Denver Gold Forum Highlights Trends Reinforce Focus on 'Walk Before Run' Strategies

Thanks to a subscriber for this report from National Bank focusing on gold miners. Here is a section:

Exploration budgets getting a lift. With balance sheets in better shape from non-core asset sales, higher metal prices, and, in cases, financings, senior and junior companies alike are ramping up exploration budgets and project evaluation programs.

For the juniors and intermediates this could generate discoveries of a size that is material to production. Recent exploration and project examples include Newmarket Gold (Fosterville), OceanaGold (Macraes, Waihi, Haile), Richmont (Island Deep), Alamos (La Yaqui) and Alacer Gold (Gediktepe).

For seniors, exploration spending remains disproportionately focused on near-mine and Brownfield targets (Figure 2) as they look to add and upgrade ounces proximal to existing mine infrastructure. This focus also seems appropriate in the context of recent trends that show a declining discovery rate despite higher-than-average exploration Page 2 expenditures. For example, from 2006 to 2015 some US$54 bln was earmarked for discovery-oriented exploration budgets (69% of total spending from 1990 to 2015), yet gold in major discoveries dropped every year except in 2015. Refer to Figure 3. Thus, in our view, it is unlikely that the recent uptick in exploration spending will generate a different result, specifically new discoveries of a size that can thwart the outlook for production declines. Recognizing that the odds are stacked against them, we view as prudent senior company’s focus on near-mine and Brownfields exploration.

?Benign cost pressures bode well for continuing balance sheet improvements and FCF – conditions that appear to buoy the interest of generalist investors. With currency one of the principal drivers of cash cost trends and FX rates in key mining jurisdictions still generally weak vis-à-vis 2014 and 2015 levels, the backdrop remains constructive for lower costs year-on-year (Figure 4). With that, we expect operating margins to remain robust and be of a magnitude sufficient to maintain investor interest in gold equities. In fact, in speaking with several generalist investors, arguably, this was one of the main takeaway from the DGF.

Here is a link to the full report.

Mines are depleting assets by definition so management teams have to make tactical decisions about when to spend, what is often significant capital, on increasing their potential supply options. After a generational long bear market the gold mining sector had been unable to address their declining mine life problem so when gold prices began to pick up they poured every available cent into increasing supply. That resulted in their shares underperforming the gold price and represented a serious headwind for the sector when gold prices rolled over.

That bitter experience has informed the actions of gold miners since and they are now much more cautious about committing to expensive exploration and development projects, even though the issue of extending mine life remains a legitimate, albeit, medium-term concern. That focus on cashflow has allowed the gold mining sector regain its leverage to the gold price.

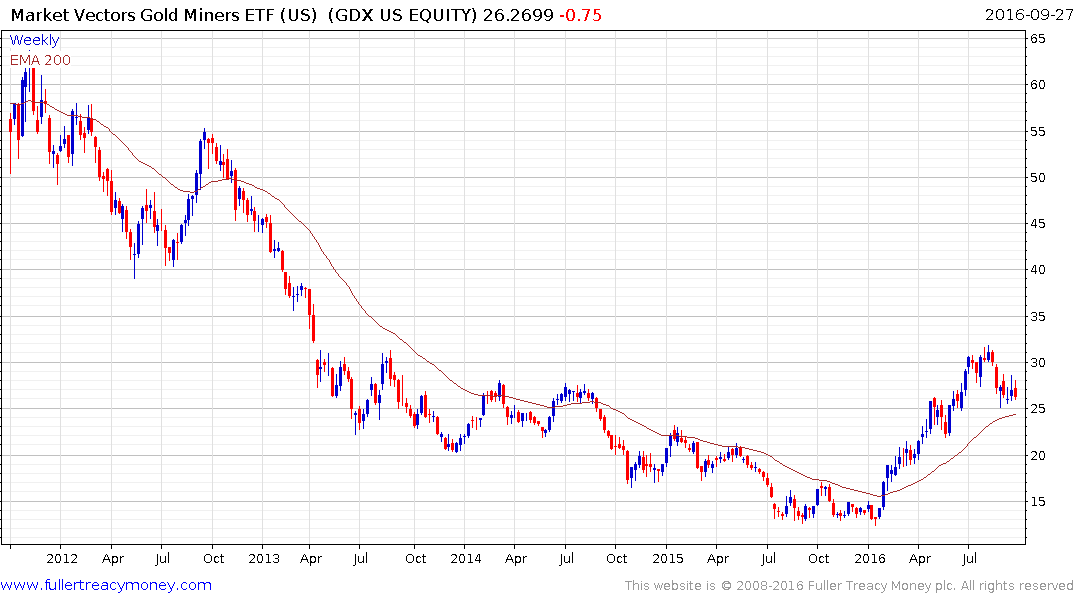

The VanEck vectors Gold Miners ETF (GDX) continues to trade in the region of the trend mean and will need to continue to find support in that area if medium-term recovery potential is to remain the base case.

The gold price continues to consolidate above the round $1300 area, However a short-term progression of lower rally highs is evident within the range and that will need to be broken to reassert demand dominance.