Deflation Stalking Many Nations as Oil Takes Toll

Thanks to a subscriber for this chart illustrated article by Mark Gilbert. Here is a section:

The euro region looks to be most at risk of sliding into deflation early next year. Consumer prices rose just 0.3 percent in November, a far cry from the European Central Bank’s 2 percent target. And the ECB’s preferred measure of where the collective intelligence of financial market participants says inflation is headed — the five-year rate on inflation swaps in five years’ time — heads lower all the time:

Deflation prospects are also evident in the world’s government bond markets. In the U.S. Treasury market, dealers have dissected the securities into so-called STRIPS– Separately Traded Interest and Principal Securities — at a pace that’s swollen the market to $211 billion, its biggest since 1999. Strips, which lose value quicker than just about anything else if inflation accelerates, have instead posted returns approaching 50 percent this year, Susanne Walker reported for Bloomberg News this week. U.S. bondholders are so relaxed about inflation that they’re almost horizontal.

And in Germany, investors are paying for the privilege of stashing their cash in government debt — another sign that they don’t expect inflation to erode the value of their returns:

Some countries are already in deflation. In Sweden, consumer prices dropped for a fourth consecutive month in November, prompting the central bank yesterday to commit to keeping its main interest rate at zero until the second half of 2016. Spain, which is at the mercy of the ECB’s policies, has seen deflation for the last five months, with prices dropping by 0.4 percent in November.

Even in the U.K., where the economic recovery is relatively robust, figures yesterday showed inflation at its slowest in more than a decade, with November consumer prices rising just 1 percent. That helped drive the yield on 30-year gilts to a record low on 16 December 2014:

There was some heated discussion in the period from 2009 about whether the USA would follow a similar trajectory to Japan and fall into deflation. Ben Bernanke’s introduction of extraordinary monetary measures avoided that outcome but the sclerosis that has gripped the Eurozone increases the possibility that it will experience a Japanese style deflation.

The difficulty of tailoring monetary policy to the vicissitudes of multiple governments and fiscal policies has been highlighted ad nauseam. Amid this discussion it is easy to forget that while the ECB has taken on additional responsibilities it only has one core mandate. That is to achieve an inflation target close to but not higher than 2%. It’s a long way from achieving that goal.

The end of the Fed’s QE has thrown responsibility for monetary easing back on the ECB since the flow of additional capital through swap lines with the Fed has decreased. Against that background, it appears to be only a matter of time before it adopts a form of quantitative easing.

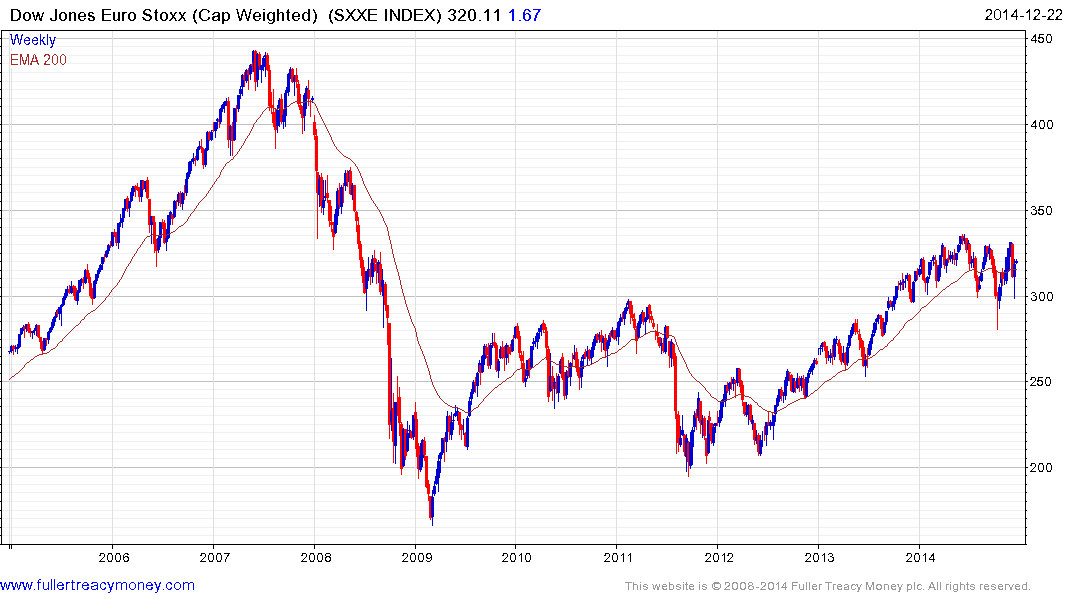

The Euro Stoxx Index should benefit from the introduction of extraordinary monetary policy. The Index has been ranging mostly above 300 for much of the last year and a sustained move below that level would be required to question medium-term potential for additional higher to lateral ranging.