EconoMIX: Who will win the trade war

Thanks to a subscriber for this report from Mizuho by Yuchiro Nagai which may be of interest. Here is a section:

It is not possible to analyze today’s Japanese economy without considering the impact of the formation and collapse of the bubble and enormous fiscal deficits. The two policies that originated in the Structural Impediments Initiative noted above are intimately related to these phenomena. The policy coordination severely restricted Japan’s fiscal and monetary policies, which when combined with the sudden financial liberalization of the time and the delay in BoJ tightening, is frequently cited as a cause of the rise and fall of the bubble. The increase in public works investment of the Structural Impediments Initiative is also singled out as a remote cause of the fiscal deficit.

In fact, Japan’s fiscal and monetary policies have long been repeatedly swinging from success to failure. We cannot pin all the blame for the bubble’s expansion and collapse and for the fiscal deficits on the Structural Impediments Initiative in light of such macroeconomic shocks as the Japanese financial crisis, the Asian currency crisis, the GFC, and devastating natural disasters as well as the responses to these. Nonetheless, it is a deeply rooted view that there is a cause-and-effect relationship between the bubble and international policy coordination, including the impact of subsequent BIS regulations on Japanese financial institutions.

China had intensely researched Japan-US trade friction prior to the recent escalation of trade issues between it and the US. Chinese policymakers appear to view the Plaza Accord as responsible for causing Japan’s bubble and subsequent downturn and they are considered reluctant to substantially adjust the exchange rate as a result. Given the major changes to the environment for the Chinese yuan, this view is not necessarily correct now, but it is still highly likely that China has looked at Japan’s experience as an object lesson, including the Japan-US Structural Impediments Initiative.

Here is a link to the full report.

The extent to which the Plaza accords were instrumental in weakening the Dollar and thereby strengthening the Yen and how much that contributed to the bubble and subsequent stagnation in the Japanese economy is a major concern for the Chinese economy today.

Here is a section from a related report, also from Mizuho, discussing the likelihood for a lose/lose outcome to the deteriorating state of US and Chinese trade relationships.

Some in the market have a tendency to believe that the objective of the US’s trade war with China is to benefit the US economy. However, Messrs. Mearsheimer and Navarro’s aim is to weaken China. From an economic perspective, this is not a winwin situation but a lose-lose situation. Mr. Mearsheimer notes that it is difficult to state confidently that mutual economic dependence will be a firm foundation for defending the peace of Asia in the coming decades.

Mr. Navarro is more extreme. He believes that in a time when the US is searching for a new balance in its trade with China, it is unclear whether such economic, political, and ideological barriers will be surmounted. He believes that whenever consumers buy a product made in China, they are contributing to the fortification of China’s military prowess, which could damage themselves and their country. The economic, political, and ideological barriers Mr. Navarro mentions are the higher inflation rates that would accompany a US–China trade war, which would unfairly burden the poor, and resistance from the right, which has always advocated free trade. He believes they are fatalist, premeditated criminals.

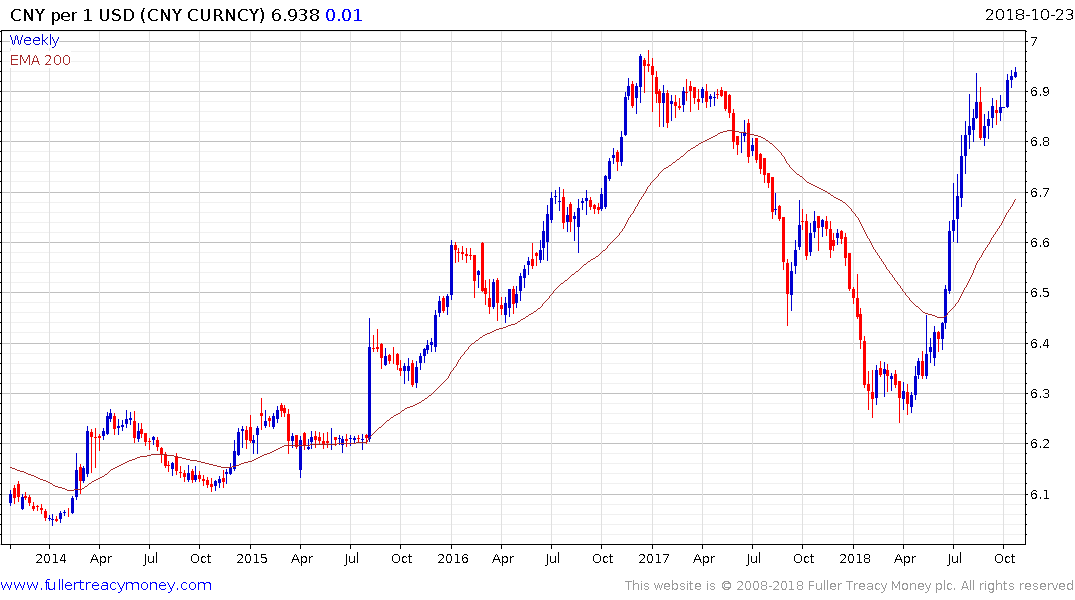

This suggests it is inevitable China will continue to use the Renminbi as a policy tool to protect the domestic economy from the full force of international tariffs. That is likely to result in even more overbearing regulation of the economy because of the risk of capital flight. It is also an incentive for the Chinese to stimulate the domestic economy and expand the nascent fiscal stimulus which began over the weekend with tax cuts for individuals. This is potentially a bullish catalyst investors’ have been waiting for to participate in the market. It may be all but essential considering the downward pressure that continues to build in the property market.