Email of the day (1)

"With Spanish and Italian bond yields pushing higher as the threat of contagion looms, how do you see this playing out for equities, gold and the European bonds themselves?

"Many thanks for the excellent coverage."

David Fuller's view Many thanks, not least for an important

and challenging question.

The

answer is that I do not know, and neither does anyone else because the situation

goes right to the heart of the euro's survival in its current form. There is

not much precedent for today's European single currency problems, although events

have been drifting in this direction for over two years. Astute observers such

as Tim Price lost confidence in the containment or muddle through prospects

long ago and the markets seem to be catching up with that view. The more bearish

phases increase uncertainty among investors and traders, leading to further

deleveraging.

What

we do know is that the process of deleveraging and a flight to cash often includes

indiscriminate selling. There has certainly been a whiff of panic in the markets

over the last two days. This has caused a temporary downdraught which is certainly

not the orderly consolidation that I would have hoped for following the preceding

two to three-week rally for stock markets.

What

we really know regarding the eventual consequences of this long, drawn out sovereign

debt crisis is actually very little in terms of practical value today. However,

what we can see is very helpful. For the duration of this single currency problem,

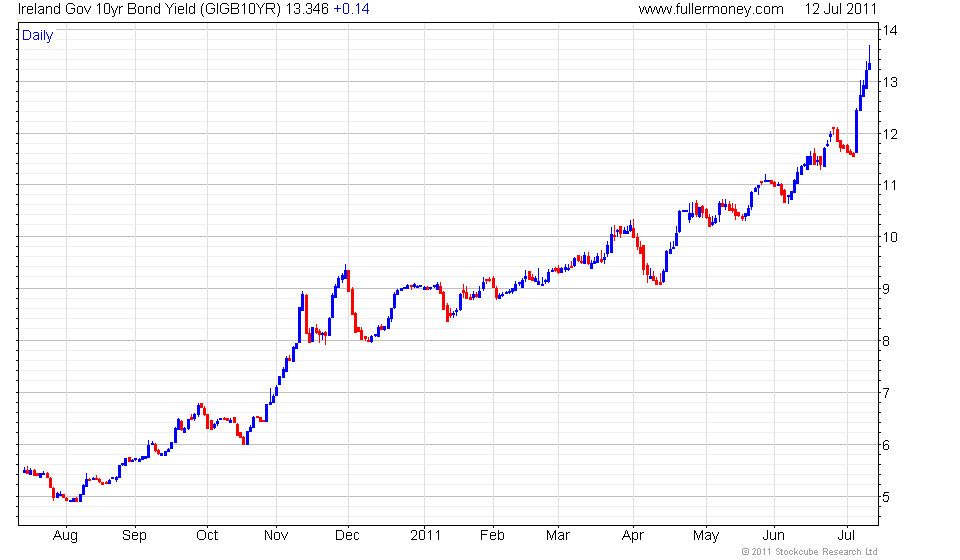

I think it is a good idea to have charts for the 10-year bonds yields of the

'crisis' economies in one's 'Favourites' section of the Chart Library. We need

them all because the attack in terms of higher yields often rotates from one

to another. First it was Greece (weekly

& daily), then Portugal (weekly

& daily) and most recently Italy

(weekly & daily).

We should also keep a close eye on Ireland (weekly

& daily) and Spain (weekly

& daily) because they have been

in the firing line. We should also include German 10-year yields (weekly

& daily) in this group because

they are viewed as the 'safe haven'.

When

yields for one of the countries above break to the upside, as the daily chart

for Italy's 10-year yields did last Wednesday, and it was not alone, we have

been warned. Upside follow through intensified the warning. You can see that

Italian 10-year yields accelerated higher yesterday and also today - a 5-day

advance of 100 basis points - before falling back this afternoon. The acceleration

led to panicky deleveraging in some stock markets and other assets this week,

before the partial pullback in Italian yields steadied nerves somewhat.

Where

government bond yields are in clear overall upward trends, as you see with the

periphery Euroland countries above, their stock markets will inevitably underperform.

Yield spikes can lead to contagion selling in other stock markets, and not just

in Europe, as we have seen yesterday and today. However, if we ask ourselves,

what lasting effects will this have on ASEAN stock markets, India, Australia,

etc, the answer is not a lot. Therefore setbacks due to contagion selling create

buying opportunities in markets which are not directly embroiled in the same

problems.

Commodities

have had an unusually high correlation with stock markets in recent years. Therefore

when global stock markets are weak, precious metals and most other commodities

will be susceptible to contagion selling. The main exceptions have occurred

when supply shortages were a concern for the commodities in question. The converse

has also been apparent, with prices for many commodities rising when stock markets

are rallying.

{kind=link}