Dogmas of the Quiet Past, Why Higher Rates are on the Horizon

Thanks to a subscriber for this article by Pamela Rosenau which appeared in Forbes. Here is a section:

For starters, history tells us that the dynamics of the supply and demand for money are relevant for determining an appropriate level for interest rates. The Federal Reserve is decreasing the supply of money by tapering their balance sheet, while the demand for money will increase with the latest bout of expansionary fiscal policy (i.e. tax reform). Professor Lars Oxelheim of the Financial Times, recently wrote how historical precedence has shown how this supply/demand shift can lead to significantly higher interest rates over a short period of time. Of course, this would impact the valuation of all asset classes as discount rates head higher. Market strategist Dave Rosenberg recently added that “we have a government policy that is aimed at pushing fiscal deficits higher and pulling trade deficits lower. Say this over and over again – these two goals can only co-exist with rising interest rates.”

Also, who is going to stroll in on their white horse and be the new big US treasury bond buyer? We know that the Fed is pruning their bond portfolio. After all, newly installed Fed Chairman Powell showed his true colors six years ago when he warned of the “Greenspan put” and its implicit encouragement of risk taking. Considering his concerns back then, I cannot imagine him being overly dovish given the valuation excesses in our environment today. Furthermore, the Chinese could play monetary hardball as a response to any hostile U.S. trade actions and choose to mitigate their participation in our auctions, thus causing a sudden spike or pernicious reset in interest rates. Frankly, Xi Jinping has a license to do whatever he wants at this point.

Let’s lay aside for a moment the arguments about whether inflation is in fact rising or not, or whether we can expect all of the deflationary forces that have contributed to the decades long decline of yields to continue. Let’s just devolve to the first principles of markets. There are more sellers than buyers.

The Fed is reducing the size of its balance sheet at exactly the same time the Treasury needs to both refinance legacy debt and print even more. That’s not a recipe for low yields.

Against that background we have to at least consider everything we know about crowd psychology and the nature of trends. Very simply, ranges are explosions waiting to happen. Treasury yields have been ranging below 3% for six years. When the breakout occurs the balance to probabilities is that it will be both surprising in its ferocity and persist for longer than many people believe possible. That is despite the short-term big under Treasuries we see right now because of the correction on Wall Street.

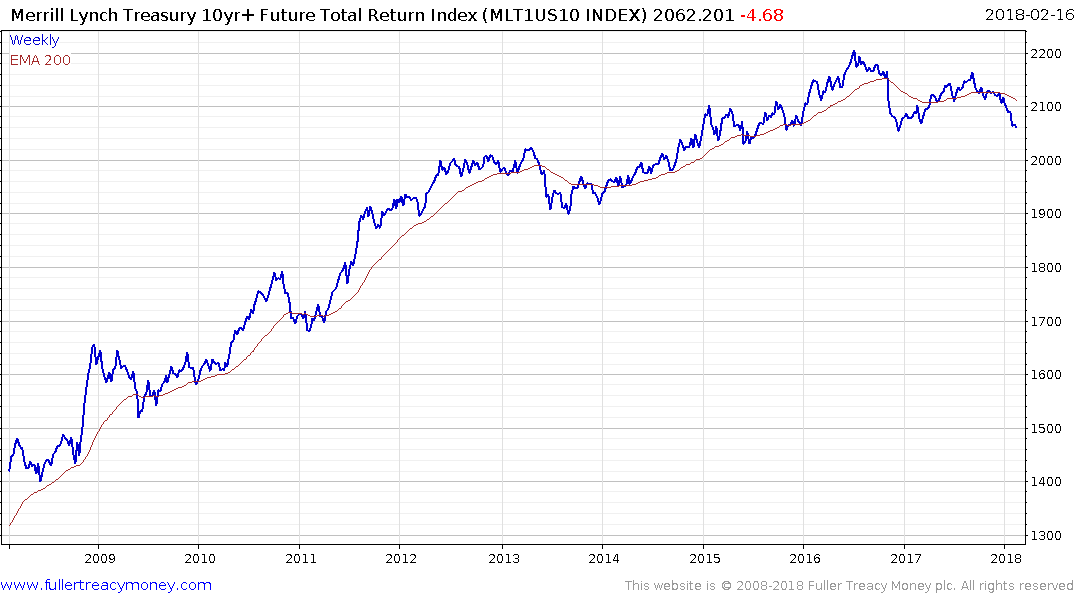

The Merrill Lynch 10-yr+ Treasury Futures Total Return Index has Type-3 top formation characteristics and a sustained move to 2050 would confirm the end of the 37-year bull market which has had an eerily similar lifespan to a Kondratieff cycle.