ECB's Villeroy Sees Rate Hike Quarters, Not Years, After QE

This article by Piotr Skolimowski, Jana Randow and Alessandro Speciale for Bloomberg may be of interest to subscribers. Here is a section:

European Central Bank policy maker Francois Villeroy de Galhau said the institution’s first interest-rate increase could come “at least some quarters, but not years” after policy makers end their bond-buying program.

In an interview in Paris, the French central banker played down concerns about the euro area’s first-quarter economic slowdown and signaled that the ECB is still likely to halt quantitative easing this year. He said inflation will resume its acceleration in coming months, with underlying price pressures set to strengthen as the bloc’s temporary weakness passes.

“We will probably give additional guidance for the end of the year for the timing of the rate hike and the contingencies,” Villeroy said in a Bloomberg TV interview with Francine Lacqua.

“We’ll see exactly how we formulate it. We’re predictable, and it’s a clear virtue of our gradual normalization path, but we are not precommitted.”

ECB policy makers have yet to formally discuss the future of their QE program. Purchases are currently scheduled to run until at least September, totaling more than 2.5 trillion euros ($3 trillion), and officials expect interest rates to stay at current record lows until “well past” the end of net buying. Maturing debt will be reinvested.

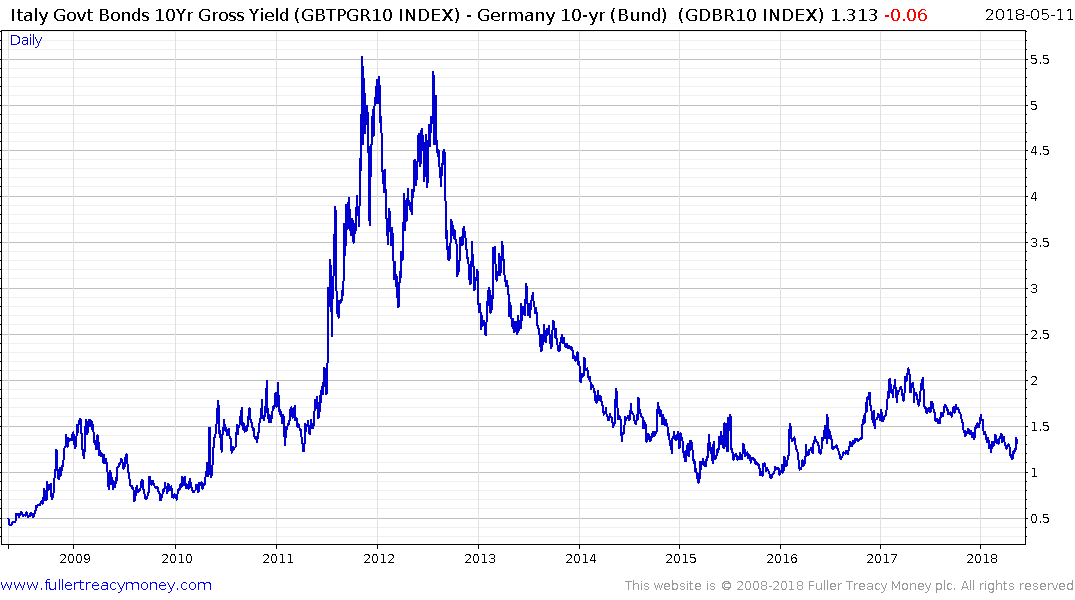

It could be argued Germany, Netherlands and maybe Austria are ready for higher interest rates. Since together they make up a substantial proportion of the Eurozone economy that is what the focus of ECB actions is likely to be.

Concurrently, the new populist Italian government is aiming at a flat tax to appease the people in the North and a guaranteed basic income to appease those in the South. Fiscal stimulus for one of the world’s most indebted countries would normally be greeted with some skepticism by the bond market but the ECB is still a major supporter of Italian bonds so there is little movement.

Nevertheless, if the ECB does in fact stop its purchase program in September, a mere four months from now, where will that leave the Italian bond market? It seems to me that spreads over Bunds which have been contracting over the last year are about as tight as they are likely to get and that there are substantial risks of a sell-off if investors take fright at the prospect of the ECB no longer supporting the market with new purchases. After all the US Treasury market experiences its “Taper Tantrum” when it initially stopped new purchases and arguably, the Eurozone has more challenging fiscal issues.

The Euro retested the psychological $1.20 area today but needs to sustain a move back it to signal more than temporary support.