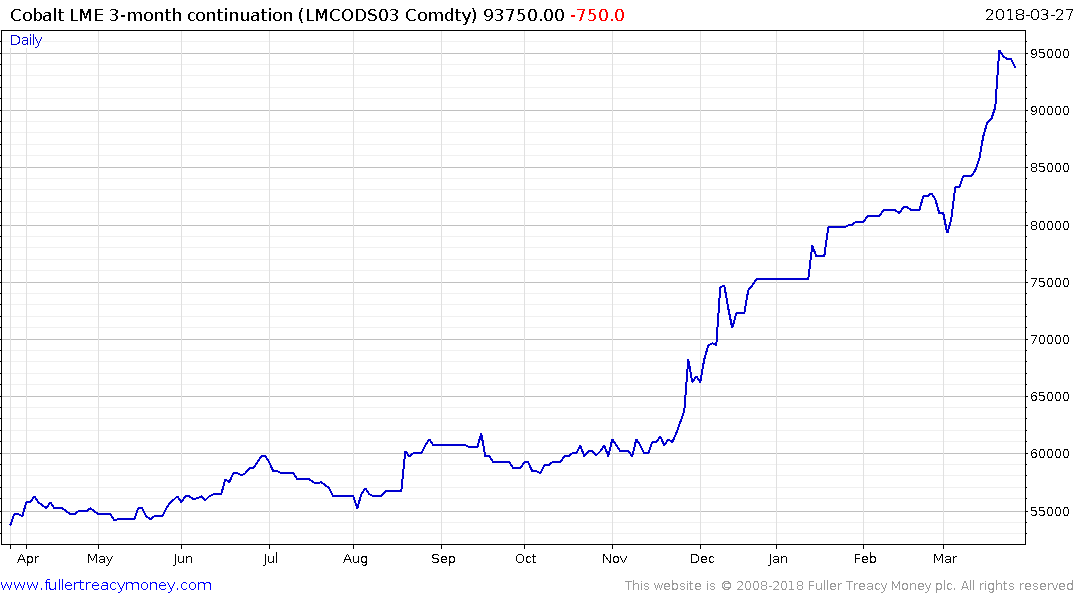

Cobalt price: Automakers 'waking up too late' as China takes control

This article by Frik Els for Mining.com may be of interest to subscribers. Here is a section:

The Democratic Republic of the Congo today has six of the top 10 cobalt mines globally. Due primarily to Chinese investment, by 2022, the central African nation will host the nine largest cobalt producers. Congo also holds half the world’s reserves.

Not only is primary production highly concentrated, but the downstream industry is beginning to resemble a monopsony. China, despite having no cobalt resources of its own, is responsible for 80% of the world’s cobalt chemical production, which overtook metal production around four years ago.

Glasenberg told FT Chinese refiners and processors "will have most of the offtake of cobalt":

They’re not going to sell batteries to the world, more than likely they’ll produce batteries in China and sell electric vehicles to the world,” Mr Glasenberg told the conference.

Despite the fact cobalt prices have surged there is no such thing as a cobalt mine. It is almost exclusively a by-product of copper and nickel mining. The Congo/Zambian copper belt therefore is the primary source of cobalt while it is a by-product of other mining operations all over the world.

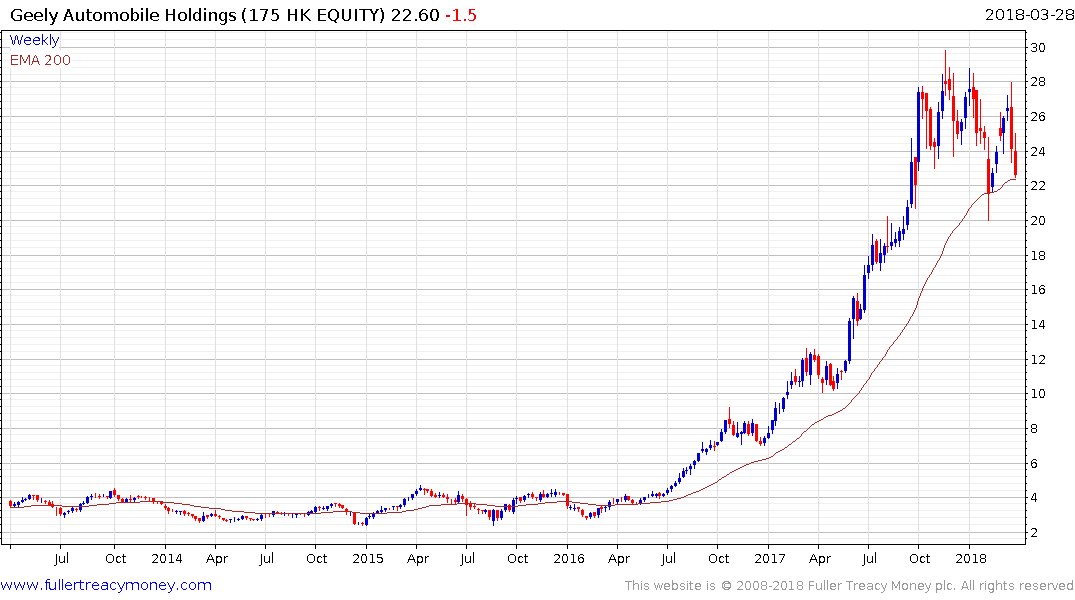

China is doing with batteries what it succeeded in doing with solar cells and is cornering the market for the manufacturing capacity and access to raw materials. It is inevitable that companies like BYD, SAIC, Geely and Greatwall Motors will be among the primary sellers of electric vehicles to both the domestic Chinese and international markets. After all, if Japan and South Korea can successfully build global auto manufacturing operations there is absolutely no reason China cannot do the same. That is particularly true considering the strong administrative resolve to do support higher value manufacturing.

BYD has first step above the base formation characteristics but downside follow through on today’s downward dynamic would challenge that hypothesis.

Greatwall hit a medium-term peak in October and continues to trend lower in a consistent manner. It will need to break the progression of lower rally highs to confirm a return to demand dominance.

Geely was among the best performing of any Chinese share in 2017 but has lost momentum this year and will need to hold the region of the trend mean if medium-term scope for continued upside is to be given the benefit of the doubt.

SAIC has held a progression of higher reaction lows since 2015 and is currently engaged in a reversion back towards the mean.

Glencore is starting to bounce from the region of the trend mean and a sustained move below it would be required to question medium-term scope for additional upside.