Draghi Big Push Seen Delivering $640 Billion With QE

This article by Alessandro Speciale and Andre Tartar for Bloomberg may be of interest to subscribers. Here is a section:

Mario Draghi is likely to announce a 550 billion-euro ($640 billion) bond-purchase program this week and won’t skimp too much on the details, economists say.

The European Central Bank president will make his biggest push yet to steer the euro area away from deflation by announcing quantitative easing on Jan. 22, according to 93 percent of respondents in a Bloomberg News survey. The median estimate of the size of the package tops the 500 billion euros in models presented to officials this month.

Draghi’s goal at a press conference after the Governing Council gathers will be to convince investors he has a strategy big and bold enough to reinvigorate the moribund economy.

Speculation over his plans has already sent the euro to an 11- year low, with the fund flows probably contributing to the Swiss National Bank’s shock decision to end a cap on the franc.

“Market expectations now are stellar,” said Attilio Bertini, head of research at Credito Valtellinese SC in Sondrio, Italy. There must be “no disappointment” and “the ECB’s next move should be pervasive, risk-transferring and long-lasting,” he said.The proportion of economists predicting QE at this week’s meeting has risen from 37 percent in a survey carried out after the last monetary-policy meeting on Dec. 4. This month’s survey polled 60 economists and was conducted from Jan. 9 to Jan. 16.

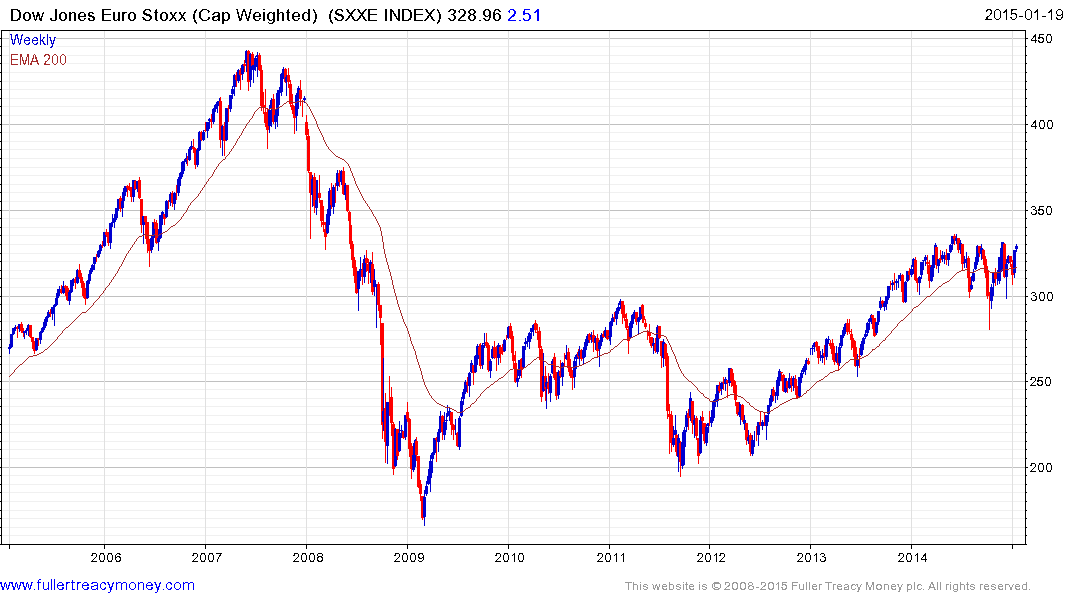

It’s been a long time coming but the prospects of a full blown quantitative easing program for the Eurozone have improved considerably in the last few weeks following the ECJ’s decision on the legality of the 2012 LTRO program, brinksmanship by Greek politicians and continued deflationary and disinflationary pressures. The equity market is already pricing in a significant move and the announcement will need to be in the region of the €600 billion mark if the recent run-up in Eurozone equities is to be sustained.

The Euro Stoxx Index has rallied over the last week to test the upper side of its six-month range as optimism about the impact on asset prices of quantitative easing overwhelms negative perceptions of the Eurozone’s growth potential. In the absence of a clear downward dynamic, potential for additional upside can be given the benefit of the doubt. I clicked through the constituents of the Euro Stoxx Index for clues to commonality among its outperformers.

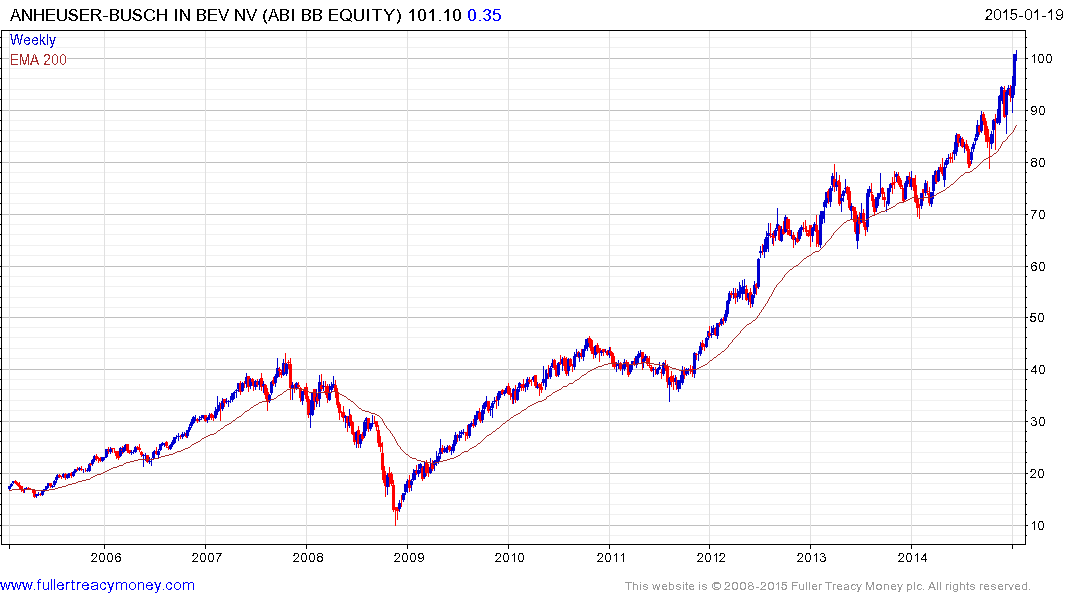

Exporters such as Anheuser-Busch Inbev have been leading the way higher but are becoming increasingly overextended.

Some clear commonality is appearing across a number of sectors.

In the insurance sector Allianz (Est P/E 10.19, DY 3.73%) has broken up out of a six-month range to reassert medium-term demand dominance.

Elsewhere AXA (Est P/E 9.52, DY 4.04%) exhibits a rounding characteristic consistent with accumulation.

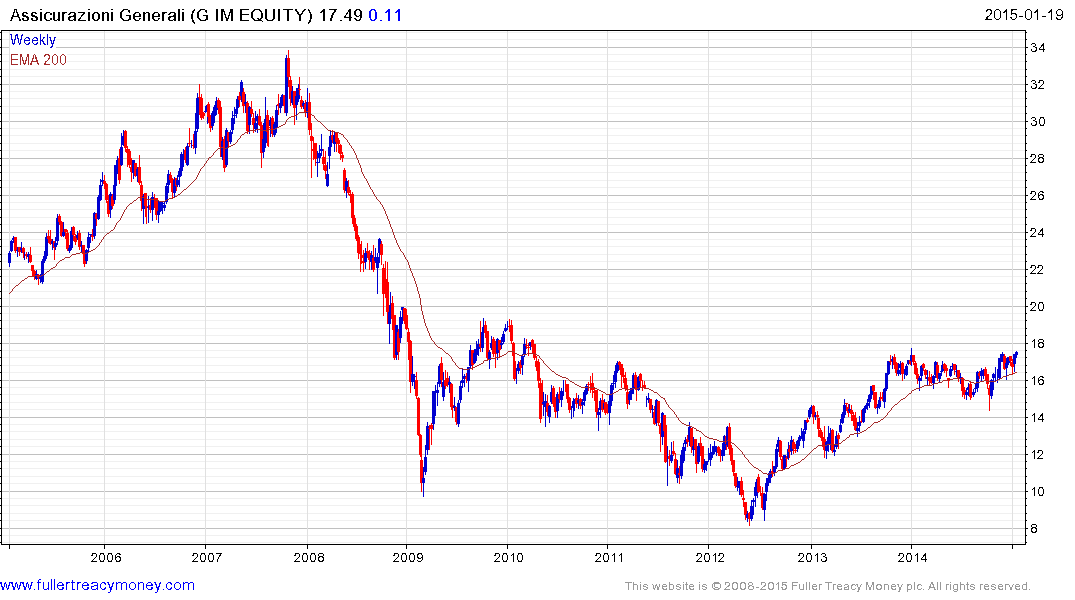

Italy’s Assicurazioni Generali (Est P/E 13.15, DY 2.57%) has a similar pattern.

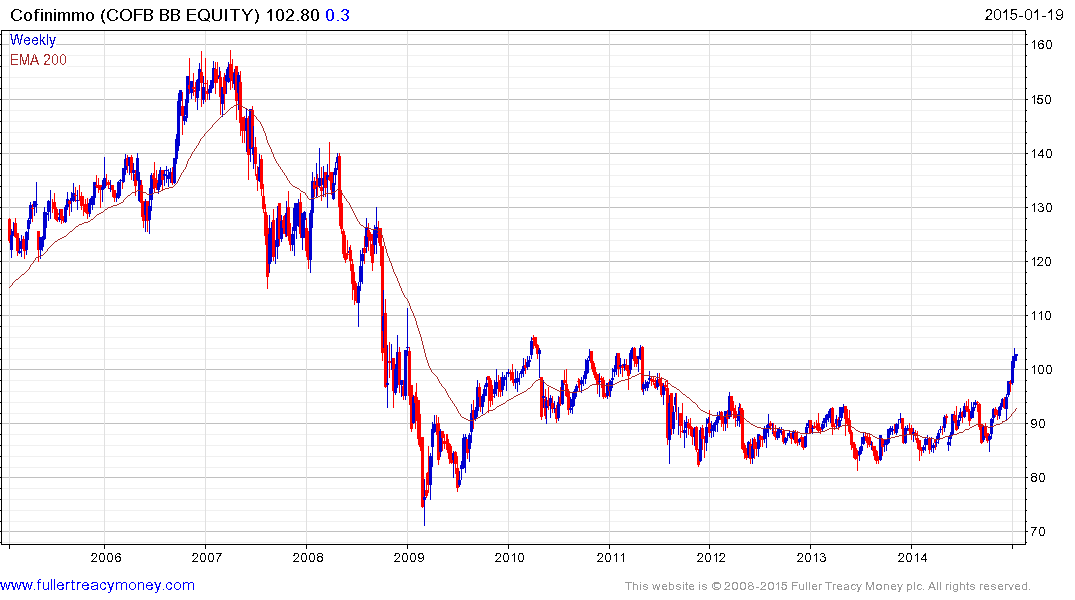

Among REITs Belgian listed Cofinimmo (Est P/E 15.99, DY 5.35%) broke out of a three-year base in the last month.

France listed Gecina (Est P/E 21.22, DY 4.2%) remains in a reasonably consistent uptrend.

France listed Klepierre (Est P/E 19.26, DY 2.32%) shares a similar pattern.

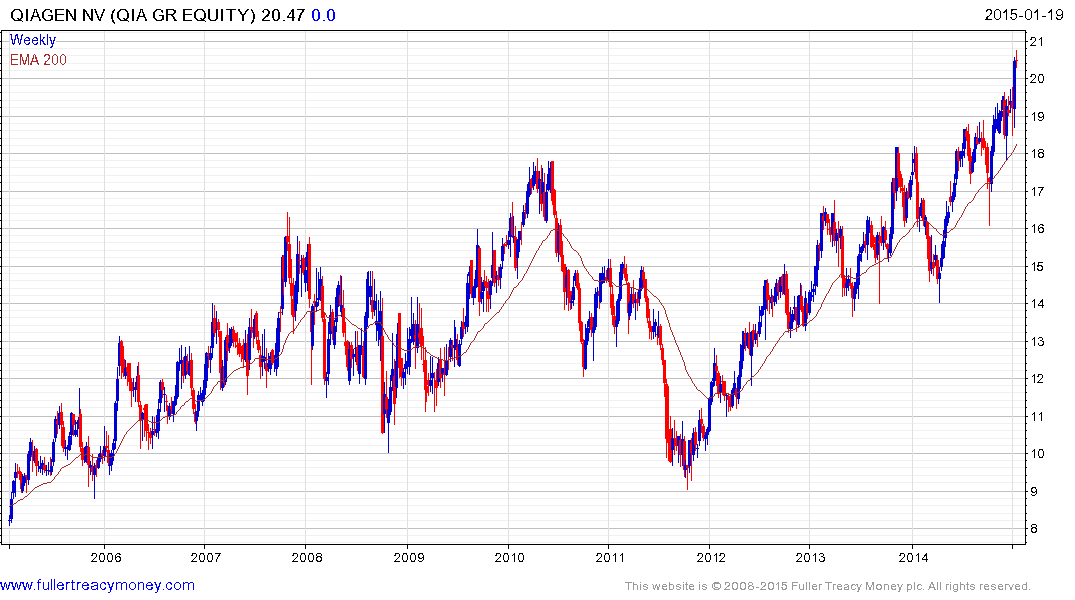

In the high tech health sector German listed Qiagen (Est P/E 22.5, DY N/A) is in the process of completing a more than decade long base.

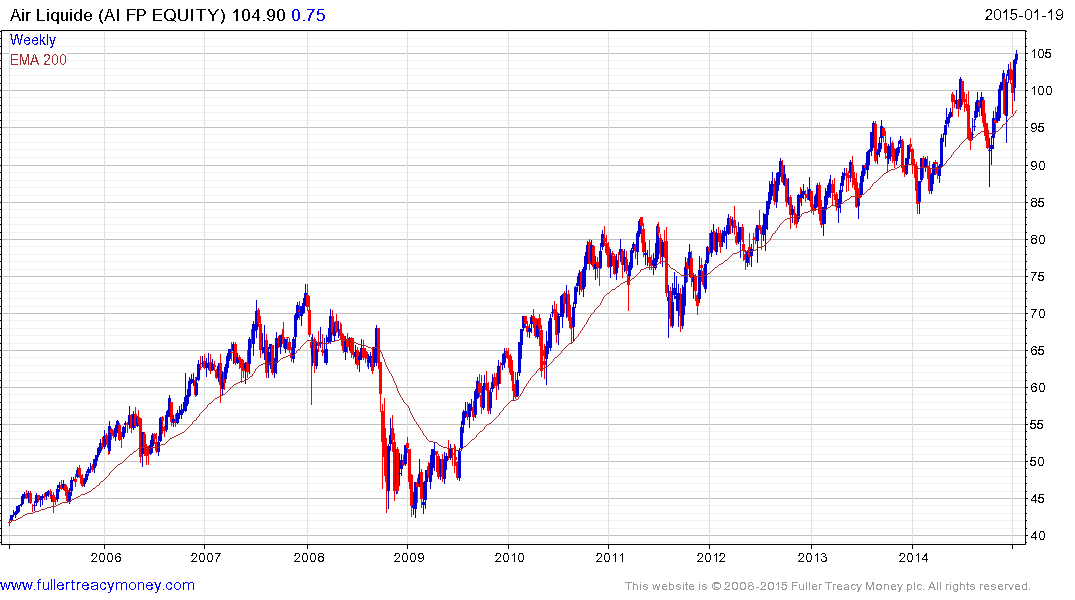

In the industrial gases sector both Linde (Est P/E 21.54, DY 1.87%) and Air Liquide (Est P/E 21.75, DY 2.21%) have broken up out of their respective more than yearlong ranges.

In the consumer sector the weak euro has flattered the performance of Unilever’s (Est P/E 21.71, DY 3.23%) Dutch listing which broke out of an 18-month range last week.

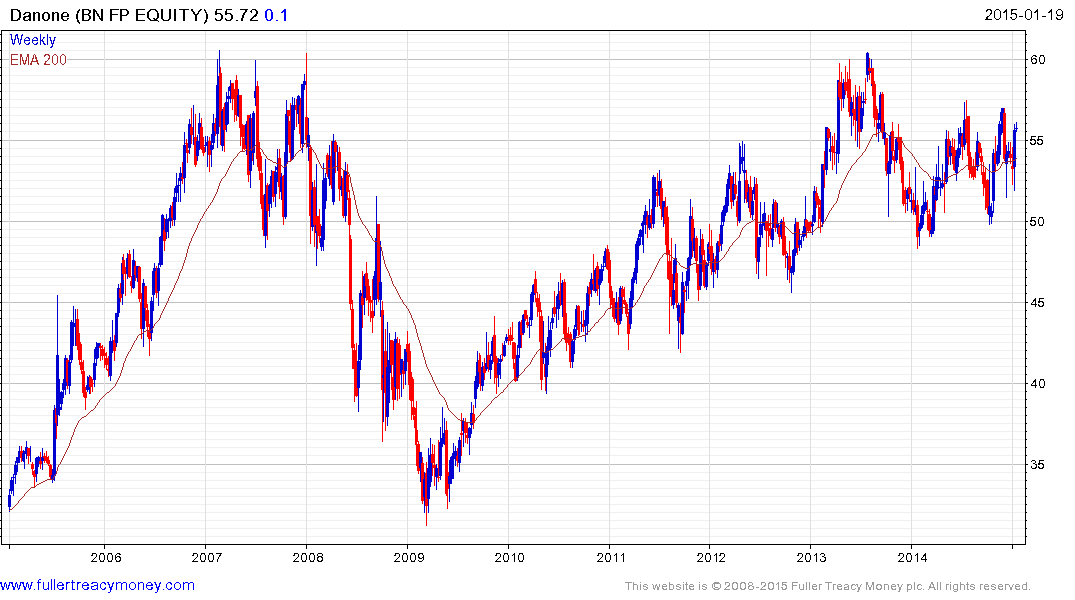

France listed Danone (Est P/E 21.2, DY 2.6%) has been ranging higher in a volatile manner for a number of years and is currently firming from the region of the trend mean.

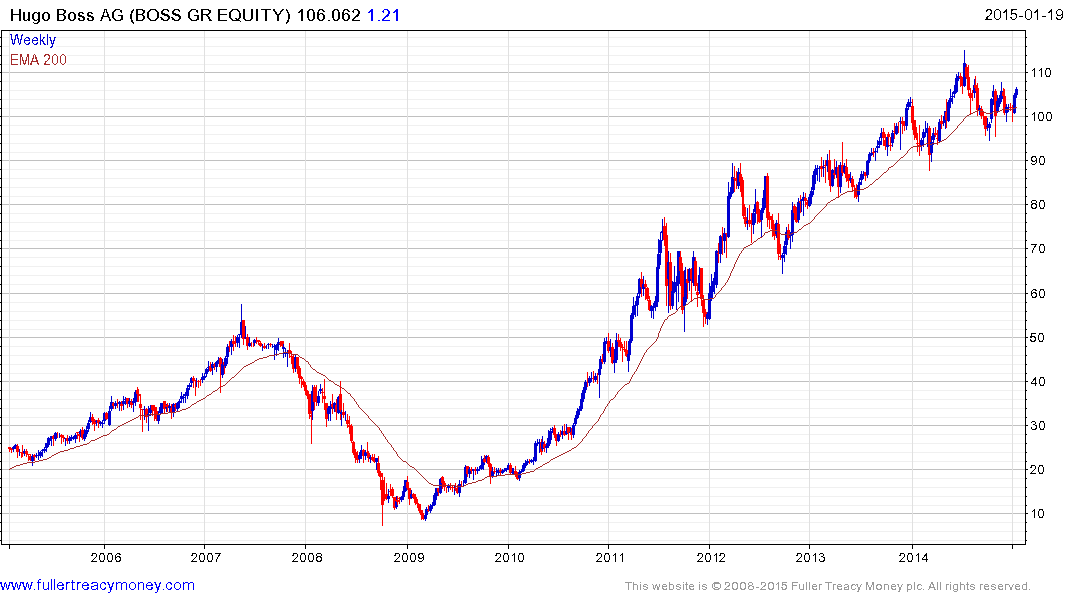

German listed Hugo Boss (Est P/E 20.34, DY 3.15%) is bouncing from the region of the 200-day MA.

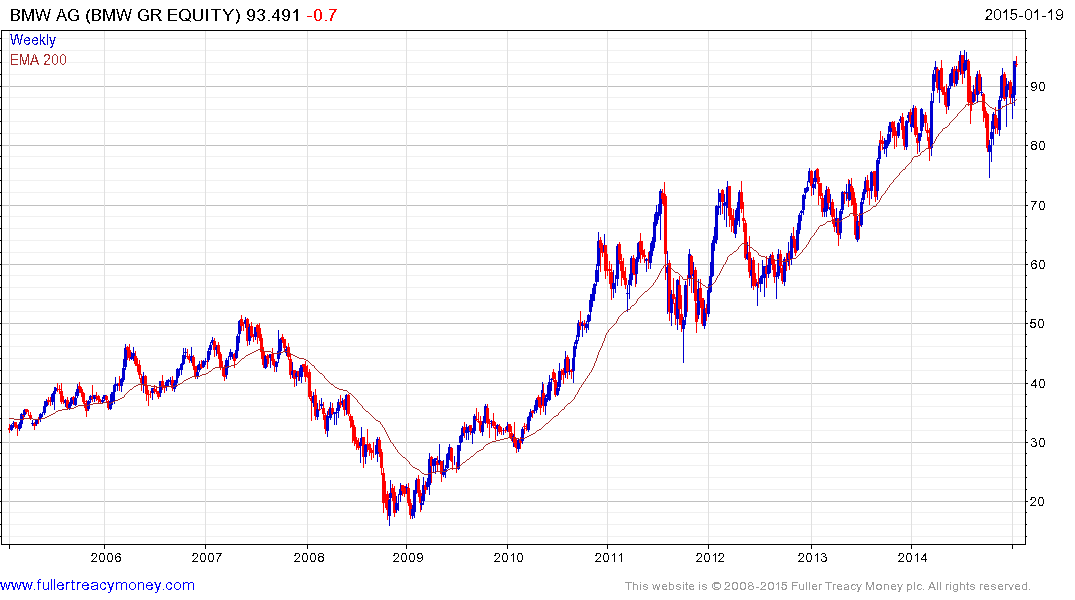

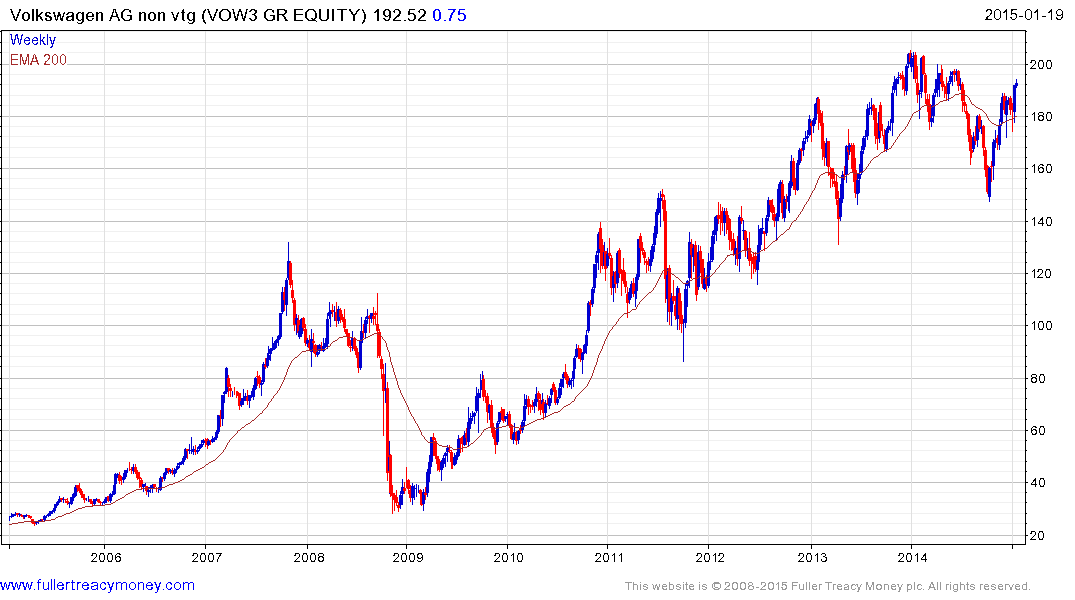

In the automotive sector Daimler (Est P/E 11.62, DY 3.2%), BMW (Est P/E 10.38, DY 2.77%) and Volkswagen (Est P/E 8.69, DY 2.11%) have all firmed impressively over the last week.

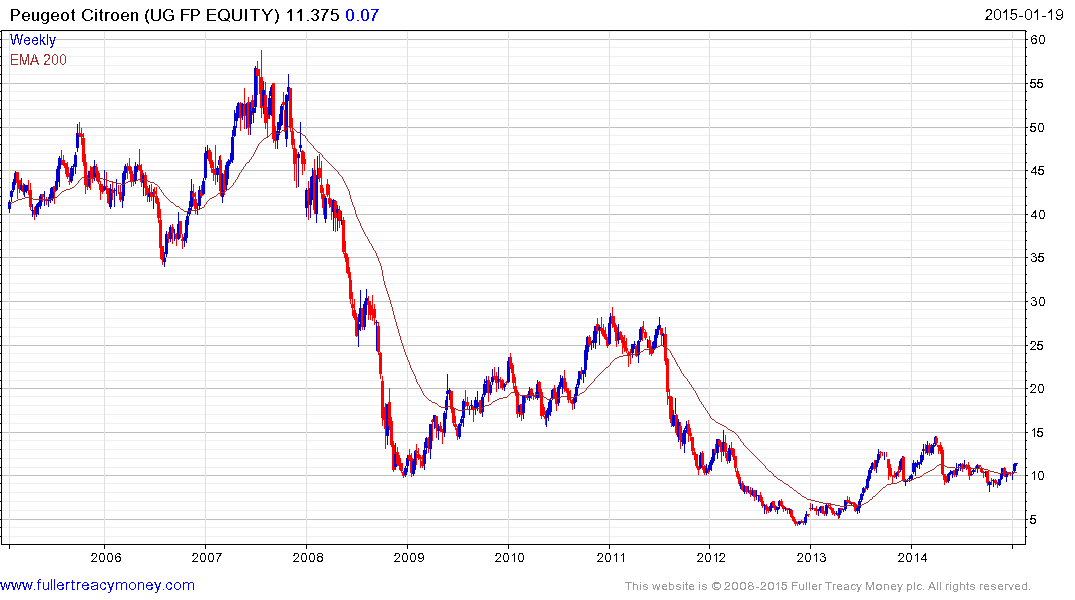

France listed Peugeot does not have the valuations of other auto companies to rely on but the share is firming within what has been a lengthy range.

In the supermarket sector France listed Carrefour (Est P/E 17.69, DY 2.28%) rallied last week to break a yearlong progression of lower rally highs.

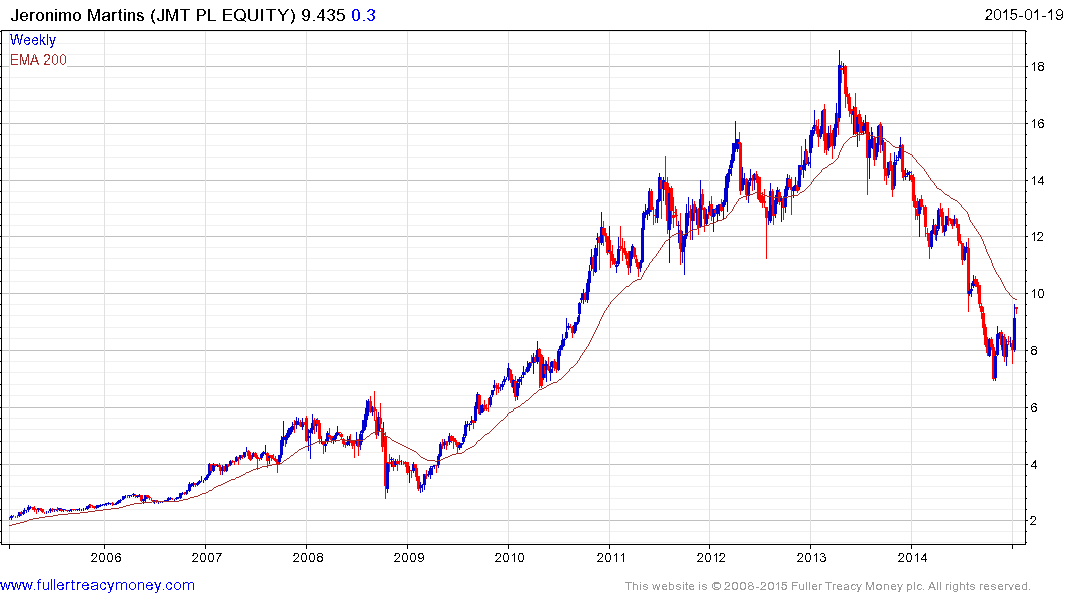

Portugal listed Jeronimo Martins (Est P/E 18.04, DY 3.23%) rallied last week to break an almost two-year progression of lower rally highs.

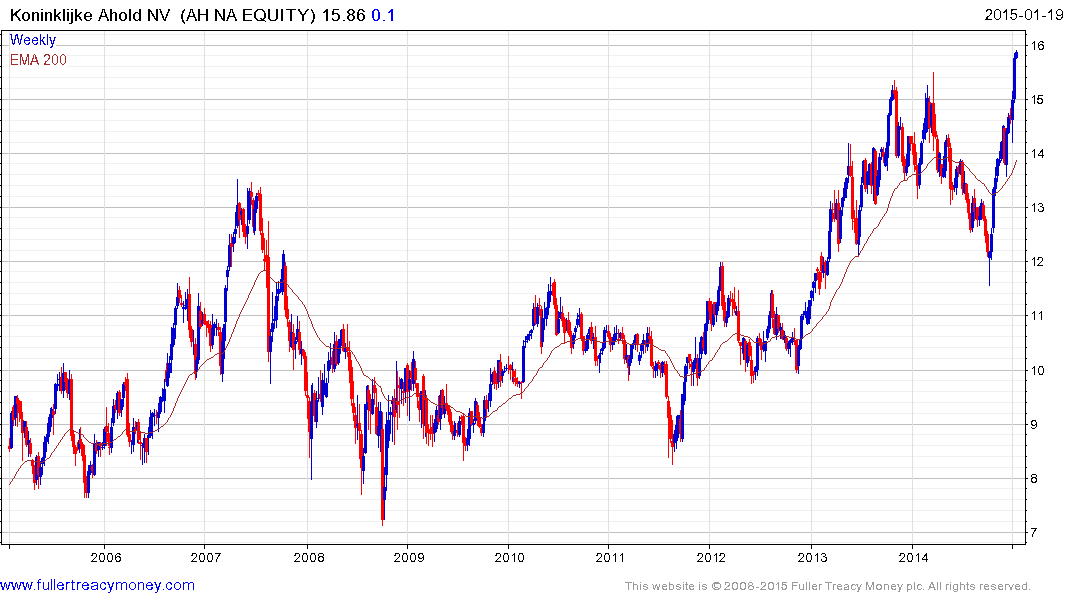

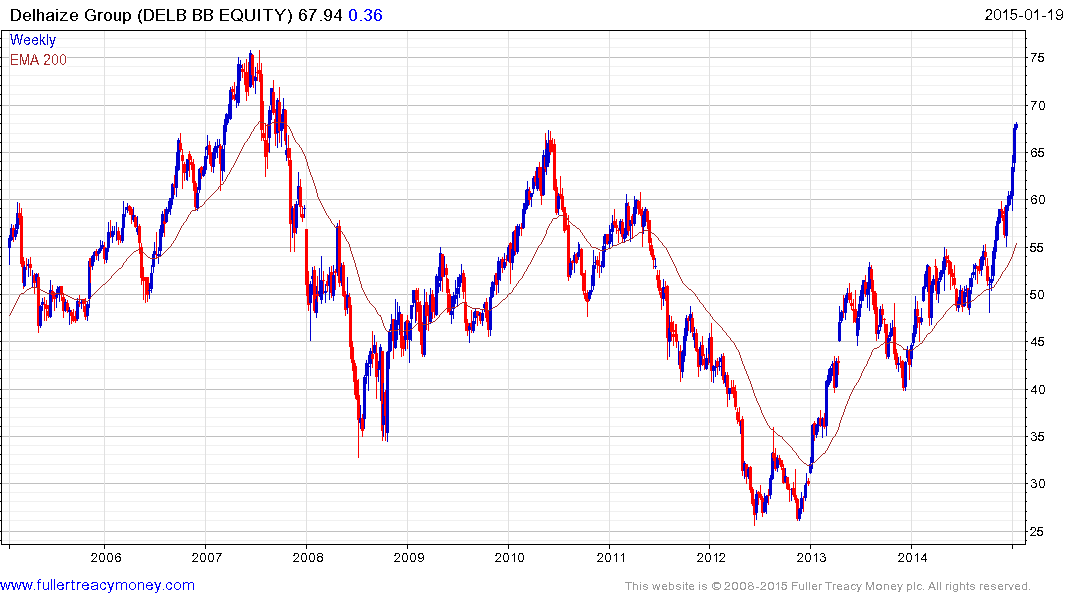

Dutch listed Ahold and Belgian listed Delhaize have been leading this group.

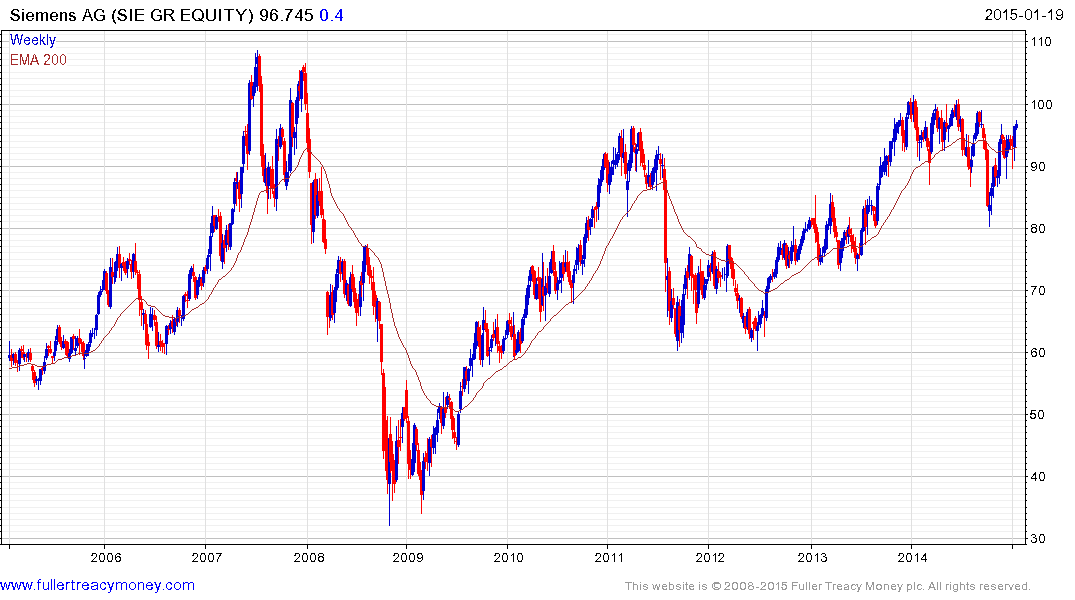

In the industrial sector Siemens (Est P/E 13.57, DY 3.42%) lost momentum a year ago in the region of the 2011 peak. The share has rebounded impressively from the October low and a sustained move below €90 would be required to question medium-term scope for additional upside.

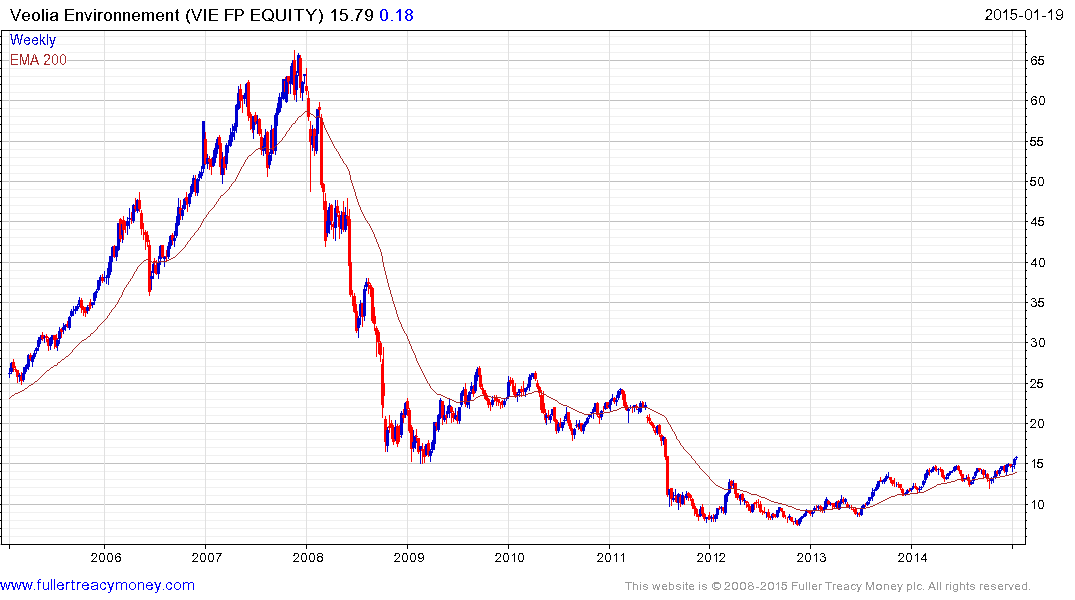

Also see last week’s mention of Veolia Environnement.

In the above review I have attempted to eschew the companies that are most overextended relative to their trend means but the general perception from clicking through all 294 members of the index is one of recovery.

Back to top