Dollar Soars After Jobs Surprise Reignites Higher Rates Bets

This article from Bloomberg may be of interest. Here is a section:

A broad gauge of dollar strength jumped after the jobless rate in the US hit a 53-year low as traders amped up bets on a higher policy rate.

The Bloomberg Dollar Spot Index extended gains for its biggest two-day climb in four months after data highlighted the resilience of the labor market and another report showed resurgence in consumer demand, suggesting even more tightening may be in store from the Federal Reserve.

The greenback gained as much as 1.2%, climbing against all of its peers in the Group of 10, with the Japanese yen, the Australian dollar and New Zealand dollar falling the most.

“The headline number for nonfarms was shocking, and the US dollar is clearly reacting to that,” said Bipan Rai, a currency strategist at Canadian Imperial Bank of Commerce. “We still have plenty of data to comb through before the picture is complete.”

The simple logic is you cannot have a recession without unemployment rising. That suggests the Federal Reserve is under no pressure to cut rates and may even continue to raise them. That lent considerable support to the Dollar Index and it is working on a large upside weekly key reversal which marks a lot of at least near-term significance.

Gold extended yesterday’s downside key day reversal to confirm at least a near-term peak and onset of at least some consolidation of the short-term overbought condition.

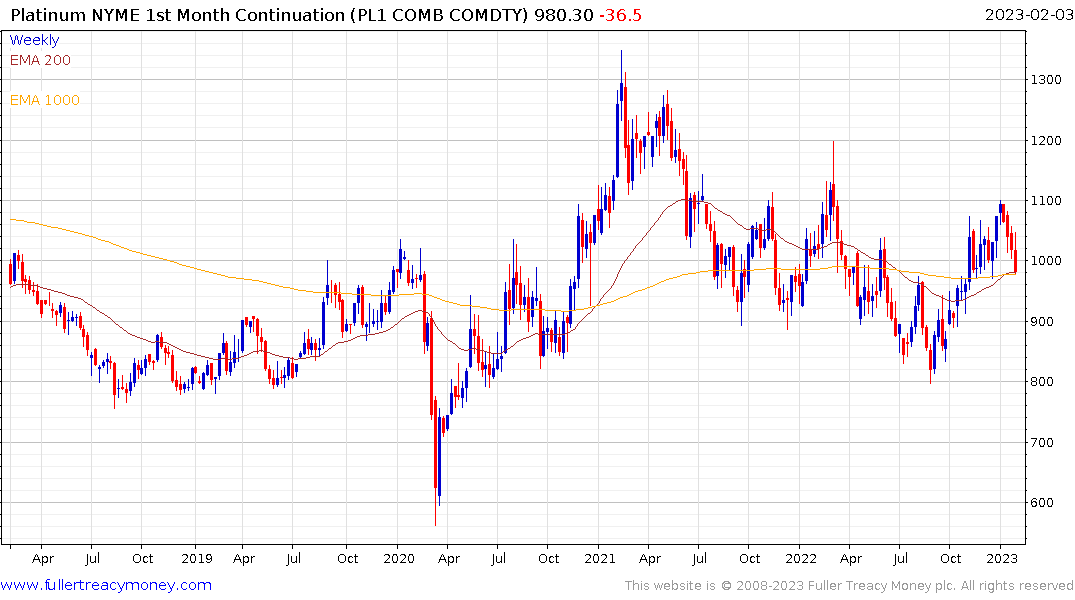

Platinum reversed yesterday’s strength to drop back below the psychological $1000 level.

Silver has also posted a large weekly downside key reversal to confirm the medium-term sequence of lower rally highs. A clear countermanding upward dynamic will be required to check momentum.

This report from Horizon Kinetics includes some useful estimates for how much interest expense will figure into future US budgets. Here is a section:

In this scenario, based simply on the repricing of the next 3 years’ debt maturities, the U.S. government must pay an extra $450 billion in annual interest expense. This does not include the possibility of: higher interest rates; any recession impact; or emergency spending impacts, as for disaster aid or war. (One might note, as to how official budget projections work, that annual weather disaster relief costs are now in the $200 billion per year range8, which far exceeds annual appropriations and supplemental appropriations of about $65 billion9. The appropriations are based in part on 5-and 10-year historical average costs. Yes, in the 2000s, annual disaster relief costs did average, $60 billion, though they approached $100 billion in the 2010s.)

The additional interest expense could easily be $1 trillion. Whatever the figure, $450 billion can reasonably be considered a lower bound. The government must find some way to raise that revenue each year or reduce annual spending by that amount. That incremental interest expense is about exactly one-third the size of last year’s budget deficit. It would be extremely difficult to accomplish even a half-trillion dollars’ worth of increased tax revenue or reduced spending. Is it even practically possible?

The only way it can come close to being practically possible, is to keep rates high enough for long enough to kill off inflation. If that increases the interest expense of rolling over government debt in the short so be it. The alternative would be to accept chronic budget constraints indefinitely. More than any other factor, that is the primary reason the Fed needs to get in control of inflation now. Little wonder they are praying for a soft landing.

Back to top