Don't lose sight of what you actually own

Thanks to a subscriber for this report from Canaccord Genuity focusing on Australia. Here is a section:

Here is a link to the full report and here is a section from it:

It is impossible to come up with a valuation-based approach on the market presently until we are able to determine the economic impact on company earnings estimates as social distancing mandates shut down economic activity, and unprecedented fiscal and monetary policies are changing by the day. We believe a test of the low is more likely than an uninterrupted move higher. Like other large market corrections, it is always difficult to pick the bottom, acknowledging that even the best investors rarely invest all their money at the bottom. We would look to add the higher quality names in the favourable sectors where the balance sheet is relatively resilient to weather the challenges and investors should look to take advantage of this opportunity presented in the market to move your portfolio up the quality chain. The focus should be on 1) protecting wealth, 2) minimising regret and then 3) capital growth.

Summary of Views by Asset Class Australian Equities Australia has done better than most other countries at controlling the outbreak of the coronavirus, by effectively implementing border controls, and social distancing measures to prevent community transmission. This ability to effectively control the virus in its initial stages indicates that Australia is well equipped to handle any future developments and may be in a better position than other countries to recover from this economic crisis. While the federal government has offered a significant stimulus package to alleviate the strain on the domestic consumer and employment market, there remains a very high probability that Australia will experience a recession for the first time in 30 years. This will have a significant impact on most companies’ earnings, with the likely result being a reduction in dividends or even deferrals as companies seek to preserve cash. In addition, while we have already seen a number of heavily discounted capital raisings, we expect further to come as companies seek to bolster their balance sheets in an environment of reduced revenue.

It is probably true that Australia is about to have a technical recession. The fires, lockdowns and collapse in Chinese demand are all contributing factors. However, it is also worth remembering that the medium-term response to the coronavirus is likely to be an epic infrastructure development spending spree which will be global in nature. For commodity exporters like Australia that is likely to be good news.

The healthcare and technology sectors have led the Australian market higher over the last few years as the banking and resources sectors have fallen out of the limelight. Together the health and IT sectors represent 17.05% of the S&P/ASX 200 while the financials and materials sectors occulting 44%.

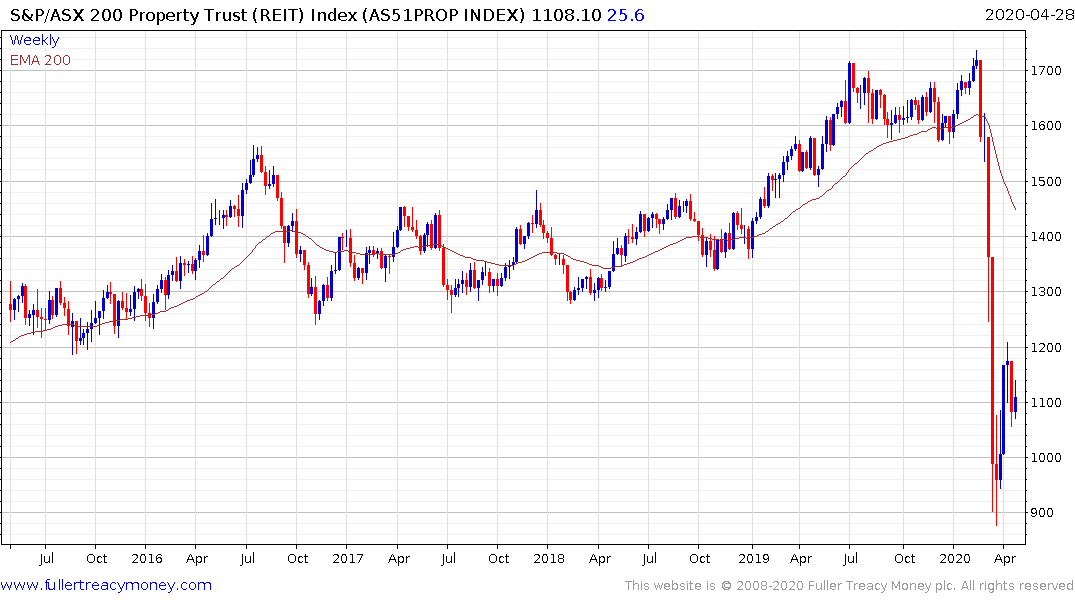

Energy, Finance and Real Estate have led the decline and with the property sector representing the greatest risk to growth. How well the rest of the world returns to a growth footing will have a large bearing on how quickly emerges to a growth position once more.

The ability of the resources sector to hold its lows during any period of consolidation is likely to be a good barometer of that outcome is being weighed by the market.