Draghi QE Plan Seen Challenged by Hoarders Amassing Bonds

This article by David Goodman for Bloomberg may be of interest to subscribers. Here is a section:

Reduced government spending is likewise contributing to a global dearth of sovereign debt. Germany is due to curb the amount of conventional bonds outstanding by 8 billion euros this year. In Spain, where Prime Minister Mariano Rajoy’s People’s Party has implemented the deepest austerity measures in the nation’s democratic history, the net issuance target for 2015 is 55 billion euros, down from net sales of 97 billion euros in 2012.

Including ECB buying, net issuance of euro-area sovereign bonds will decrease by 259 billion euros in 2015, Morgan Stanley strategists, including London-based Neil McLeish, Anthony O’Brien and Serena Tang, forecast in a Feb. 9 note. The ECB may struggle to find sellers, leaving its target in jeopardy, the U.S. bank’s Maggie Chidothe and Anton Heese wrote in a Feb. 13 report.

Draghi’s competition for purchases may come from banks requiring bonds to meet regulatory rules, pension funds who need to match their liabilities, passive investors who track debt indexes and other central banks, which buy European securities as part of their balance-sheet management.

Quantitative easing programs around the world have taught us a number of lessons. The first and perhaps most important is that there is no limit to what a central bank can do to the monetary base provided they are willing to act. Naysayers have repeatedly been proved wrong since the advent of QE. The second is that as a result of extraordinary monetary intervention it is possible for government bonds and equities to rally in tandem. The third is that while we can debate the economic benefit of QE, there is no questioning that it successfully inflates asset prices.

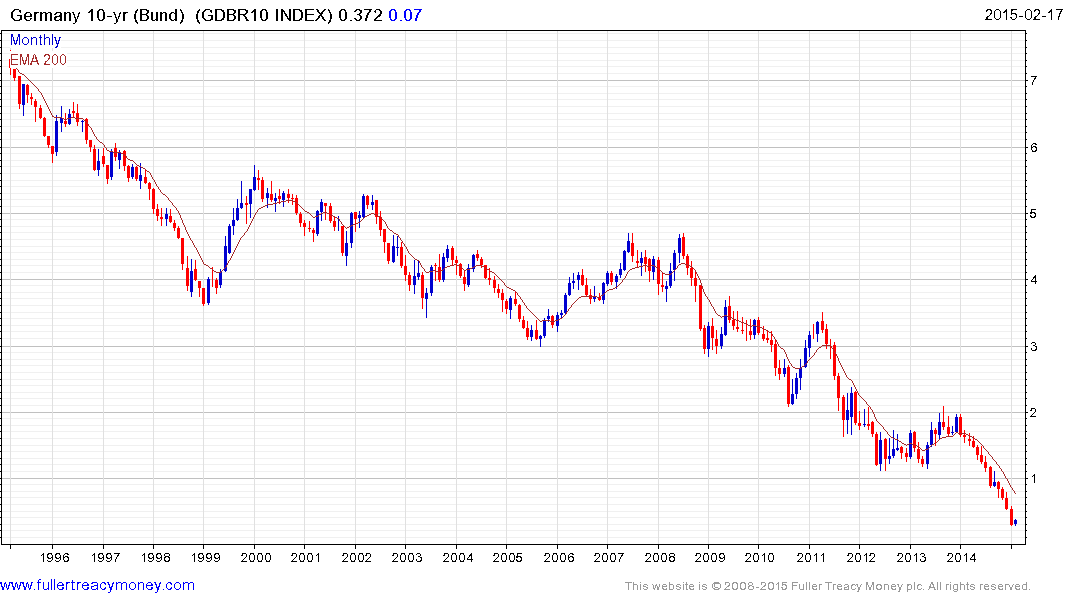

At the present time the German 10-year Bund yields 0.37%, the DAX total return index yields 2.51% and the Euro Stoxx 3.08%.

Momentum has already driven a number of core Eurozone countries’ debt to negative yields, particularly at shorter maturities. German Bund yields have stabilised above 0.3% and potential for a reversionary move has increased. However a sequence of higher reaction lows would be required to signal a return to supply dominance beyond the short term.

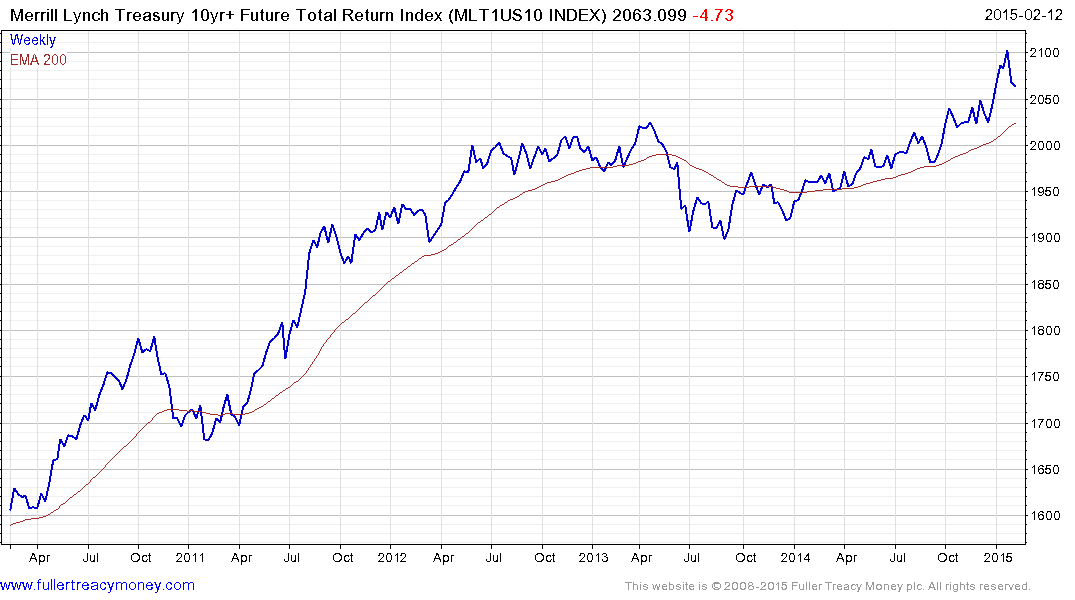

Total Return Bond indices for the USA, UK and Switzerland have already begun to unwind overextensions relative to the 200-day MA while Germany remains an outlier at least for the moment.

Investors might be unwilling to sell their holdings of longer dated issues because the repurchase risk is too great and momentum has flattered performance. However this does not affect maturity risk in shorter dated issues. For those hungry for yield the European stock market represents the same conditions today that Wall Street did in 2010. Once committed to its program, there is no limit to the price the ECB will pay for bonds. This has the potential to foment additional momentum but the relative attraction of equities with reliable dividends will only improve.

I will review the constituents of the S&P Europe 350 Dividend Aristocrats tomorrow.

Back to top