Email of the day on share dilution

Thanks, Eoin, for your considered response. The point I was trying to get at though is that looking at a stock price chart only can hide all manner of sins. If the share count has doubled, all else equal, the price per share should only be worth half what it was previously. Having said that, I wouldn’t be in the least bit surprised if the Robinhood crowd bid up these names as they search for the last remaining recovery names without due consideration for all of the facts. Though in the short-term markets can be a voting machine, in the long term they are a weighing machine, and ultimately these investors will be found out.

Thank you for coming back on this topic. The most basic principle of price setting is to find the balance point between supply and demand. Supply is a present real-world statistic and demand is always going to be about what the future holds. Therefore, the price reflects both what is known and what is expected about any given instrument.

The easiest way to illustrate the point you are concerned about is to compare the market cap of a company with the price. Since market cap is calculated by multiplying shares outstanding by the price any deviation reflects either excess supply and a dearth of supply.

Norwegian Cruise Line Holdings is a very good example of this. The company spent a great deal of money buying back shares ahead of the pandemic so the market cap traded below the price for a prolonged period. In many respects financial engineering was the primary support for the share. Now, the company has massively increased the supply of shares so it will have to deliver on revenue growth if the recovery is to be sustained.

There were a number of stories about Tesla’s additional share sales today, the third this year. However, $5 billion is inconsequential relative to the size of the market cap at this stage.

There were a number of stories about Tesla’s additional share sales today, the third this year. However, $5 billion is inconsequential relative to the size of the market cap at this stage.

The ability of companies to engage in highly risky financial engineering is a product of the low interest rate environment. That is going to last as long as ample liquidity remains the primary support for markets.

I don’t think the social/leisure sector is going to be the leader in this recovery but it was priced as if were about to go bust. That suggests there is scope for a significant recovery as we come out of the pandemic.

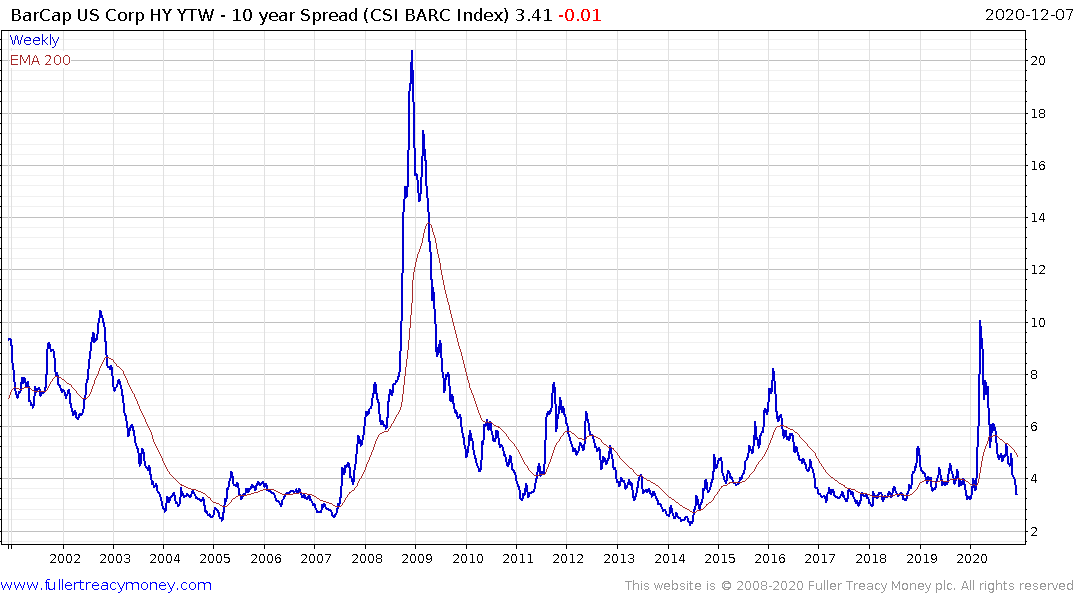

If high yield spreads were rising, I would be much more worried about highly indebted/high leverage companies but most have been able to refinance at very accommodative rates this year. That has pushed out a possible maturity cliff a few years at least.