China Turns to Market-Boosting Playbook That BofA Calls Obsolete

This article from Bloomberg News may be of interest to subscribers. Here is a section:

“The margin call, forced sale, margin call vicious cycle can quickly develop a momentum of its own,” Cui, the head of China equity strategy at Bank of America in Singapore, said in an e-mail on Monday.

Doubts about policy makers’ ability to prop up the world’s second-largest stock market are spreading after a weekend interest-rate cut and speculation that regulators will halt IPOs failed to prevent the Shanghai Composite from tumbling into a bear market. The gauge would need to fall a further 13 percent to match its average downturn since 1990.

“Any support the government can provide would be short lived,” Chad Padowitz, the Melbourne-based chief investment officer at Wingate Asset Management Ltd., said by phone. “The only real support they can provide over time is providing a reasonably balanced, growing economy. That’s the best thing they can do. Anything they do short term, decreasing interest rates to support the market or things like that, are somewhat foolish.”

Expectations for future upside potential deteriorate within a range not least because they are boring and disappointing relative to the trending phases. We define ranges as explosions waiting to happen. However, the conditioning process of these congestion areas means that the strength of the breakout is often surprising to people most familiar with the market. Following an impressive breakout from a medium-term range prices will rally for as long as it takes supply to overwhelm demand. The test of whether a new uptrend can persist into the medium-term is in the extent to which the breakout can be sustained in the ensuing period of consolidation. This is what we term the first step above the base.

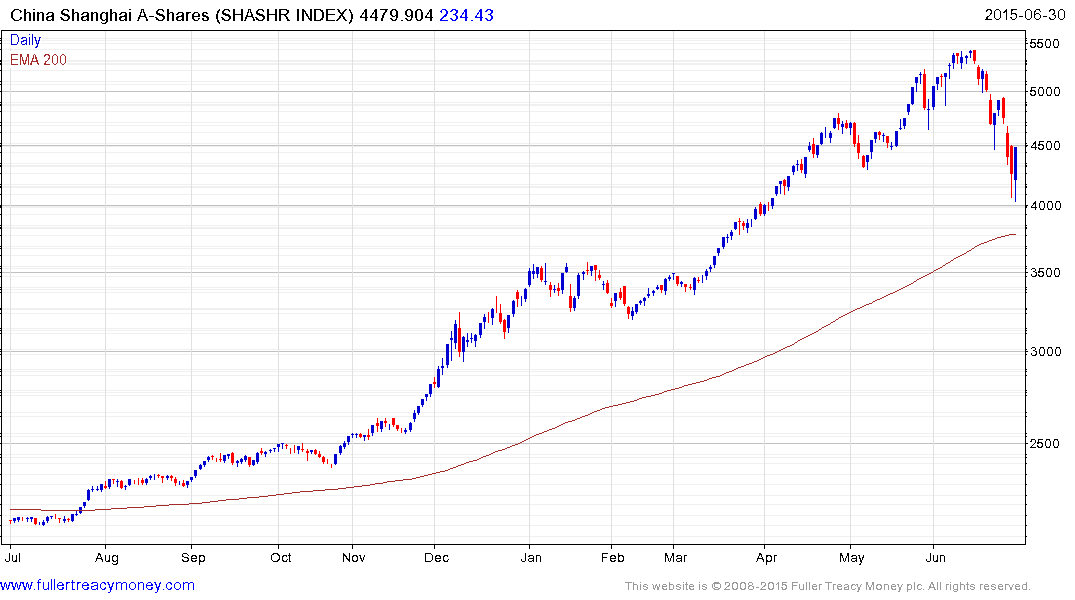

During the first step above the base two arguments predominate. The bull base will be that there is a new story that we need to be aware of, that valuations are attractive and monetary policy is attractive. The bear case will be that the breakout is nothing more than a flash in pan, that investors are dangerously overleveraged and that it will all soon end in tears. The big question then is whether this is a short-term boom to bust move or does it have capacity to be something more meaningful. China offers a good example of just this type of argument at present.

Today’s bounce on the Shanghai A-Shares from the region of the 200-day MA, following a steep decline represents at least a near-term low. Nevertheless, a period of support building will be required before a sustained move to new highs can be supported. The extent to which the monetary authorities continue to support the market will likely have a meaningful impact on performance.

Back to top