of England is the thin end of the wedge in providing needed assistance on a global basis. It also gives us some insight to where the epicentre of risk is. Pensions.

Importantly, the primary reason assets have been selling off is because liquidity has been tightening. Today’s action by the Bank of England, promising to buy “unlimited” numbers of bonds lent support to the long-end of the curve and suggests a peak of medium-term significance. It’s the fresh source of liquidity many traders have been waiting for.

Importantly, the primary reason assets have been selling off is because liquidity has been tightening. Today’s action by the Bank of England, promising to buy “unlimited” numbers of bonds lent support to the long-end of the curve and suggests a peak of medium-term significance. It’s the fresh source of liquidity many traders have been waiting for.

The Pound also bounced because the Bank of England’s action removes some of the uncertainty even if it implies additional supply. That suggests scope for an unwinding of the short-term oversold conditions but not much more than that.

The Pound also bounced because the Bank of England’s action removes some of the uncertainty even if it implies additional supply. That suggests scope for an unwinding of the short-term oversold conditions but not much more than that.

The primary challenge is the unfunded fiscal splurge. The reality of the Bank of England buying bonds and the government spending like a drunken sailor is a clear monetization of the debt. That’s not going to help with inflation.

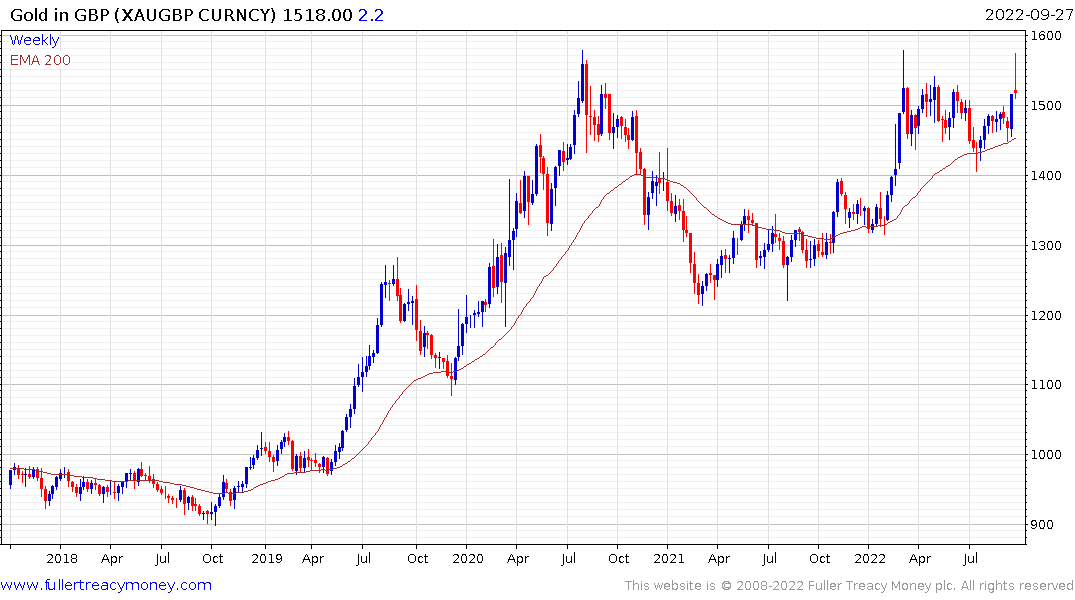

Gold in Pounds continues to pause in the region of the March peaks.

Gold posted an upside key reversal today. Upside follow through tomorrow could break the sequence of lower rally highs so this could be a pivotal event.

Gold posted an upside key reversal today. Upside follow through tomorrow could break the sequence of lower rally highs so this could be a pivotal event.

Copper also rebounded with an upside key reversal.

These market reactions assume the Bank of England action will likely be repeated by other central banks in the event bond yield surges become problematic.

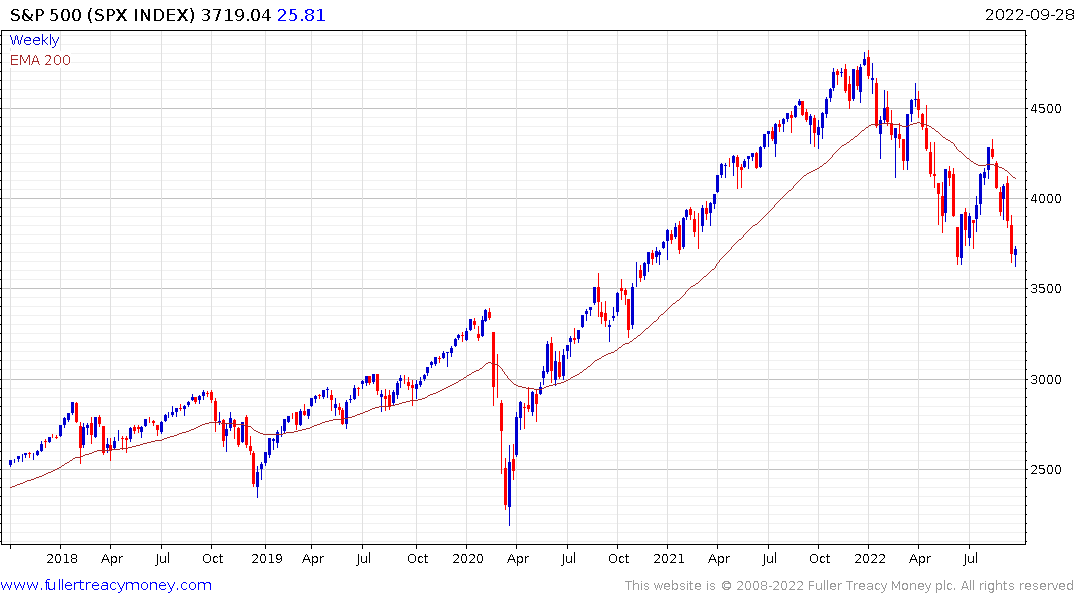

The S&P500 bounced today and has further scope to unwind the short-term oversold condition.