Draghi Sees Almost $1 Trillion Stimulus With No QE Fight

This article by Simon Kennedy for Bloomberg may be of interest to subscribers. Here is a section:

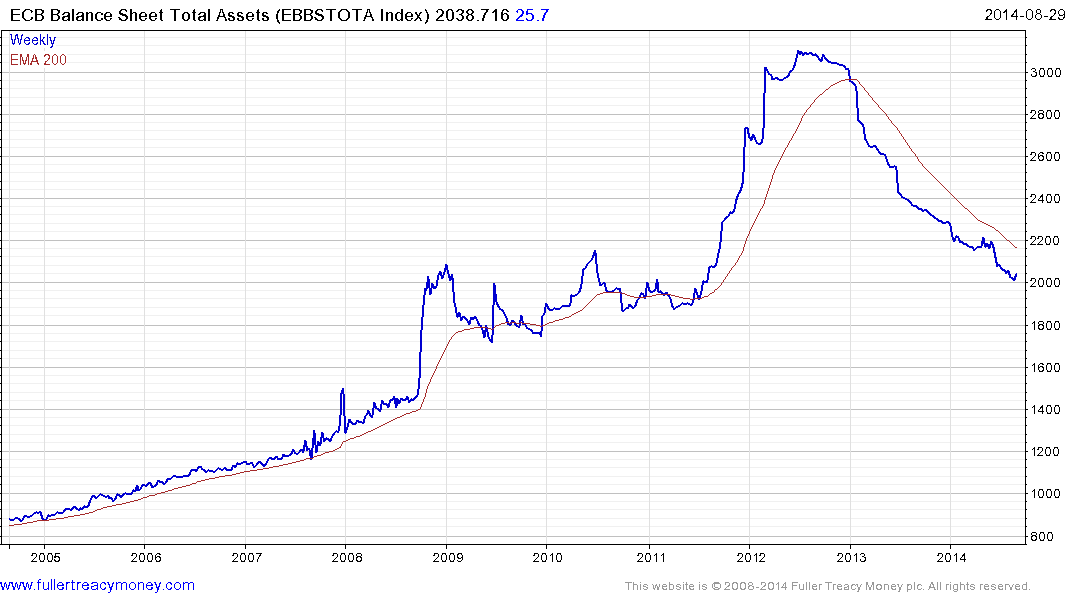

Pledging to “significantly steer” the European Central Bank’s balance sheet back toward the 2.7 trillion euros of early 2012 from 2 trillion euros now, the ECB president today announced a final round of interest-rate cuts and a plan to buy privately owned securities. His mission: to revive inflation in the 18-nation euro area.

Fully-fledged quantitative easing as deployed in the U.S. and Japan wasn’t enacted amid a split on the 24-member Governing Council, with Bundesbank President Jens Weidmann opposing the new stimulus and others seeking more. The latest round of measures pushed the euro below $1.30 for the first time since July 2013 and sent European bond yields negative.

The steps “probably reflect that President Draghi does not have unanimity, or a large enough majority for quantitative easing,” said Andrew Bosomworth, a Munich-based portfolio manager at Pacific Investment Management Co. and a former ECB economist. “The ECB is ready to do more if more is needed.”

The ECB announced a number of months ago that in addition to implementing a negative deposit rate, it would also seek to reverse the contraction of its balance sheet, explore asset backed security purchases and potentially adopt a fully-fledged quantitative easing program. The timing might not have been ideal at the beginning of the summer but with the Fed’s QE winding down, the ECB now has little choice but to pick up the slack if it is to maintain the access to liquidity on which the Eurozone’s banking sector relies.

The ECB Balance Sheet contracted from more than €3 trillion to €2 trillion from mid-2012 which contributed to the deflationary pressures experienced by the domestic economy. The announcement of a reversal of this policy should act as a tailwind for nominal asset prices although the Euro is likely to suffer.

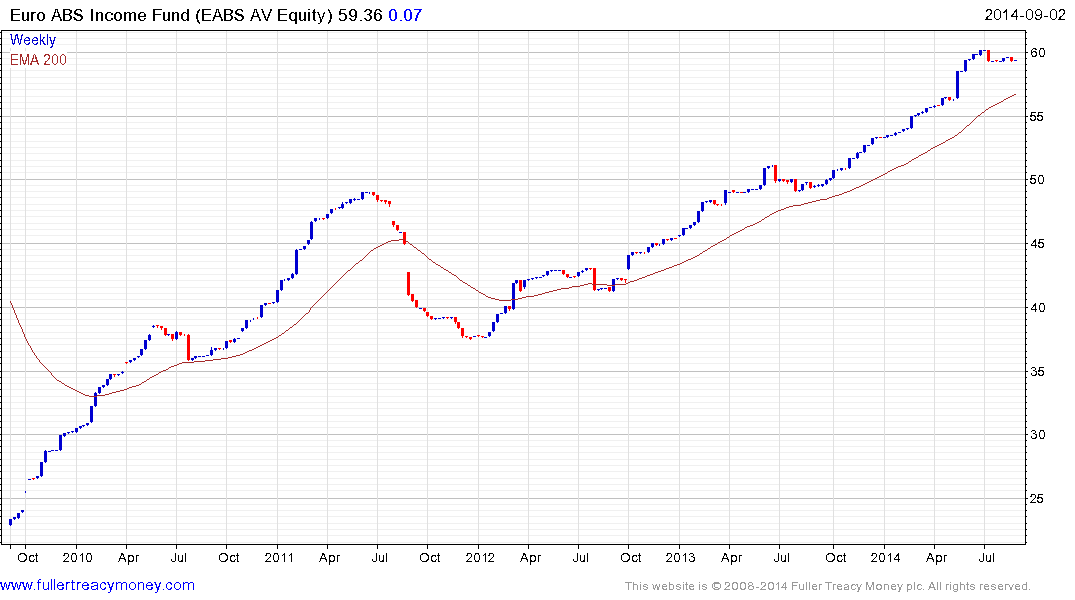

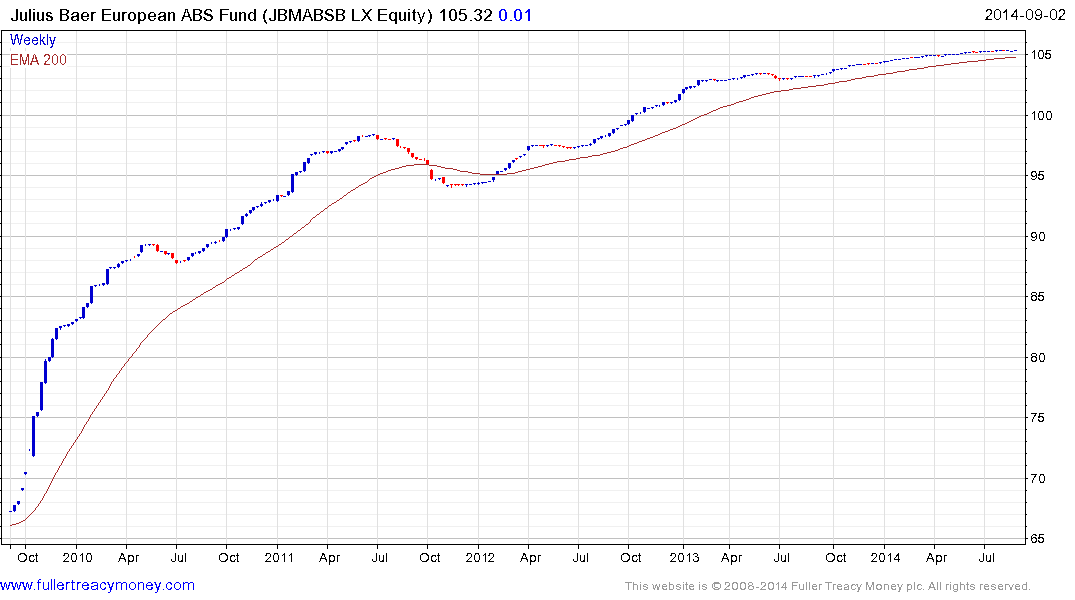

The announcement of a concerted policy to purchase asset backed securities (ABS) is a welcome development for the financial sector and those seeking credit to purchase homes and cars or to make credit card purchases. This policy is similar to that followed by the Fed in its support of Fannie Mae and Freddie Mac debt. It also signals that the illiquidity of the Euro ABS market will improve and that the central bank is willing to support the market.

The UK listed PFS Asset Backed Income Fund has an indicated yield of 7% and continues to hold a progression of higher reaction lows.

The Austria listed Euro ABS Income Fund invests at least 75% of assets in Euro ABS, yields 1.38% and has been cutting its dividend. The fund continues to hold a steady progression of higher reaction lows.

The Luxembourg listed Julius Baer European ABS Fund continues to hold a progression of higher reaction lows.

Here is a link to three additional Euro ABS related articles posted since April.

Back to top