Email of the day on the Autonomies and the big picture:

By coincidence I did exactly the same exercise as you on Autonomies this week. I also find that the 10 year view is helpful in current market conditions. You put the emphasis on those Autonomies that are doing relatively well in the current market. What about those Autonomies that show much more bearish patterns? Are they in the majority among the overall number of such companies or not?

Thank you for this question sure to be of interest to subscribers. No Index has been immune to selling pressure in what is the largest stock market correction in seven years so it is a reasonable question how many of the Autonomies have bearish patterns.

On Friday I focused on the 30 or so that are still trading above their respective trend means because following a large drawdown I think it is more useful to attempt to identify leadership not least following a process of mean reversion. I also mentioned that the majority of underperformers are in sectors exposed to the slowdown in China’s economic expansion and deteriorating commodity prices, especially oil.

There are a significant number of companies that have experienced larger reactions that at any time in the last seven years but are still trading in the region of their August lows. These are the companies performing more or less in line with the wider market and are most notably represented by Apple. They have all experienced a loss of uptrend consistency but the broader question is to whether this is the first big consolidation in a secular bull market or whether it is a significant medium-term peak such as those witnessed in 2000 and 2008.

You probably know my view, not least if you read Crowd Money, that we could anticipate a lengthy volatile ranging phase when the Fed eventually decided to begin to normalise monetary policy. The rationale is that following a major breakout from a very lengthy trading range, it is entirely possible to get a consolidation, or first step above the base. Considering how long the base was, this range could last upwards of a couple of years and it has already been one year for the S&P500.

The background for this view is that the bullish factors represented by the revolution in energy, technological innovation and rise of the global consumer would be tempered, for a time, by the normalisation of interest rates following a particularly profligate period of monetary policy.

Volatile ranging has a waring effect on sentiment and this is particularly true when investors are unaccustomed to such drawdowns. The underperformance of the banking sector, globally, is perhaps the most significant bearish factor right now because commonality is pervasive and the downtrends so consistent. As liquidity providers banks should do well in an overall bullish environment. However what looks like inevitable stress in the high yield energy bond sector, significant regulatory cost inflation and meagre credit growth are weighing on financials because we do not yet have clarity on which banks are most susceptible to these factors.

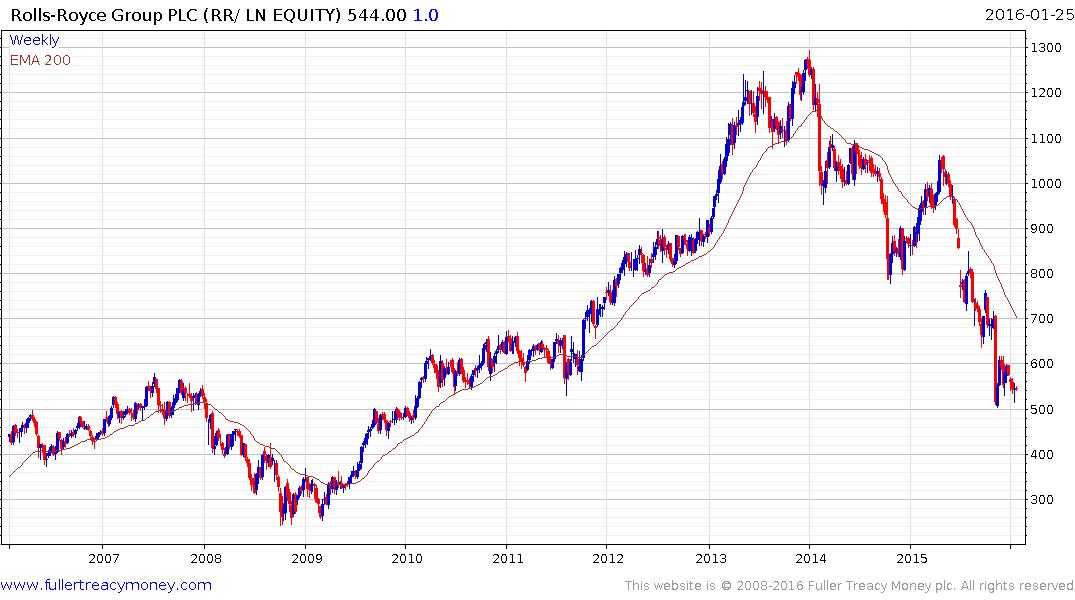

Within the industrial sector most shares have taken out their August lows so while the potential for a reversionary rally has increased they have considerably more work to do before investor sentiment recovers to a stage where medium-term demand dominance can be reasserted. Even within the industrials sector there is considerable variation. For example Rolls Royce is down over 60% from its 2014 peak and bounced last week from the region of the August lows. Potential for a reversionary rally has increased but a period of support building will likely be required to rebuild confidence.

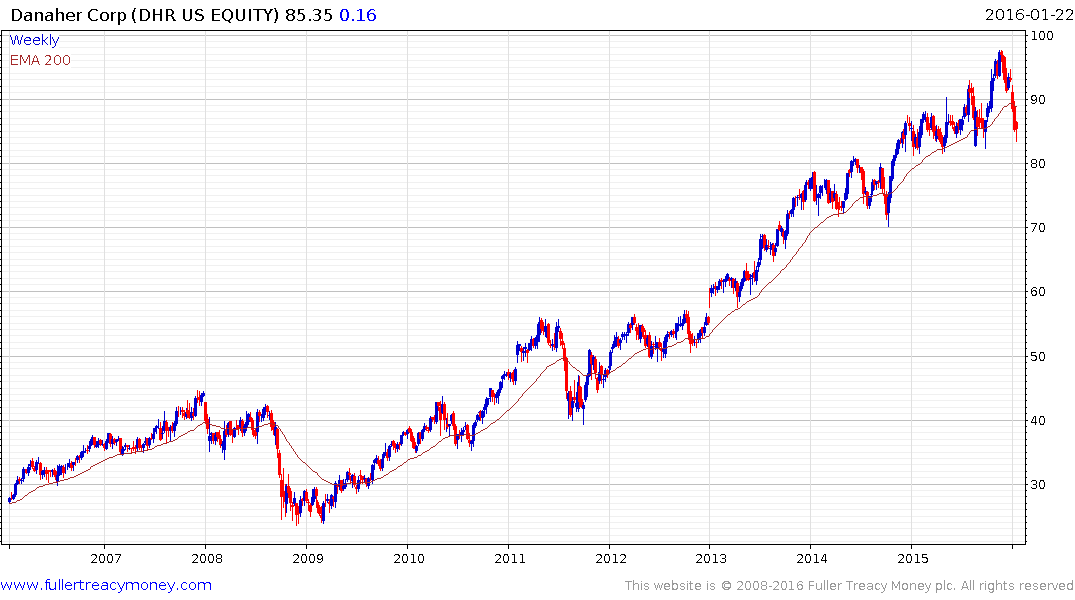

Danaher on the other hand failed to sustain the move to new highs in November and has pulled back to test the region of the lower side of the underlying range. It needs to steady here if the medium=term uptrend is to be given the benefit of the doubt.

Siemens has underperformed for much of the last few years but is currently bouncing from the lower side of a multi-year range.

The chemicals sector exhibits many of the same characteristics.

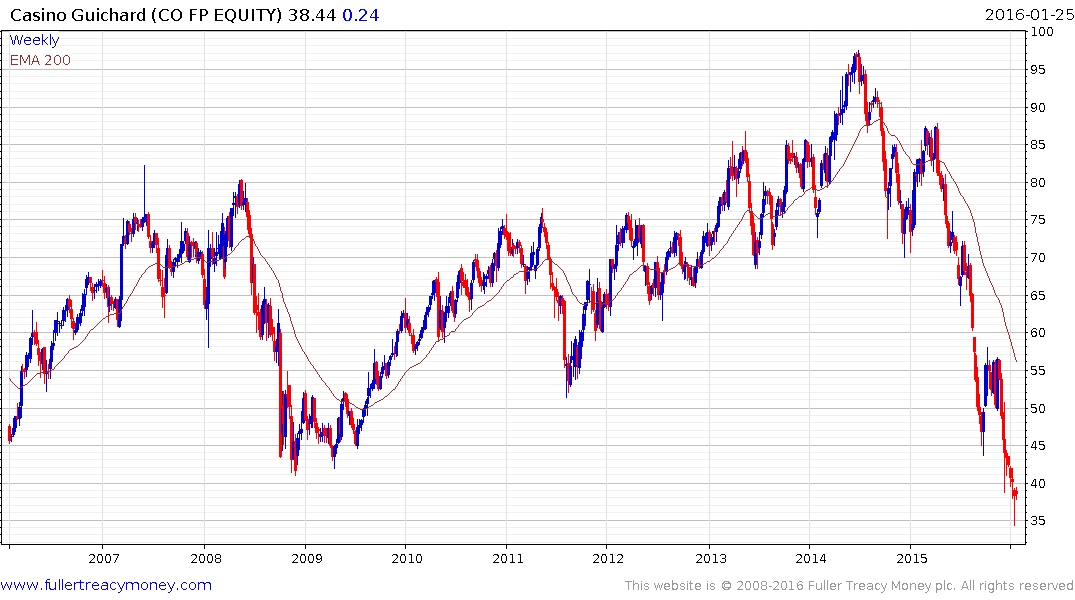

Looking at some of the companies that have experienced the deepest pullbacks Casino Guichard is heavily exposed both to the Eurozone and Latin America. The share has accelerated lower, posting new 19-year lows on Friday. It’s unlikely that the €3.12 dividend will be sustained at the next announcement, in March, but the bigger question is whether this is already in the price? A move above €40 would at least suggest a process of mean reversion is more likely than an additional decline.

The oil majors such as Exxon Mobil and Chevron are outperforming the oil prices by a considerable margin while miners such as BHP Billiton are deeply oversold relative to the trend mean but remain in medium-term downtrends.

If we add all this up then a short covering rally looks more likely than not but the medium-term outlook remains challenging so we can expect additional volatile ranging on major indices. However it should also be remembered that major market pullbacks inevitably create favourable entry opportunities and particularly in sectors that have experienced exaggerated pullbacks. In short this is still a difficult environment but not without opportunity.