Email of the day on a bullish case for bonds

Globalization, improving technology, high unemployment, low wage growth, excess capacity and increasing supply, especially of commodities, should lead to lower prices. This is deflationary. Despite Friday’s move, the gold price has been telling us that deflation threatens. The following recommendation to buy bonds is taken from Rambus Technology. It seems logical.

“PM and commodity decline is signalling deflation despite the FEDs attempts to counter it and this will power long term government bonds upward. As the world’s reserve currency a major part of all world- wide debt is denominated in US dollars. As marginal countries are forced to de-lever it will act as a short covering of the USD and force the USD to rise. As the economies of peripheral nations falter it will drive capital towards the core which is the USD and its economy. This will continue to stoke our Sovereign bond market until the currency becomes suspect. Just as occurred in the great depression government bonds should rally until we reach a point of banking conflagration as we did with the failure of the Credit Anstalt Bank in May 1931. By then gold should resume its traditional role of being an asset with no counter party risk and last ditch store of value. This is how we should transition into the next bull market in gold. It won’t be an easy transition as Mr. Market will do his utmost best to throw off initial bull believers just as he has done to the bears on the way down. Until a similar banking crisis emerges US Government bonds should rally and interest rates decline. At present US interest rates hover above those of most developed nations and its easy to imagine how with a stronger USD rates can at least match that of other nations. Hoisington is forecasting long US rates to fall to a range of 1.7-2.3%.”

The full report is here:

Thank you for this thought provoking email. I agree that the relative strength of the US economy and the concordant strength of the US Dollar represent bullish considerations for US Treasuries. The Fed’s Total Foreign Holdings of US marketable securities Index is reported with a five-month lag but remains on an upward trajectory and stood at $6 trillion at the last update. This is not a timing indicator but the trend is clear and there is no reason to believe it will reverse with the ending of QE.

Falling commodity prices are disinflationary rather than outright deflationary because they encourage rather than impede productivity growth in the wider economy. Therefore I am cautious of drawing to hard a conclusion from that trend at the current time. Just how low oil falls will be a major determinant on the deflationary effect since the sector represents such a high proportion of capital expenditure for the US economy.

Commodities are not included in PCE Deflator model which the Fed uses to measure inflation but wages are. With labour participation beginning to recover and increasingly clear calls for higher minimum wages, the potential for that source of inflation to reappear is increasing.

Right now, we can conclude that the benign scenario of a recovering economy, falling deficits and gradual normalisation of Fed policy is playing out. The big question is whether the bullish considerations for Treasuries can continue to buoy momentum when the Fed is no longer the purchaser of first resort.

US 10-year Treasury yields hit an important low in 2012 near 1.38%. In all likelihood this represents the low for the secular decline. A type-3 bottoming process appears to be underway where a progression if mildly rising lows, interspersed with some dramatic volatility, is evident. Yields spiked lower in October and continue to unwind that move. A sustained move above 2.5% would be required to suggest a return to supply dominance beyond the short-term.

.png)

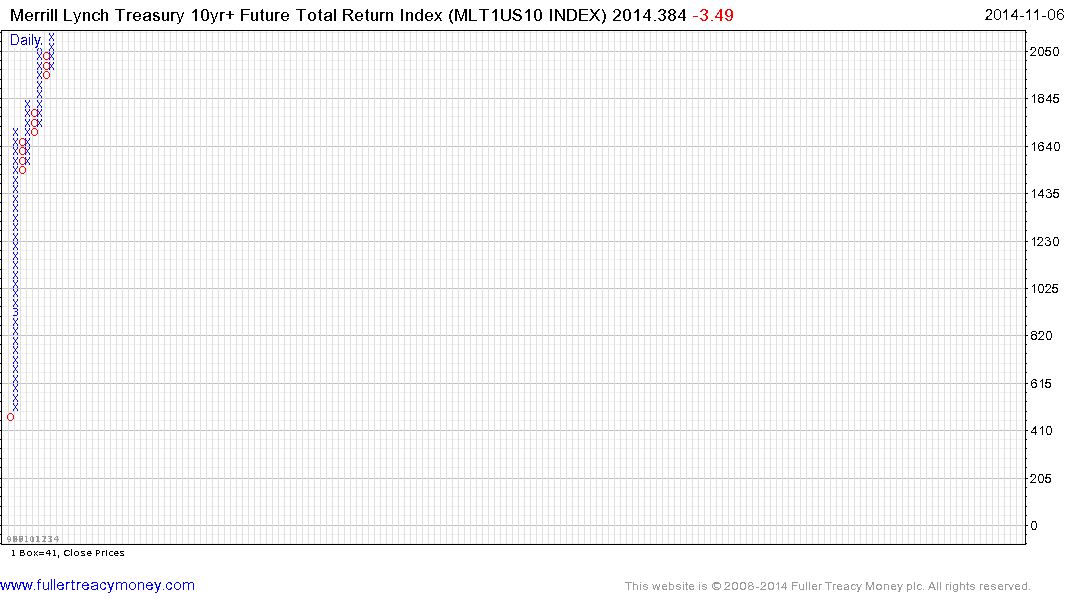

The Merrill Lynch 10yr+ Total Return Index hit a new all-time high in October and is now unwinding the short-term overbought condition.

The point & figure chart offers an excellent depiction of the trend’s consistency. The pace of the linear advance has changed in the last few years but the progression of higher reaction lows remains intact. A sustained move below 1920 will be required to confirm a change of trend. In the absence of such a move, the bears will have little evidence of top formation completion.