Email of the day (1)

“ If my memory is right, you have been discussing potential rotation away from recently popular consumer stocks into beaten down mining and industrial stocks. I thought the graph below would be of interest. ”

Eoin Treacy's view Thank you for this long-term ratio which is sure to be of interest to subscribers and yes I have been discussing the potential for rotation in the Subscriber's Audio for the last couple of weeks.

Fullermoney has favoured the consumer sector for a number years because so many of these companies fit the requirements we look for in an Autonomy. They are truly global with household name brands that instil consumer loyalty. They have strong records of building businesses overseas and many are no longer dependent on their domestic markets to revenue growth. They tend to have strong balance sheets and a significant number have impressive records of dividend growth. The global population went from being mostly rural to mostly urban in the last few years. As cities grow, productivity tends to improves. The associated growth of the consumer sector represents a powerful investment proposition for the long-term.

However, despite the allure of the fundamental story, which an increasing number of people find inspiring, we can only deal with the reality provided by the market. The simple fact is that when prices become wildly divergent from a trend mean such as the 200-day MA, the temptation is to become more bullish because we want the good news to keep coming. However the risk of a reversion back towards that mean increases even as sentiment becomes progressively more complacent.

For example Johnson & Johnson represents a cross section of the medical devices, pharmaceutical and consumer healthcare sectors. It has increased its dividend for 40 consecutive years and possesses an enviable suite of globally recognised brands. The share price spent a decade ranging mostly below $70 from 2002 which coincided with a lengthy process of valuation contraction where expectations of upside potential deteriorated considerably. The share broke successfully above $70 in January and rallied for 17 of the last 18 weeks before encountered at least near-term resistance close to $90 this week. This was a remarkably impressive breakout and suggests in no uncertain terms that Johnson & Johnson is now in a new bull market environment.

However the short-term risk is that this impressive four-month advance is now consolidating. This would allow the overextension relative to the 200-day MA to be unwound. From the perspective of someone who does not have a position the risk/reward of buying today is heavily outweighed by the potential for a more favourable entry point following a reversion to the mean. For anyone with a position the best time to lighten is following a major advance and the best time to increase the position is following a reversion to the mean. Alternatively one might simply decide to wait out any potential reaction since the medium to long-term potential is so appealing and a buy-and-hold strategy is likely to be handsomely rewarded.

A wide swathe of the consumer sector has completed lengthy base formations in the last couple of years and would be best bought following reversions to the mean.

At the other end of the spectrum the materials and mining sector have been subject to concerted selling pressure and have borne the brunt of fears over slowing economic growth, cost overruns, declining standards of corporate governance and in some cases oversupply. They have been among the worst performing sectors in the global beauty contest this year but an increasing number have lost downward momentum and have the capacity to outperform if the consumer sector moves into a process of mean reversion.

For example Germany listed Linde AG is part of an oligarchy that dominates the industrial gases sector along with Air Liquide and Praxair. The share found support in the region of the upper side of its underlying 18-month range at the end of April and a sustained move below €140 would be required to question medium-term scope for continued upside.

Austria listed Voestapline is a steel producer and has held a mild upward bias within its two-year base. A sustained move below €24 would be required to question medium-term scope for continued higher to lateral ranging.

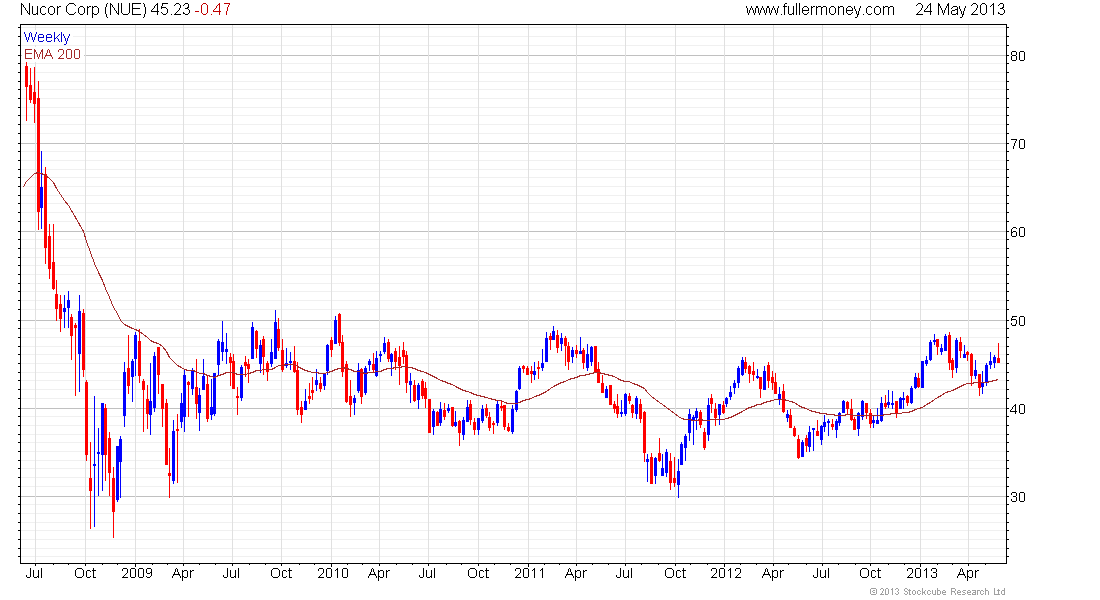

The USA's largest steel producer Nucor continues to range higher and is approaching the upper side of its almost four-year base.

Returning to the long-term ratio you so kindly forwarded, when such a deeply oversold condition is evident the potential for at least a partial unwind of that condition increases substantially. One consideration at the back of my mind has been that a great deal of negative news has been priced in to materials and basic resources shares. If the macro environment is seen to improve a rerating of the sector is possible.

{kind=link}