Email of the day on industrial metals miners

“All the big mining companies coming down 20-25 pct in 4 to 5 days. pretty scary to me. what am I missing? Beside talk about the Fed raising interest rates in May with 0,5 pct and a growth scare or the lockdowns in China? Any other reasons? Should we now buy the miners again with the positive future ahead? Gold and copper also look attractive now. your opinion please”

Thank you for this question which may be of interest to the Collective. Ultimately, the question can be distilled down to whether we believe the rest of the world is going to invest in enough infrastructure to outpace a significant economic slowdown in China. The answer is not necessarily binary. We probably get one first, then the other.

.png)

Today we have a strong Dollar, tightening monetary policy, less accommodative fiscal policy, and a deteriorating Chinese economy. None of those factors have historically been positive for commodity prices.

Russia’s invasion of Ukraine, the build out of renewable energy infrastructure and battery factories point towards significant demand growth in future. As efforts to avoid Russian supply mature, the potential for more aggressive sanctions grows. Unfortunately near-term beats long-term when profit taking sets in. Brent crude oil continues to pause in the $100 area.

Commodities have, until this week, been rallying in line with the US Dollar. That’s not normal. It’s only been possible because investors panicked out of bonds. That created demand for physical assets. If supply chain issues with China continue to exacerbate it will complicate the outlook for commodities.

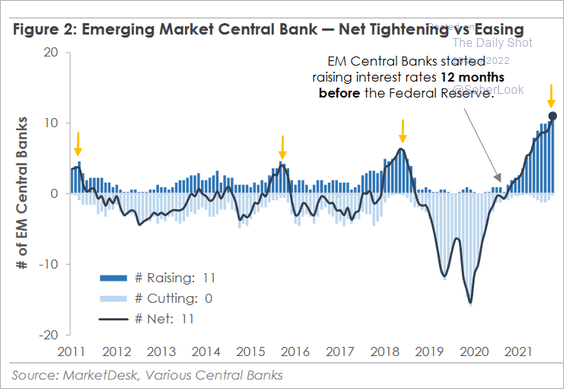

Monetary tightening has barely started, and yet more emerging markets are simultaneously tightening today than at any time since 2010.

Monetary tightening has barely started, and yet more emerging markets are simultaneously tightening today than at any time since 2010.

China’s metal bashing industries were shut down for the Winter Olympics. They should have started back up now, but that is happening only sporadically because of the pandemic. The continued spread of COVID in China and the Party’s commitment to fighting it at all costs, is negative for growth.

Xi Jinping today supported plans to accelerate infrastructure development which is positive. However, how will building be possible if they lock down more and more of the economy? Dispensations for “essential workers” don’t exist in China like they do in California.

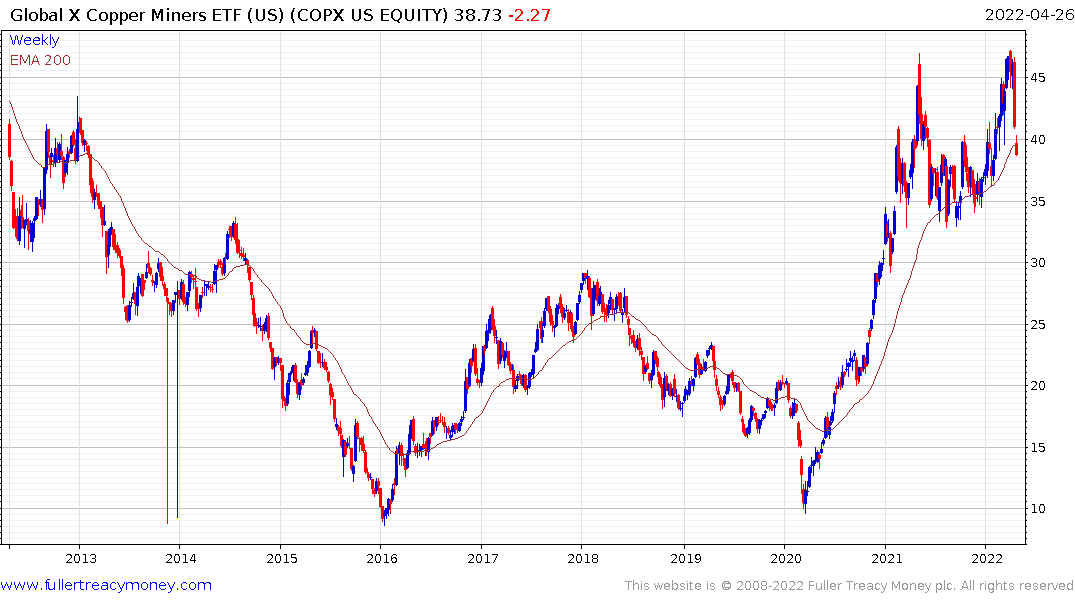

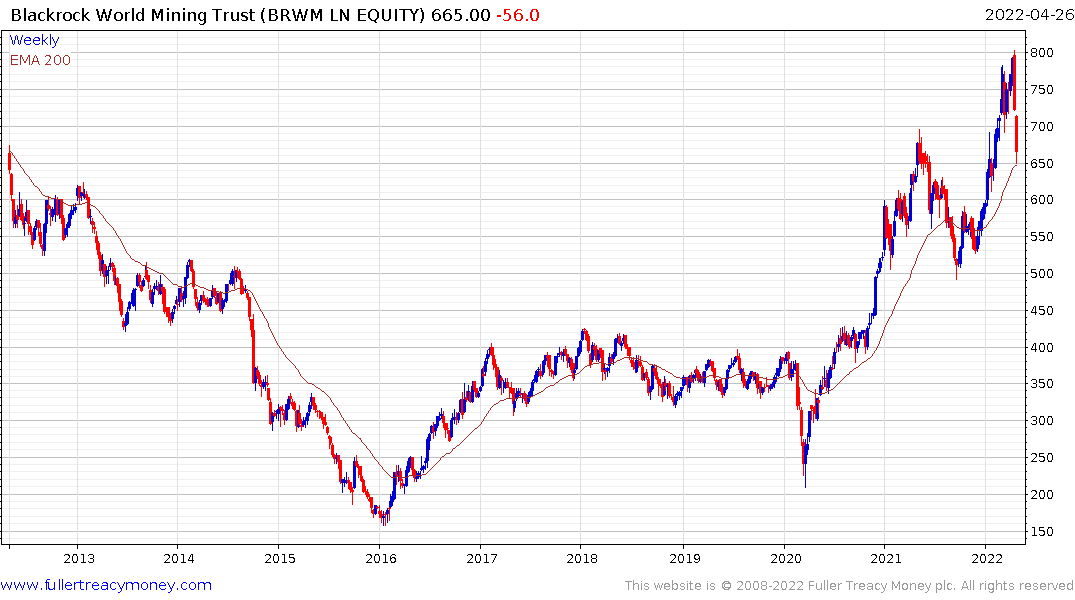

Mining stocks are pricing in at least a mean reversion for industrial resources. The London Metals Index pulled back sharply today but still has a wide overextension relative to the trend mean.

The Blackrock World Miners Trust and the Global X Copper Miners ETF are both already testing their respective trend means.

The primary aim of central banks tightening policy is to contain demand for everything. That suggests we should be expect volatility because any significant drop in metal prices will be swooped on by consumers. GE announced losses in its wind division today which were driven by higher costs. They will be in the market to secure lower priced metal in the event a significant setback.

During the last commodity bull market, the majority of shares posted sawtooth profiles with deep retracements and impressive surges. Given the confluence of bullish and bearish arguments, I think it is reasonable to expect a similar risk profile on this occasion. Personally, I will be willing to buy big dips but I’m not buying yet.

The one sector that has already had a big sell-off is bonds. With the prospect of slowing global growth and inflationary pressures that could moderate as a result, bonds should rebound. The 10-year yield continues to pause below the psychological 3%.