Email of the day (2)

“I had noticed the strength of the Nikkei. Can the U.S. 10 year be far behind?"

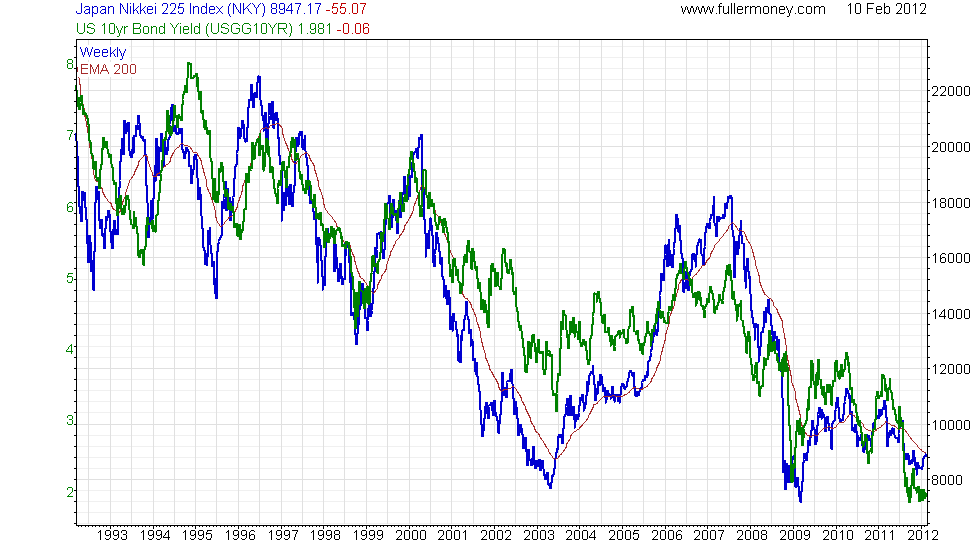

Eoin Treacy's view Thank you for this topical question. Over the years, many investors have used this overlay to represent the preference of Japanese investors for foreign assets rather than their domestic stock market. As one of the largest creditors in the world, holding the second largest position in US Treasuries there is some justification for this view. However there are a number of caveats.

While the two measures moved in lock step between August and January, there are plenty of examples where they have diverged over the last year as well as over longer horizons such as 5 years, 20 years or 50 years. At some point, probably within the next decade, Japan will need to start liquidating its savings to pay pensions. That could pressure US Treasury yields higher but there are other factors to consider.

Unlikely as it may seem, Japan may decide to grasp the nettle of its high debt to GDP ratio. It may also reform the pension system which would decrease the need to liquidate its foreign assets.

Alternatively, the Federal Reserve might not have to support the Treasury market through quantitative easing if growth continues to recover. The only reason it continues to increase the supply of money is because the velocity of money is so low. If economic activity picks up, there will be less need to artificially supress yields.

While viewed as risible only a few years ago, our contention that the USA could become energy independent within a decade has been taken up by a wide number of pundits of late. This is primarily because supply growth from shale oil and gas continues to outstrip expectations and the USA has abundant supplies of both. The USA's fiscal problems, trade deficit and unfunded liabilities all still need to be addressed but become much less daunting issues with energy independence.

While the above points are still conjecture, price action represents reality and we will be guided by it. US 10-year Treasury yields accelerated lower in August and lost momentum in the region of 2% where they have been ranging since September. They continue to exhibit an upward bias but a sustained move above 2.3% will be required to confirm a return to supply dominance.

{kind=link}