Email of the day - on rising inflationary pressures

I am building a garage-workshop (2,200 sq ft) at my home in Arizona, in a mid-sized community (100,000 population spread out in 4 towns) which is experiencing the most rapid growth in its history, thanks to the socio-economic disaster in the state to our West (California). About 1,000 new homes are being constructed this year, with 9,000 additional already authorized by the county. Similar growth rates are happening in many other desirable parts of the country, like Austin, Texas and Boise, Idaho.

My project is competing with this construction frenzy, and I am experiencing substantial delays in construction as high-quality contractors are beset with material delays and cost overruns, plus a labor market dramatically harmed by government handouts coupled with high labor demand. Real inflation should be measured using real facts and versus longer-term averages, not the current crap methods...

This article includes a letter from the CEO of a metal roofing manufacturing company - who does not mention (but maybe should have) how hard it is (read soon to be more expensive) to get and retain qualified employees... which I would add to the article to round out what it says...

[I believe the article can be freely republished with attribution.]

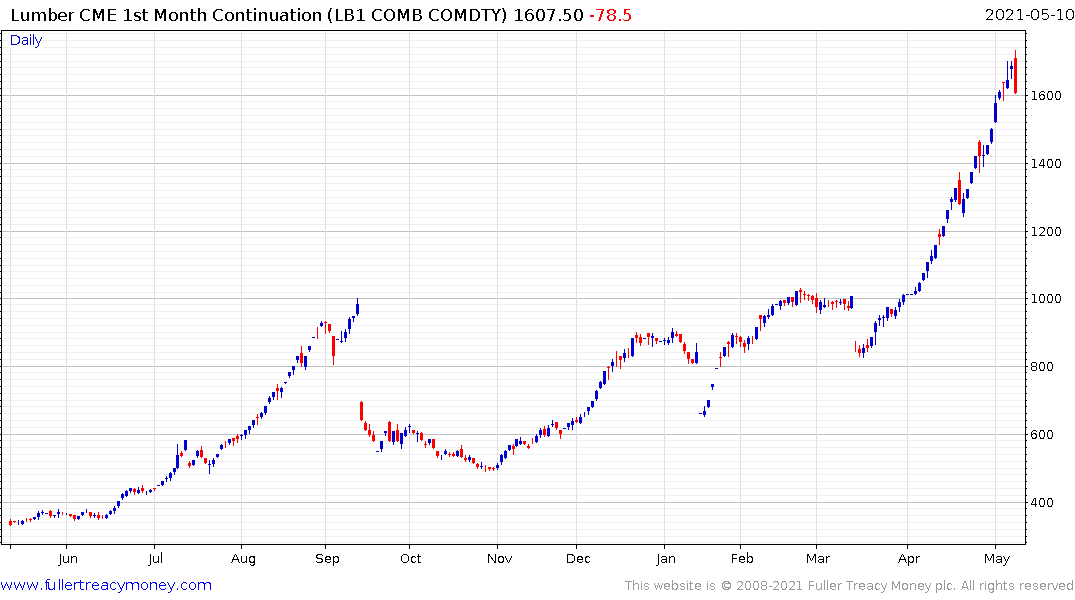

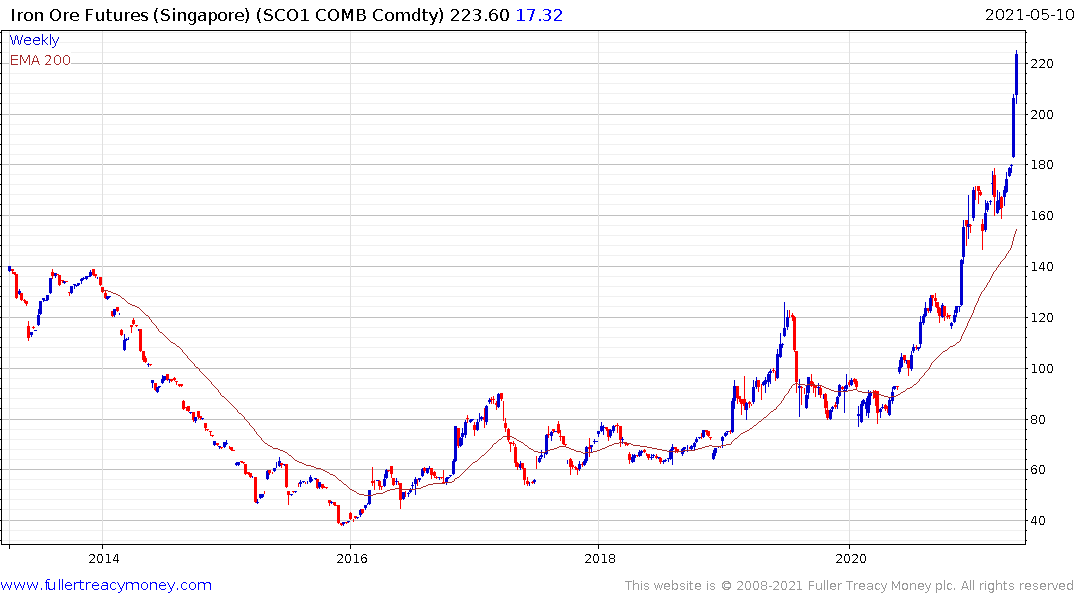

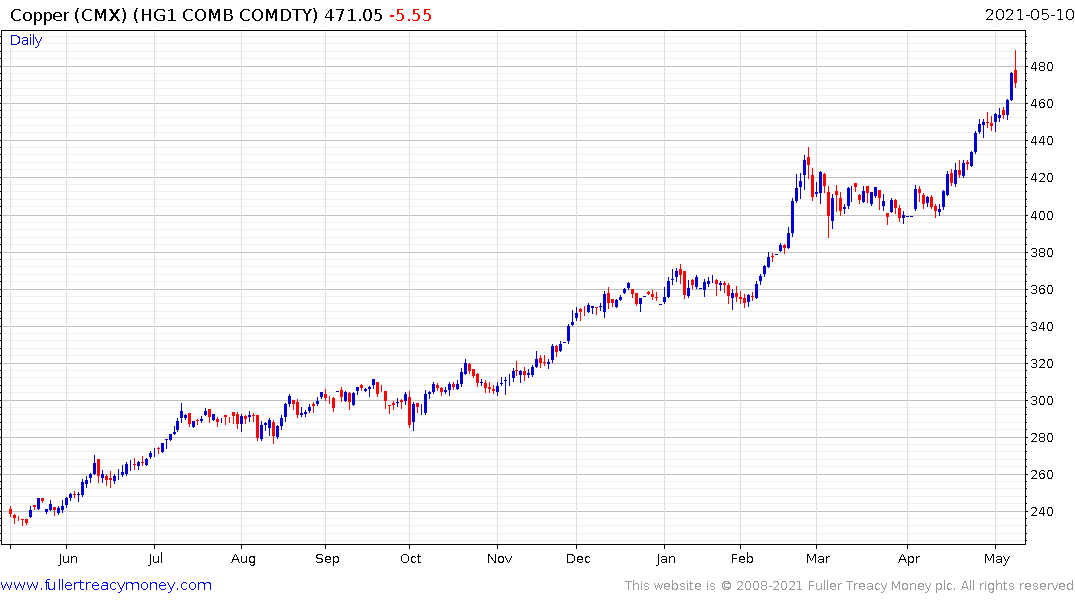

Lumber, iron ore and copper prices have accelerated higher as investors binged on supply inelasticity trades. Prices are now getting to points where substitution demand is evolving. I priced the cost of a new kitchen hood cover over the weekend. It is now only marginally more expensive to have it done in stone than wood.

I’m reminded of the craze for adorning London’s landmark buildings with pineapples in centuries past. Limited supply creates demand but also incentivises new supply to come to market.

The oldest adage in the commodity markets is “the cure for higher prices is high prices”. That’s particularly true for commodities that are reasonably easy to increase supply.

Lumber supply is more about a lack of workers and the speed with which closed mills can be reopened. There is no shortage of trees. Today’s limit down day is a shot across the bows for the trend. If the decline holds for more than a couple of sessions it will likely mark a peak of medium-term significance.

China’s trade spat with Australia, coupled with continued lacklustre Brazilian exports are supporting the acceleration in iron-ore prices amid China’s reflationary demand boom. At least some consolidation of recent gains appears likely following the recent acceleration.

Copper is benefitting both from significant new demand and long lead times to develop new resources. Nevertheless, the price has raced to new highs and it would not be surprising to see some consolidation relatively soon.

Our abiding adage from the last commodity bull market was “don’t pay up for commodities”. They are capable of impressive moves both up and down and rarely fail to disappoint the most ardent latecomers to the party.

This report from JPMorgan by Marko Kolanovic may also be of interest. Here is a section:

With inflation on the rise, the current debate is how long this trend will persist. The question that matters the most is if asset managers will make significant change in allocations to express an increased probability of a more persistent inflation. We think this shift in allocation will happen (regardless of how temporary inflation is), and new data points related to inflation will on margin cause investors to shorten duration, move from low volatility to value, and increase allocations to direct hedges such as commodities. We expect this trend to persist during the reopening of the global economies in the second half of this year. Given the still high unemployment, and a decade of inflation undershoot, central banks will likely tolerate high inflation and see it as temporary. Portfolio managers likely will not take chances and will reposition portfolios. The interplay of low market liquidity, systematic and macro/fundamental flows, the sheer size of financial assets that need to be rotated or hedges for inflation put on, may cause outsized impact on inflationary and reflationary themes over the next year.

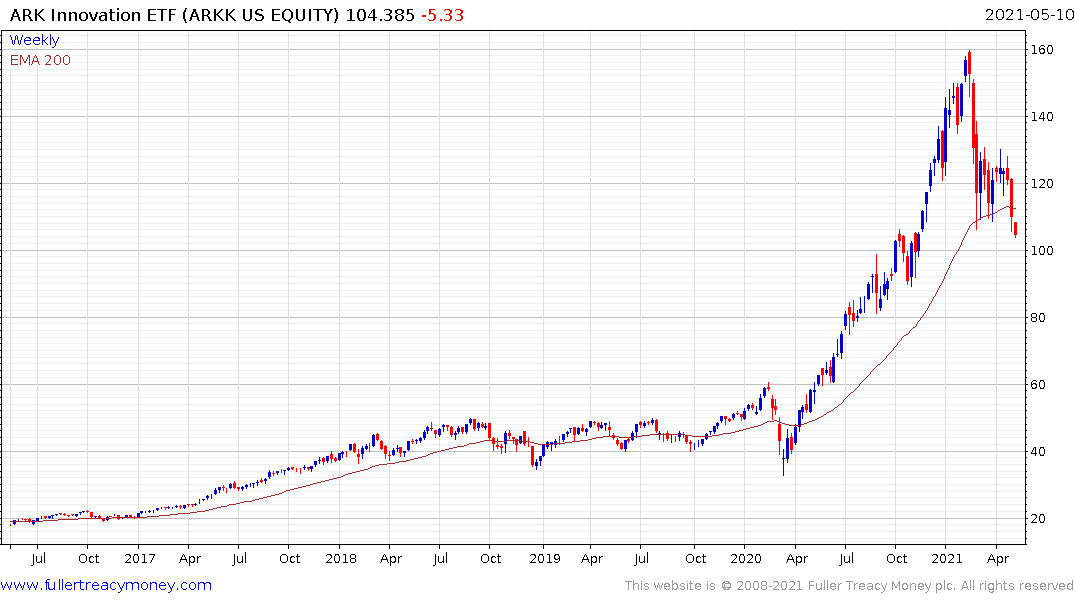

In practise, fears of inflation remove support for unprofitable companies with aggressive valuations. The Stay-At-Home champions are increasingly rolling over while dividend aristocrats and value strategies are outperforming.

The gold price has been correcting for nine months and is showing increasingly convincing signs of bottoming. The idiosyncrasies of crowd psychology are that very few investors are paying attention to gold and instead tend to chase accelerations.

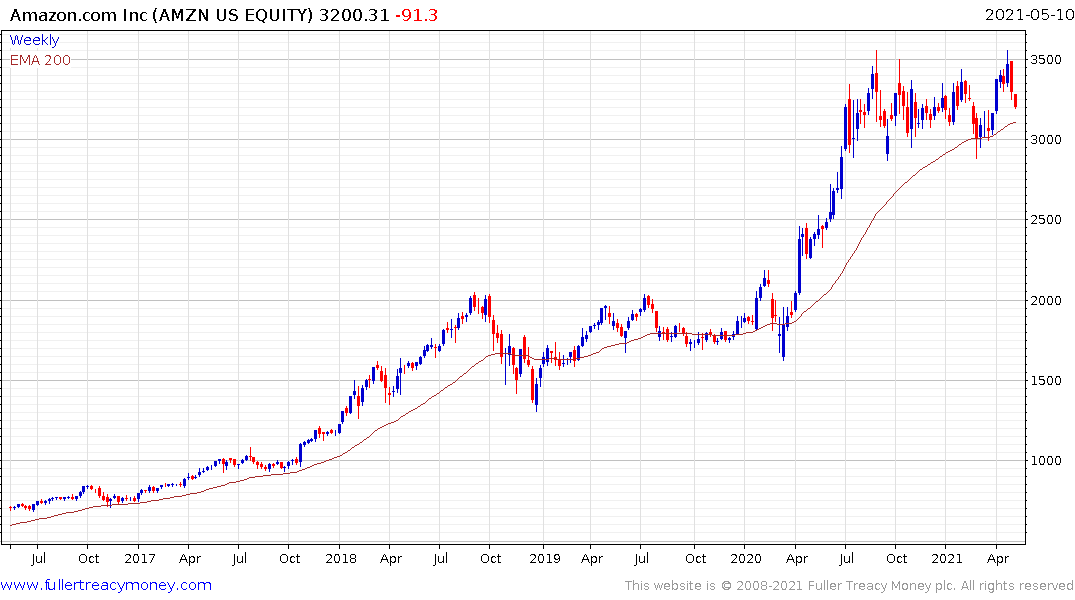

The loss of momentum and failed upside breaks on shares like Nvidia, Amazon, Apple, and Netflix are warning signs that a significant rotation will weigh heavily on last year’s winners.