Email of the day (1)

"Your Rockefeller quote has prompted me to alert the Fullermoney community about the potentially dilutive effect of scrip dividends and hence the reliability of the quoted dividend yield of some companies. This may be relevant to the screening of Autonomies where dividend yield is an important consideration..

"I work for a bank with an extraordinary high dividend yield (12.5 per cent as of Friday's close). I was mentioning to a colleague that at this level you had to question the sustainability of the dividend. He pointed out that since nearly 90 per cent of the dividend was being taken in scrip form, we were getting less of a dividend and more of a stock split. Very little cash is going out of the bank but the number of shares in issue is continuing to rise dramatically which is akin to what happens in a stock split.

"Obviously, this is an extreme case but it did illustrate to me that the dividend yield can be a somewhat misleading term if most of the payout is non-cash.

"On a separate note, David, your commodities call ("supply inelasticity meets rising demand") ten years ago was amongst the calls of the decade and it would not surprise me if in eight years time I am making a similar comment about your Autonomies call.

"That said, don't you think the commodities story is now approaching its past-it date. A lot of mining projects commissioned ten years ago are now coming on-stream whether it be in Western Australia, Mongolia or Brazil. Copper trades today at nearly eight times where it was at the start of the boom. The worst excesses of the Fed and ECB balance sheet expansion should be behind us. Should one begin to underweight Commodities now (perhaps with the exception of Energy)?

"Thanks and keep up the great work."

David Fuller's view Thanks for your kind words and an email

certain to be interest to many other subscribers.

It has

been a while since I have heard about script issues and had hoped that the fashion

for them in earlier decades had died out. I do not feel that they should be

labelled as dividends and regard them as largely meaningless. However, they

can be a minor nuisance in terms of disposal as you will have to pay a commission

and the proceeds will still be treated as income in most countries. The only

dividends that I am interested in are in the form of cash. I have assumed that

the dividend yield listed in the FT, WSJ or financial services such as Bloomberg

refers to cash payments only. I would be very surprised if any Dividend Aristocrats

considered script issues in this decade.

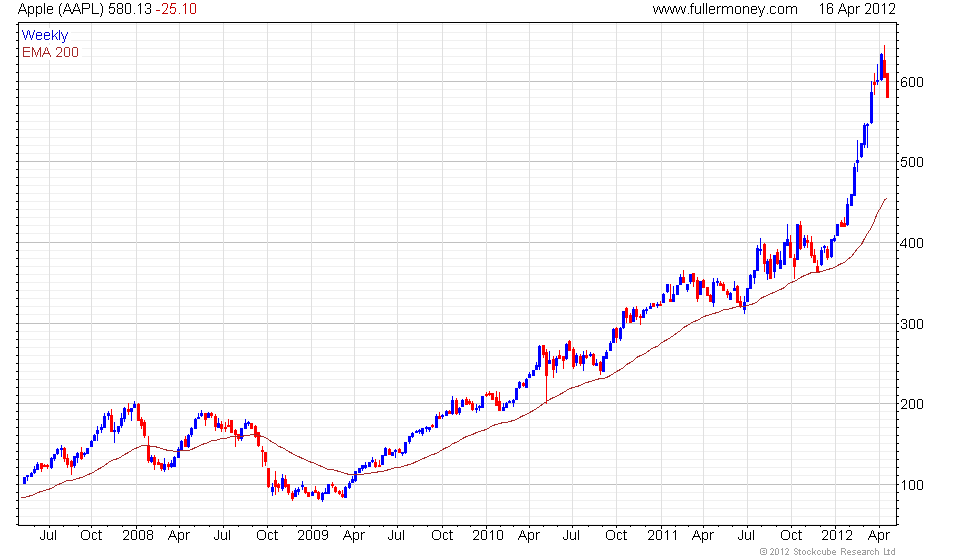

Regarding

Autonomies, those that satisfy global consumer demand, such as Coke,

Nike, McDonald's

and particularly Apple have done exceptionally well,

to the point that they are now experiencing corrective phases towards their

trend means approximated by the 200-day moving averages. This will provide additional

buying opportunities and on a longer-term basis and subject to continued good

management, I think they have every chance of rewarding investors, given that

the global growth in middle classes should remain a secular theme.

Regarding

commodities and using my shortest definition of Autonomies - multinational sector

leaders - I regard BHP Billiton as the

leading industrial resources Autonomy. However, it is certainly performing like

a cyclical rather than growth share at present. China's growth has slowed somewhat

and more importantly the central government has reined in property speculation.

There may also be less infrastructure build during the current political transition.

Also, your point about long-term mining projects that are now coming on stream

is correct. How much of this is already factored into the share price is hard

to say but with a current yield of 4% and a 5-year dividend growth rate of 28%,

according to Bloomberg, I feel that I am being compensated for my patience.

It depends on how actively you wish to manage your portfolio but see also the

report immediately below.

{kind=link}