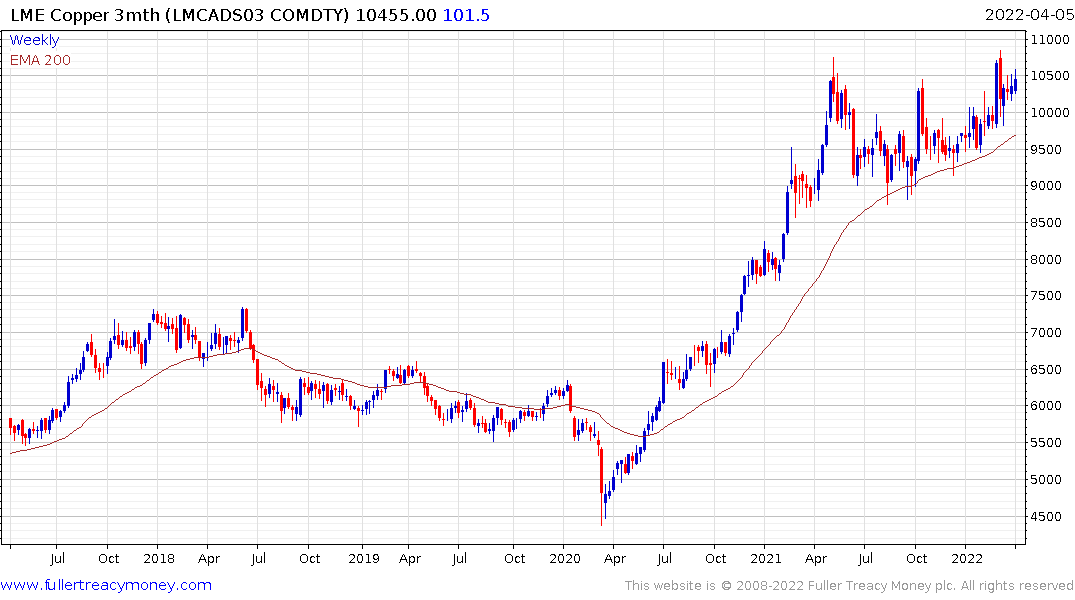

Copper: Supply meets demand concerns

Thanks to a subscriber for this report from UBS which may be of interest. Here is a section:

A link to the full report is posted in the Subscriber's Area. Here is a section:

Copper’s price action suggests that ongoing supply chain constraints are still the dominant price driver. Indeed, smelter closures in China and unplanned production suspensions as well as logistical challenges affecting scrap supply are among factors that continue to point to a more constrained supply side. Adding to this are prospects of lower Russian copper exports and anemic copper production in South America (in Chile, mine production fell 7% y/y to 399kt in Feb). Consequently, our estimate of a 3.7% increase in copper supply for 2022 versus 2021 is at risk.

But it is not just supply that is being challenged. China’s NBS manufacturing PMI slipped to 49.5 in March from 50.2 in February, reflecting the impact of extensive omicron-related lockdowns. Slower European copper demand due to an energy shock could have a more material impact on copper demand as well. This necessitates the need to track demand-related and macroeconomic news more closely in the months ahead. For now, we still target a rise in demand of 4.1% in 2022 versus 2021.

After accessing the supply and demand dynamics, we stick with our copper market deficit of 332kt (or 1.3% of demand) in 2022 and of around 240kt in 2023. As long as inventories are under downward pressure, we suggest being long copper by targeting a move to USD 12,500/mt. Alternatively, we like selling the price downside risks in copper for a 10% p.a. indicative yield over six months. We favor strike levels at USD 9,750/mt.

Ranging prices contribute to analysts hedging their bets of which direction prices are likely to breakout and how much they are likely to move. Nevertheless, by suggesting a strike on put options of $9750, which coincides with the trend mean, they are effectively saying give the benefit of the doubt to the upside provided it continues to hold that level.

The challenge at present is the big demand growth drivers for copper are visible but still in the future. Major battery manufacturing operations are still under construction. Once they open, demand for materials will surge. The desire to pursue energy independence, particularly in Europe, also suggests robust demand growth for the wind, solar and transmission sectors.

The present market is more focused on the near-term risk of interest rate hikes and the associated hit to demand. That suggests scope for near-term volatility before longer-term bullish characteristics take the lead again.

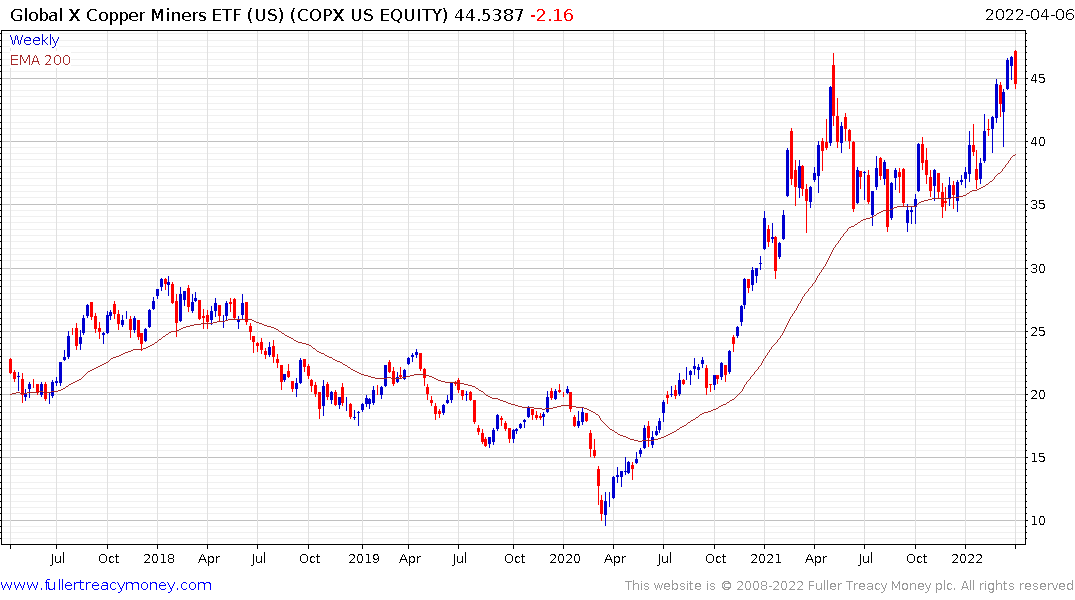

The copper miners ETF posted a downside key day reversal yesterday and followed through on the downside today. That increases potential for a full reversion towards the mean around $40.