Email of the day on batteries and the challenge of commodity supply

Congrats on your opinion on a larger correction and acting on it with put purchases.

Last week Double Line presentation had a chart that showed the performance of equity and the different credit subclasses, Ags., EM, HY, ClOs and so forth. Showed the large move by equities compare to credit over the same time period. It made me wonder how much further the equity correction can go.

You often follow interesting companies, you mention EQNR from Norway. have you ever looked a Freyr. It is also Norwegian and is involved in batteries. During the last days because of a report on its possible growth it had a huge move , but during this correction it may be a good opportunity, let me have your thoughts. Based on your comments how much the market has already priced in the EVs maybe it is not a good idea.

The move on copper is not a good signal

Trust all is well for you and your family

Thank you for these well wishes and questions which may be of interest to the Collective. Of my nine different long-dated put positions, the only one not in profit is Tesla and yet that is the one I have the greatest hopes for. They all have maturities in 2024, but I expect the point of maximum pessimism will arrive while they still have some time value.

There is no doubt that bonds have sold off aggressively. However, to conclude the bottom is in for stocks we will need to see some evidence both of capitulation and falling interest rates. Demand in the US economy is still strong. To illustrate that take a look at the container numbers arriving in Los Angeles port.

Before the pandemic it was highly cyclical with predictable peaks, troughs and wild swings in between. After the pandemic a new higher plateau has been reached and the seasonal cyclicality is gone. That means every month is Christmas for retailers.

Before the pandemic it was highly cyclical with predictable peaks, troughs and wild swings in between. After the pandemic a new higher plateau has been reached and the seasonal cyclicality is gone. That means every month is Christmas for retailers.

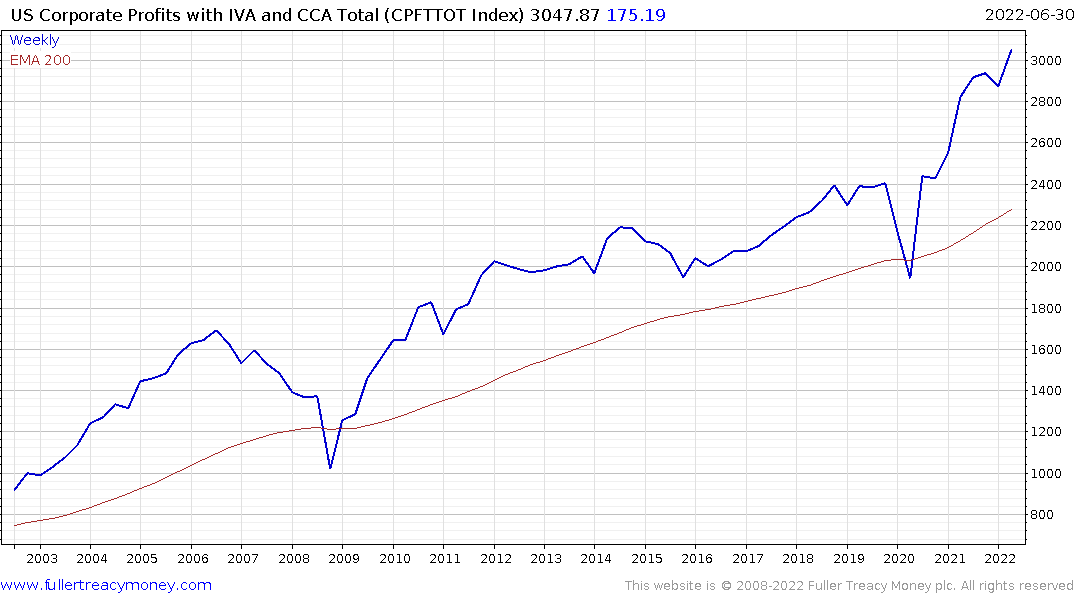

Interest rates are rising and liquidity conditions are tightening, but consumers have not pulled back from spending. That has continued to support corporate profits at record highs. Against that background, the Federal Reserve has no choice but to continue to raise rates. They will keep going until something breaks.

Interest rates are rising and liquidity conditions are tightening, but consumers have not pulled back from spending. That has continued to support corporate profits at record highs. Against that background, the Federal Reserve has no choice but to continue to raise rates. They will keep going until something breaks.

Large banks are trending lower. Goldman Sachs’ rebound was knocked back forcibly last week so it is no longer offering a counter argument to widespread weakness in the sector.

Large banks are trending lower. Goldman Sachs’ rebound was knocked back forcibly last week so it is no longer offering a counter argument to widespread weakness in the sector.

The epicentre of risk in this cycle is in the private equity sector. Faced with low interest rates pensions poured money into private equity ventures. The covenant-lite structure of those issues offers scant protection in a downturn.

The longer higher rates are sustained for, the greater the potential for a significant drawdown in leveraged loans. Private equity has prospered for a decade by fudging numbers and having no requirement to mark to market. That will change if coupon payments become difficult to service or refinancing becomes challenging. That tightening liquidity environment is also a factor in copper's underperformance.

That’s a long way of saying I do not believe this downtrend has reached bottom.

I last reviewed battery manufacturers on September 14th.

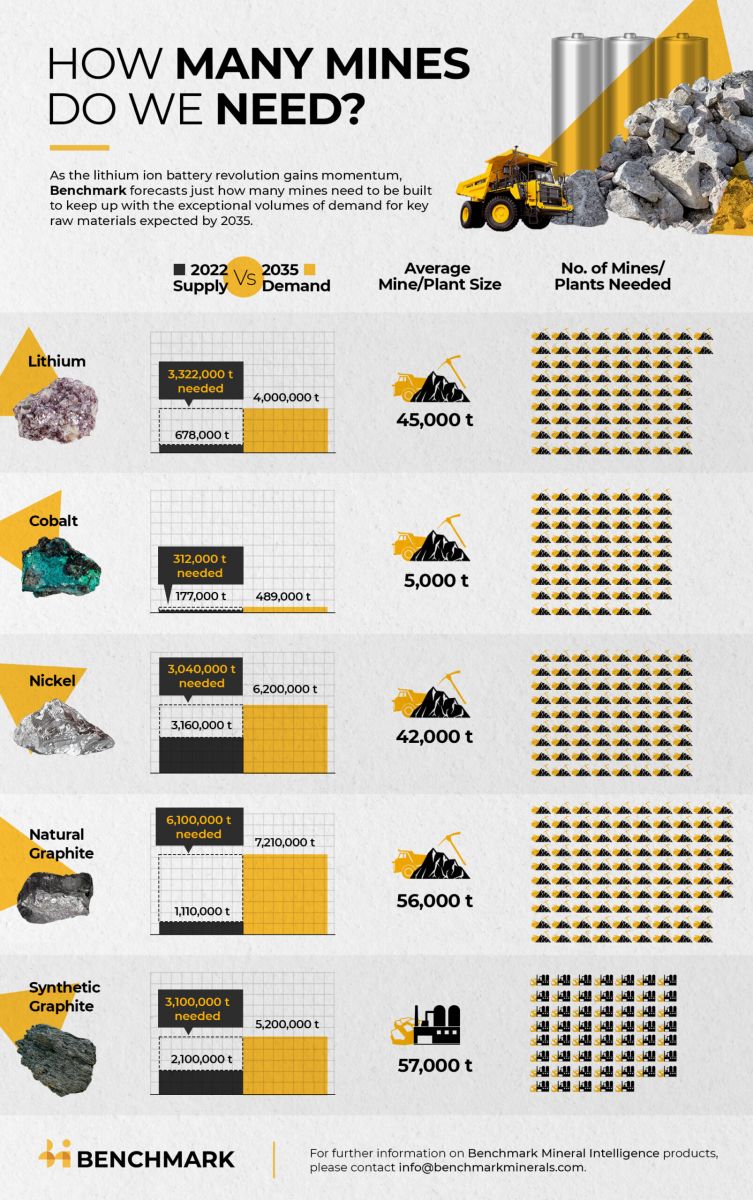

This report from Benchmark Minerals Research may be of interest to subscribers. Here is the important graphic highlighting how many new mines will need to be built to meet 2035 targets.

I agree with the prediction there will be more demand for batteries. However, not all batteries are going to be reliant on lithium. Solid state batteries are probably a pipe dream without significant innovation in developing lithium assets. Their anode is solid lithium so that could end up being cost/commodity accessibility prohibitive.

I agree with the prediction there will be more demand for batteries. However, not all batteries are going to be reliant on lithium. Solid state batteries are probably a pipe dream without significant innovation in developing lithium assets. Their anode is solid lithium so that could end up being cost/commodity accessibility prohibitive.

Freyr Batteries is developing lithium-ion batteries using renewable energy as a sales pitch but that will not free it from the commodity limitation.

Freyr Batteries is developing lithium-ion batteries using renewable energy as a sales pitch but that will not free it from the commodity limitation.

ESS is developing iron redux flow batteries which do not rely on commodities in limited supply. These utility scale solutions have a clear path to commercialization as demand for back up power grows significantly over the next decade.

ESS is developing iron redux flow batteries which do not rely on commodities in limited supply. These utility scale solutions have a clear path to commercialization as demand for back up power grows significantly over the next decade.