Cover title, initial cap only, goes

Thanks to a subscriber for this report from White & Case, focusing on the European leveraged debt market which may be of interest. Here is a section:

Although they barely existed in the pre-financial crisis days, cov-lite loans have become a firm fixture of the European leveraged loan landscape.

The growth and popularity of cov-lite deals reflects the shifting balance of power between borrowers and lenders in an era of looser monetary policy, lower interest rates and an increasing institutional investor base. In other words, yield seeking investors are willing to embrace more risk against limited deal flow. In 2017, the share of first-lien institutional loan issuance that was cov-lite topped 76 percent, up from a 27 percent share in the first half of 2016 and 52 percent in H2 2016.

While a European cov-lite loan sees the removal of maintenance covenants, it also typically has a so-called springing leveraged covenant in the revolving credit facility. Historically, these were tested when between 25 percent and 30 percent of the revolving credit facility was drawn. However, usage triggers have moved higher in 2017, with 47 percent of credits having a trigger greater than 35 percent compared to 18 percent of loans last year.

The use of portability, which was a regular hallmark of the high yield bond market, has also become more common in the loan market. It has risen from only 3 percent of loans in the second half of 2016 to 13 percent in the first half of 2017, although this slipped back to 8 percent in the second half of the year. This year has also seen a loosening of restrictions on acquisitions, with covenants not subjecting acquisitions to any monetary cap or any form of leverage ratio tests. The percentage of loans having no such restrictions climbed to 74 percent in the second half of 2017 versus 71 percent in the first half of the year.

Here is a link to the full report.

Here is a section from the report:

Although they barely existed in the pre-financial crisis days, cov-lite loans have become a firm fixture of the European leveraged loan landscape.

The growth and popularity of cov-lite deals reflects the shifting balance of power between borrowers and lenders in an era of looser monetary policy, lower interest rates and an increasing institutional investor base. In other words, yield seeking investors are willing to embrace more risk against limited deal flow. In 2017, the share of first-lien institutional loan issuance that was cov-lite topped 76 percent, up from a 27 percent share in the first half of 2016 and 52 percent in H2 2016.

While a European cov-lite loan sees the removal of maintenance covenants, it also typically has a so-called springing leveraged covenant in the revolving credit facility. Historically, these were tested when between 25 percent and 30 percent of the revolving credit facility was drawn. However, usage triggers have moved higher in 2017, with 47 percent of credits having a trigger greater than 35 percent compared to 18 percent of loans last year.

The use of portability, which was a regular hallmark of the high yield bond market, has also become more common in the loan market. It has risen from only 3 percent of loans in the second half of 2016 to 13 percent in the first half of 2017, although this slipped back to 8 percent in the second half of the year. This year has also seen a loosening of restrictions on acquisitions, with covenants not subjecting acquisitions to any monetary cap or any form of leverage ratio tests. The percentage of loans having no such restrictions climbed to 74 percent in the second half of 2017 versus 71 percent in the first half of the year.

The cult of the equity is largely a US, UK and Australian phenomenon. In Europe, bonds are still a popular asset class for retail investors. Retail investors in Italy will remember the reverse convertible products peddled by banks over the last couple of decades. The quantity of such products on the books of Banca Monte dei Paschi di Siena was one of the primary contributors to the bank’s eventual demise. If anything, this helps to emphasise the point that there is no shortage of dodgy products in both the bond and equity markets that tend to gain popularity when there is a dearth of yield.

In an environment where a substantial proportion of bonds had negative yields, demand for leveraged debt, often with light covenants has surged. In normal circumstances most people would have reservations about buying leveraged debt with light covenants but the desire for yield in a yield-starved world is powerful. It is inevitable that the surge in this kind of issuance is going to cause a problem in future but probably not until yields have risen and refinancing is imminent.

The Credit Suisse Liquid Western European HY Eur Overall Benchmark Spread has risen from a decade low of 250 basis points in November, to break the progression of lower rally highs. It is now ranging in the region of the trend mean and a break to new recovery highs would begin to suggest a more pronounced trend of pressure on the high yield sector. The fact that the spread chart is moving up faster than the Bund chart, with the spread expanding, suggests the high yield sector is very sensitive to the ECB’s actions in tapering.

Meanwhile the Barclays US Corporate High Yield spread is now testing the upper side of its tight almost yearlong range. A breakout to new recovery highs would begin to suggest some de-risking in the high yield sector which has historically been associated with a loss of momentum in the stock market.

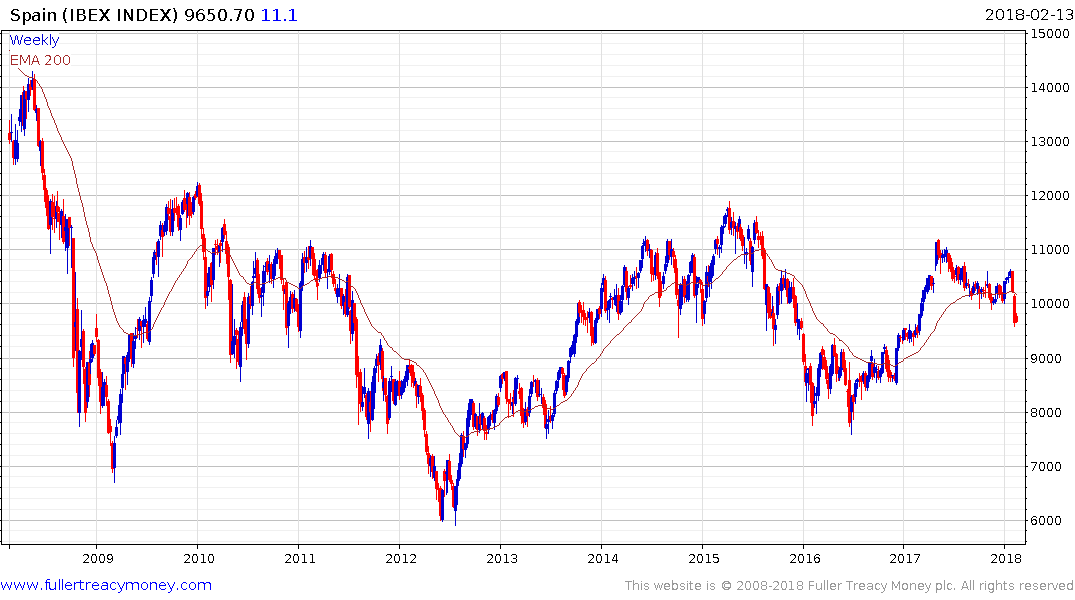

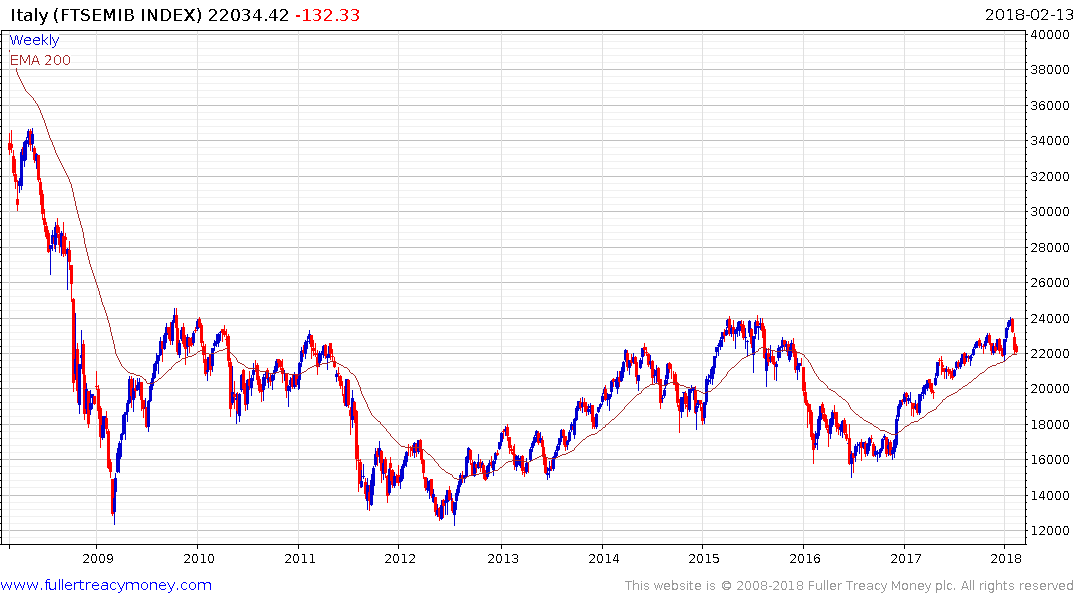

It occurs to me that Europe may be due its own version of a taper tantrum since it is certainly arguable that the economy is not yet ready to grow on a self-sustained footing with the tailwind of quantitative easing. The underperformance of the Spanish, Italian and Portuguese stock markets, as they pull back from the upper side of lengthy base formations could be symptomatic of that; particularly if they fail to find support in the region of their respective trend means.