Email of the day on gold and interest rates

Can gold really breakout when real interest rates are rising?

Thank you for this question which I have been pondering for a while. Gold does not have a yield so the only way it can outperform on a total return basis is for the price to rise. The reason it can do that is because the supply of gold is not easily or quickly increased. That’s it’s primary advantage relative to electronic money which is wished into existence by a simple keystroke.

Most of the time the global supply of gold is ample for the needs of the global market but when people get worried about the purchasing power or increasing supply or other currencies or the rate of inflation then demand for gold rises and focus turns to supply inelasticity.

Gold tends to do best when inflation, whether as measured by governments or felt by consumers is running ahead of the rate at which investors are being compensated by rising interest rates.

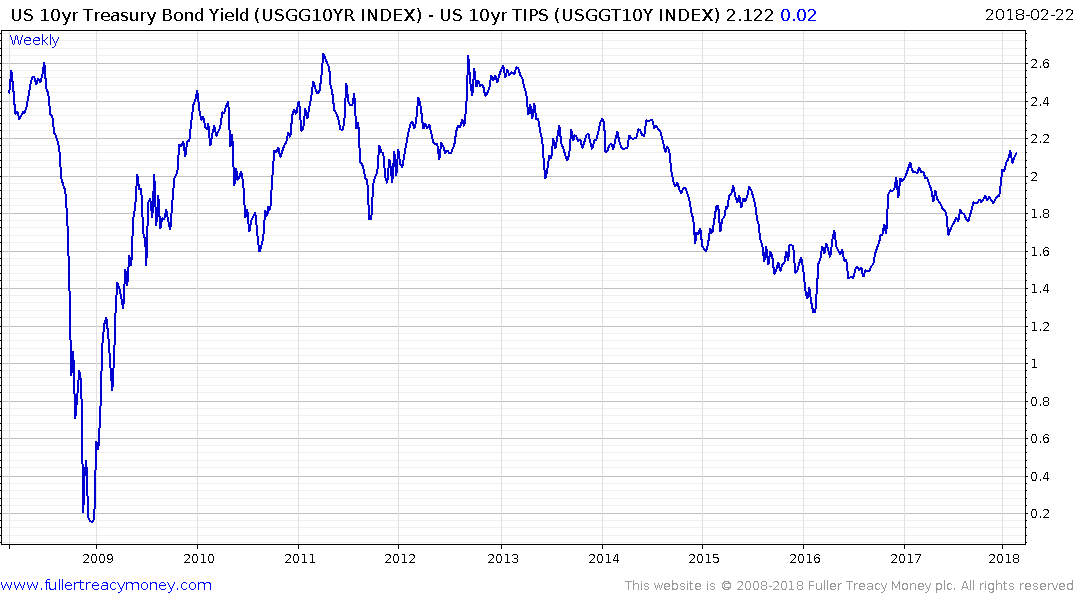

If we look at the spread between the 10-year Treasury yields and 10-year TIPS we get a reasonable barometer for inflationary expectations. This chart confirms inflationary expectations are rallying from the 2016 lows but the absolute level is still well below the rates seen between 2010 and 2014. Gold’s history during that time suggests that rather than the absolute real interest rate, it is the perception of whether inflation is under control or not that influences demand for the metal.

Gold has been ranging below $1400 since 2013 and there has been a distinct rounding characteristic to the chart action since the sharp rally in early 2016. As long as the progression of higher reaction lows remains in place we can conclude the metal is under accumulation by investors. Within the context of this 10-year chart the current consolidation has been relatively orderly but a sustained break above $1375 will be required to confirm a return to demand dominance beyond the short term.

Two additional points come to mind. The first is that there are no new TIPS due to be auctioned this year so the performance of that chart is likely to be a reflection of market perceptions about future inflation rather than influenced by the Treasury flooding the market with new supply as is the case with the shorter end of the Treasury curve.

The second is that gold represents a hedge against central banks making a mistake with inflation. It has been so long since we had to account for inflation risk that people are unfamiliar with the toll it can take on investments. On this occasion the quantity of debt that has been issued represents a significant headwind for governments attempting to meeting coupon payments as the bonds are incrementally refinanced at higher rates.

Back to top