Cracks in the market: Is New York's real estate boom over?

Thanks to a subscriber for this article by Daniel Geiger for CrainsNewYork which may be of interest. Here is a section:

Among the recent string of sobering reports is news that a 10-story building in Brooklyn Heights—one of three large properties being sold by the Jehovah’s Witnesses there and in Dumbo—will fetch a price 25% below the $300 million or more for which it was initially projected to sell. The parcels are considered prime places for both residential and commercial development.

Brokers said the decrease mirrors a precipitous drop in the value of land sites in the city by 20% to 25% so far in 2016. These brokers declined to speak on the record because several are marketing such properties and don’t want to openly disparage the products they are trying to sell.

Tumbling land values, which had reached $1,000 or more per square foot for prime sites, are a reflection of the growing weakness in the city’s high-end residential market. Developers had been willing to pay record sums for land as long as the apartments they built could fetch unprecedented sums. The payoff is no longer the same, according to the brokerage Corcoran Group, which reported that the average sale price for a luxury apartment fell from $8.1 million in the fourth quarter of 2014 to $6.9 million at the end of 2015, a 15% decline.

The rise of the dollar against currencies of countries whose citizens have been stashing their wealth in New York real estate has also hurt the market, according to a report released last week by the National Association of Realtors.

The number of articles crossing my desk of late discussing slowing demand for luxury property has grown considerably over the last few months. This article from the Wall Street Journal from January is another example. As we have mentioned previously, one of the primary effects of quantitative easing has been to inflate asset prices and this is as true of property as it is of stocks and bonds.

The Fed is very gradually attempting to normalise monetary policy while at the same time the ECB and BoJ are accelerating their purchase programs. As the central bank policy trajectories diverge I wonder will Eurozone property fare better than US and UK property over the next few years not least because asset prices are lower on average than the inflated prices currently on offer in the UK and USA.

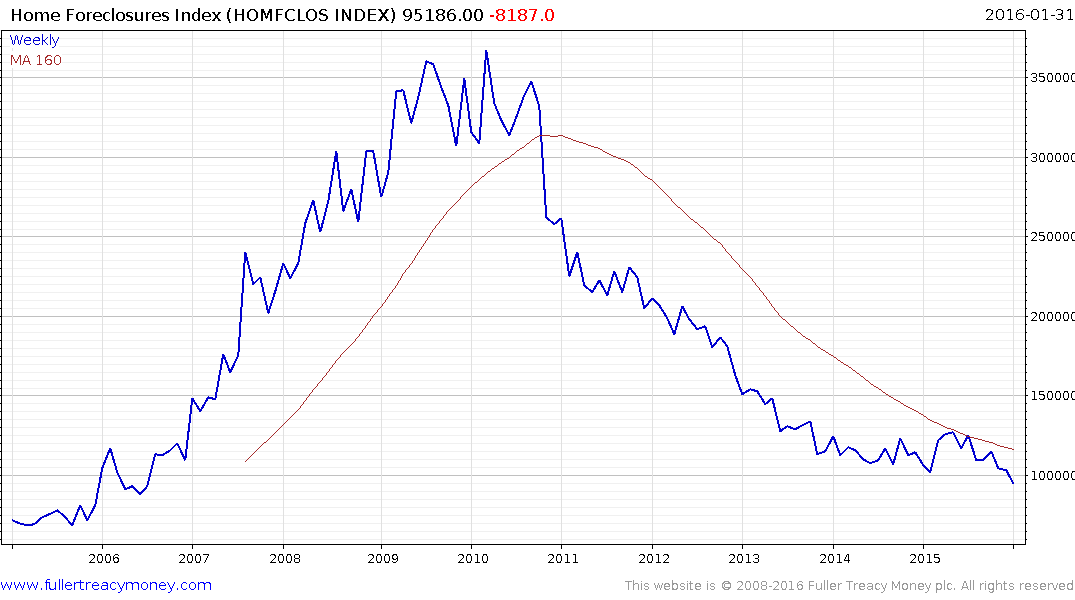

The relative strength of the US Dollar has increased the profits of foreign holders of US property but represents an increasingly high hurdle for the new buyers on which the trend of higher prices depends. Against that background home foreclosures hit a new recovery low at the end of January. However there is increasing evidence that banks are accelerating repossession of homes that have been in the bankruptcy process for the last couple of years.

Interest rates are still very low and the Treasury yields mortgages rates are priced off of are still attractive so there is scope for the market to absorb these properties provided nothing untoward happens to the economy or interest rates spike higher. With prices for lower priced homes rising fastest homebuilders are increasingly moving into the starter home segment.

KB Home specialises in homes for first time buyers and has an Estimated P/E of 10.7 and yields 0.75%. The share trended lower from its 2013 peak until early January and has since bounced to challenge its medium-term progression of lower rally highs. Some consolidation appears likely so it will have to hold the lows near $10 during any pullback if recovery potential is to be given the benefit of the doubt.

An additional story that caught my attention is how Blackstone is positioning itself in the current environment. The firm purchased vast numbers of single family homes during the housing crash and has more recently been selling its hotel properties; IPOing Hilton in 2014 and selling luxury hotels to Anbang over the weekend.

Investors represented a powerful source of demand for houses following the crash and represent a potent source of potential supply should they decide to sell so their actions are worth monitoring.

Anbang’s bid for Starwood Hotels, topping Marriott’s bid, suggests the Chinese may be in a hurry to deploy assets overseas before the Renminbi devalues any further. The currency has unwound its oversold condition relative to the trend mean but will need to strengthen further to break the medium-term downtrend.

Back to top