Corporate America = Vapourware?

This article by Bernard Tan may be of interest to subscribers. Here is a section:

Here is a link to the full note and here is a section from it:

For this group of 50 companies, we can observe that over the past 11 years, they have handed over $3.38 trillion of cash to their shareholders while doing so much M&A that their Net Tangible Assets is now a mere $150 billion – an average of just $3bn per company! And they are saddled with near triple digit net gearing ratio.

The experience of Kraft Heinz should be a big warning sign that intangibles can become worthless overnight. The company wrote off over $15bn in intangibles recently which resulted in an >20% reduction in shareholders’ equity. The stock now continues to trade at a big discount to its book value presumably because Wall Street has suddenly woken up to the fact that the remaining $52 billion in equity is held at gunpoint by a still bigger $86 billion of now questionable intangibles. The share price is now just one third of the high reached in Feb 2017.

With so little equity relative to their intangibles, the entire corporate America can find itself in quicksand very easily.

Taking a step back, it’s as if corporate America has gone to the extreme of running corporations purely on cashflow paradigm. We seem to be way past balance sheet optimisation and well into cash flow optimisation.

One of the most significant side effects of ultra-low interest rates has been the creation of a clear incentive to take on as much leverage as possible. Whether that is justified as reducing the weighted average cost of capital, providing the funding for buybacks and dividend increases or for improving the veneer of EPS growth, the result is the same. Leverage has increased substantially.

Heinz was a prize asset when acquired by the rump of Kraft. Meanwhile, Kraft’s most prize assets were overseas, where there is still a growth market for established reliable brands. That is now Mondelez International. The leverage that was heaped onto the combined companies coupled with evolving eating habits, where sugar has been outed as one of the primary causes of obesity, have contributed to the share’s demise.

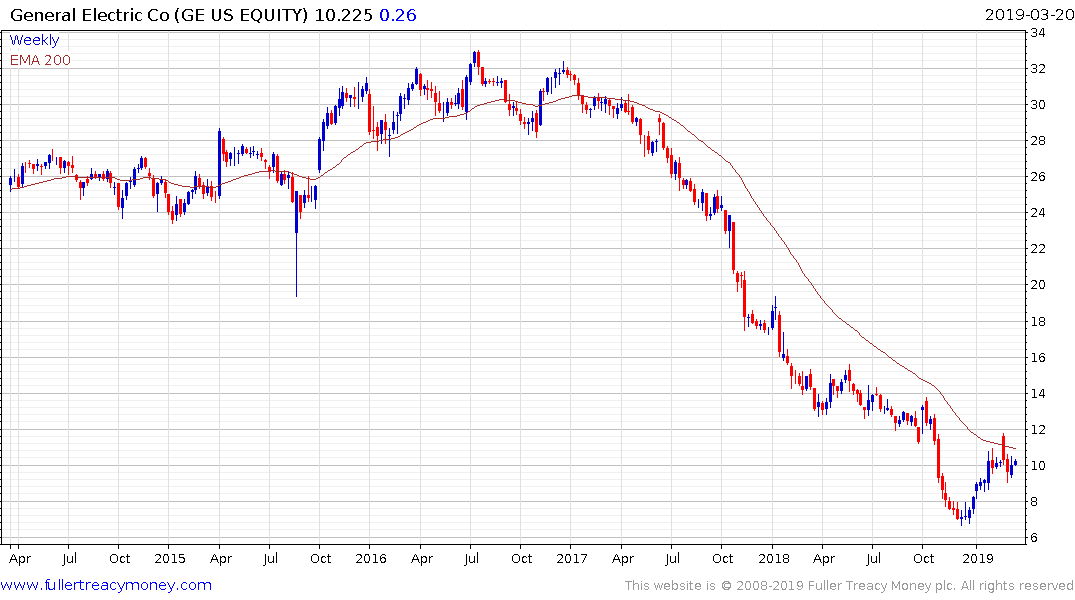

I would suggest that General Electric is another example of a highly leveraged company that has been forced to sell off some its’ most attractive assets in order to remain solvent. The companies which have acquired these assets such as Danaher, Baker Hughes, Wabtec are leaner businesses and better able to manage them.

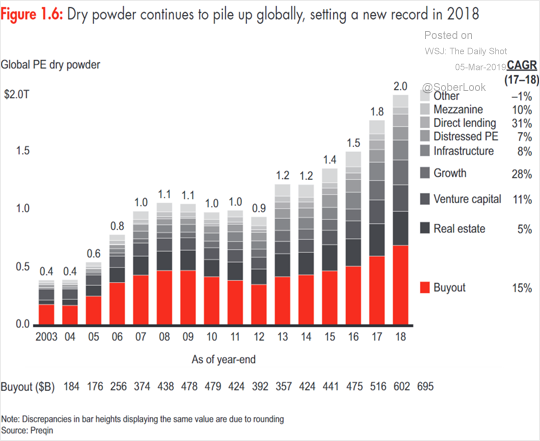

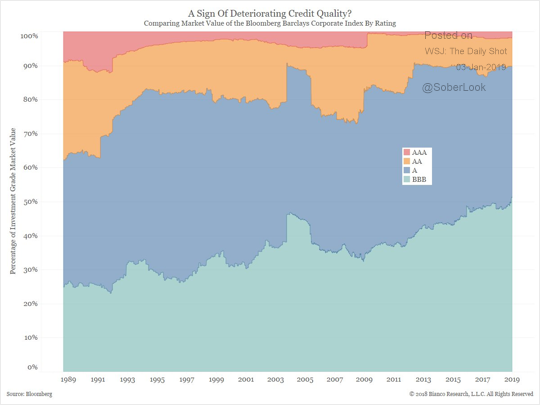

With more than half of all debt now rated BBB and a great deal of refinancing expected in the next couple of years, there is the real prospect that more highly leveraged companies will be forced to divest of attractive assets, to either maintain their investment grade rating or stay afloat. The $2 trillion in private equity, which is sitting on the sidelines waiting for buying opportunities, is likely waiting for these bargains to arise.