Dollar Advances for a Third Day Versus Euro Before Fed Minutes

This article by Marianna Aragao for Bloomberg may be of interest to subscribers. Here is a section:

The dollar climbed for a third day versus the euro before the release of minutes of the Federal Reserve’s latest policy meeting that may provide clues on the path of U.S. interest rates.

The greenback reached its strongest level since July versus Europe’s shared currency as traders awaited the record of the Federal Open Market Committee’s September meeting for signs that Chair Janet Yellen will raise borrowing costs soon. The odds of a rate increase by year-end have climbed to 68 percent, from 60 percent a month ago, amid speculation a recent surge in oil prices will fuel inflation. A gauge of the dollar held near a two-and-a-half month high.

“The dollar has already received support over the recent days on comments” from Fed officials, and “the market now wants to look if the minutes are in the same direction,” said Georgette Boele, a currency and commodity strategist at ABN Amro Bank NV in Amsterdam. “If the minutes confirm it, the dollar could get a bit more support.”

The dollar appreciated 0.3 percent to $1.1025 per euro as of 7:22 a.m. New York time, having touched $1.1010, the strongest since July 27. Bloomberg’s Dollar Spot Index, which tracks the currency against 10 major peers, was little changed, after rising Tuesday to the highest level since July.

The Fed is flirting with raising interest rates again, having already done so once. While absolute levels are still very low that represents a sharp distinction from just about all other major central banks that are still in easing mode.

The experiment with negative interest rates in the EU and Japan has helped support their respective currencies. However there is increasing acceptance that it is counterproductive to the aim of the achieving inflation and also represents an existential threat to their respective banking sectors.

The ECB caused some debate two weeks ago when some officials hypothesised that tapering might be a good idea but realistically the Eurozone economy is a long way from being able to sustain an expansion without significant support. The same can be said for the Japanese economy. The result is that it is hard to imagine why these currencies should be strengthening against the Dollar when the prospect for a widening interest rate differential is in its favour.

The Dollar Index has now broken a progression of lower rally highs, evident since late last year. A clear downward dynamic will be required to question potential for additional higher to lateral ranging and a possible retest of the psychological 100 level.

The Dollar is now testing its downtrend against the Yen and a move above ¥105 would break the medium-term progression of lower rally highs.

The Euro is retesting the $1.10 area which represents the progression of higher reaction lows since late last year.

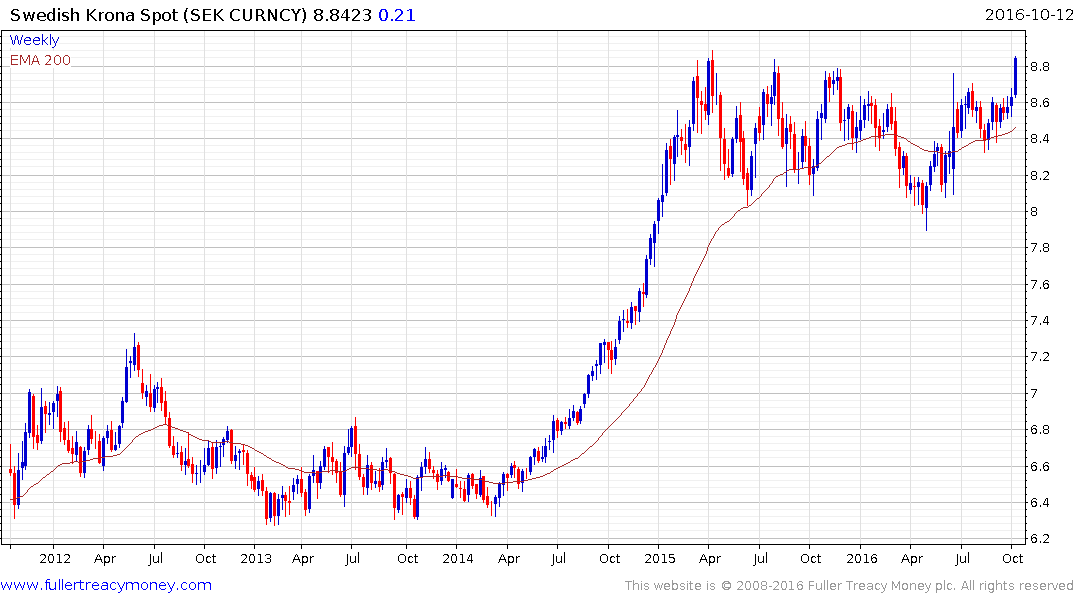

While the Pound has steadied following last week’s flash crash there is still a great deal of uncertainty surrounding the outcome of negotiations with the EU so it is likely to represent a continued tailwind for the Dollar Index. Meanwhile the Dollar rallied impressively today to test the upper side of the almost two-year range against the Swedish Krona.