Email of the day on currencies and stock market performance:

Thank you for your always articulated views on the general macro. Highlighting the China risk (“China deserves an additional risk premium”) and the direction of credit spreads (“EU junk spreads have been on the rise in 2018”) are particular eye opening

One point on USD though. In your videos resp. online reports, you say / write that the USD should get stronger. One of the reasons you add to the commentaries is that the FED is on its hiking path and the interest rate differential makes the USD interesting relative to zero / negative interest currencies. In addition, you write that Gold suffer when nominal rate rise less than inflation (i.e. real rates rise) and when the USD is on the rise. I hope I am correct in the summary. Otherwise please correct me.

If I look at the recent history I am puzzled to note following: the FED started to raise rate in Dec 2015 and EUR/USD was at around 1.08 USd per EUR. Likewise gold was trading at something like 1’100 USD / Oz. at the same time.

How is it that 1+6 hikes later (1 in 2015, 1 in 2016, 3 in 2017 and 2 in 2018), EUR /USD is at 1.17 and gold is at 1.250 (and was 1300 just 2 weeks ago)? shouldn’t rate hikes make the USD interesting relative to ZIRP / NIRP countries like the EU Area or Japan?

Isn’t it that the current dollar strength is nothing more than an adjustment of a USD oversold condition prevalent until April? (due to lots of carry trades with EM currencies accumulated last year, most of which are done via a cross on the USD because of liquidity constraints with smaller currencies)

And that when the entire market hysteria around tariffs and on Trump tweets on NATO, on Germany and China retaliations threats etc. etc. calm, we will see the normal path of rising US interest rates and a falling USD combined with a rising JPY and EUR and rising Gold again? at the end of the day this makes sense. Otherwise it would be like a free lunch (buy USD, invest at higher rate and gain on the exchange rate). it cannot last forever.

Negative interest rates and ZIRP are deflationary policies. It makes sense for the EUR and JPY to appreciate.

Am I missing something?

Ps: if I look at history on other countries, higher rates are not supportive for a currency. Look at Turkey, Argentina, etc. All down sharply. the higher the rates to stem a crisis, the lower the currency.

On the other end, when the Bank of Russia reversed its super high interest rate policy after the 2014 crisis, RUB (and its equity market) started to recover. And RUB was also relatively stable during the most recent EM crisis

I would not be surprised to see TRY doing the same if the new governor reduces rates (the FT reported that Erdogan is not a fan of high rates) and the ministry of finance enact a policy aiming at reducing the current account deficit. Then TRY should recover despite the bad-to worst governance structure of the country

I would be interested in hearing your view on that

Best regards and nice holidays in China!

Thank you for this email which raises a number of points about currencies and what we can expect from various asset over the medium-term.

I think the most important thing to remember about currency markets is that they are a discounting mechanism just like equities and bonds. When we think about interest rate differentials it does not make sense to look at today’s levels because that is already in the price. We need to look further out.

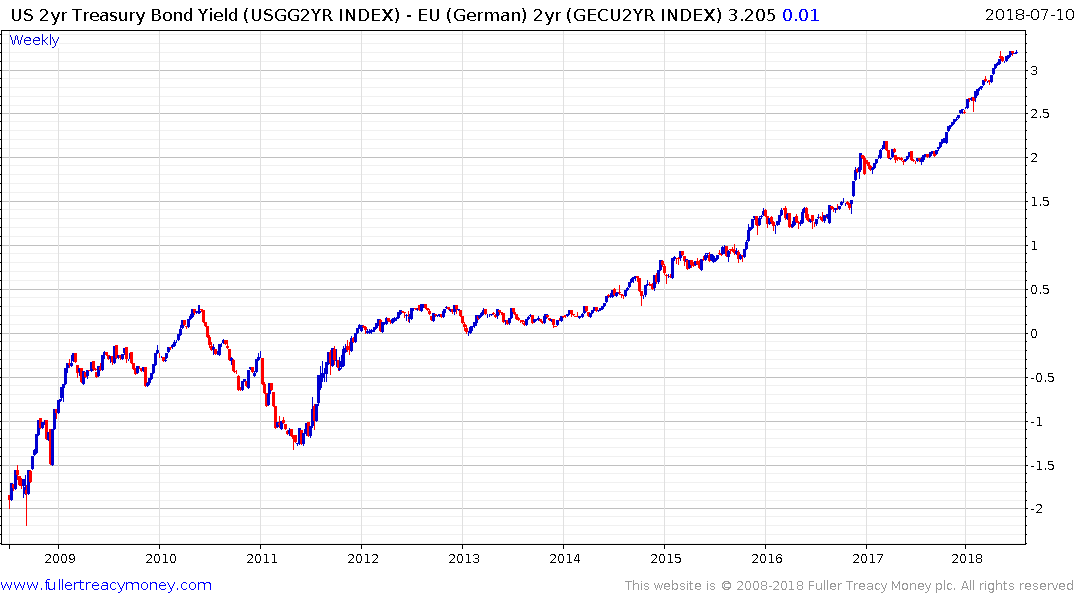

I created this chart of US 2yr yields over Eurozone 2yr yields and redenominated the Eurozone yield to US Dollars for a fair comparison.

Here is the same chart without the redenomination which suggests currency makes up about a 10-basis point difference right now.

The spread is now over 3% so it makes sense for Euro investors to hold US Dollars as long as it is trending higher. The other side of that trade is that it is expensive to be short.

The Eurozone has negative yields because of the ECB’s quantitative easing program and because investors are wary of thinking now is the right time to stop stimulating. If the USA stops raising rates or the ECB raises rates or follows through on its commitment to stop stimulated, then we will be at pivotal moments for the above spread which is likely to lead to the US Dollar’s advance rolling over.

That is when the most convincing argument for being long Euro, gold or the Yen will be made.

Europe, Japan, UK and Switzerland have zero interest rates because they are afraid of deflation. It’s exactly the opposite in troubled emerging markets which are forced to raise rates aggressively to stem outflows because of inflationary fears. They usually can’t lower interest rates again until inflation abates and that is generally a sign for international investors to come back in. That is why emerging markets tend to do well when elevated interest rates start to come back down.

It is certainly true that the US Dollar has more than unwound an oversold condition relative to emerging markets. I think even a casual perusal of spot rates tells us it is in a new uptrend against the majority.

The Dollar broke out against the Yen today suggesting it’s rally is more than a mean reversion.